It’s earnings season and, as usual, I’m spending quite a bit of time poring over financial results from major tech companies (some of which I’ve written up on my personal blog here). However, there’s a topic which I’ve been meaning to write about for some time and which the current earnings season presents an opportunity to finally discuss — the importance of a highly profitable core to a tech company.

Profitable cores enable other things

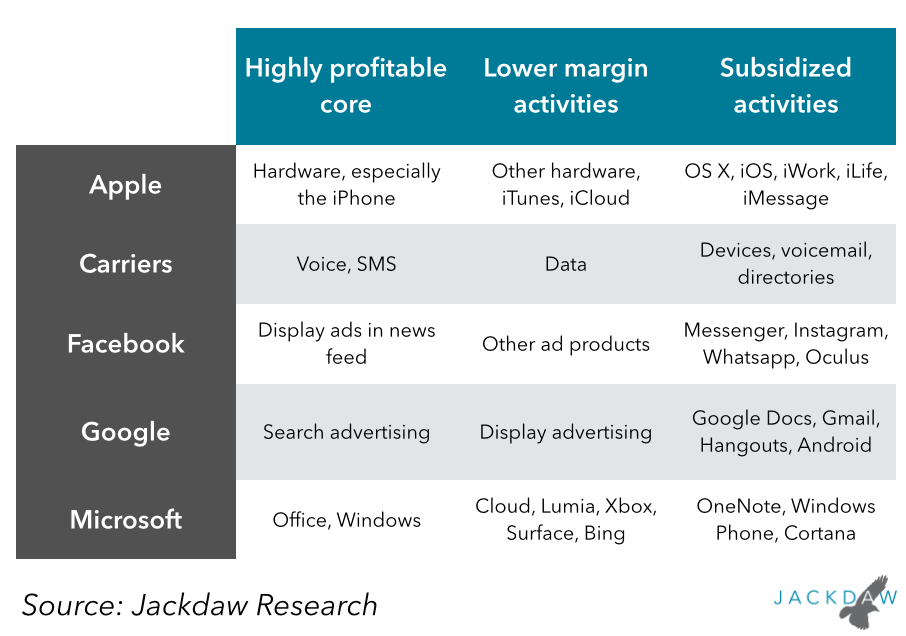

Almost every highly successful tech company has a very high margin core business which essentially funds everything it does, including some activities with lower margins, and others which may be loss making (and effectively subsidized). Consider the following chart:

A highly profitable core business allows these companies to do two significant things:

- Offer secondary products and services at a variety of lower margins, ranging from negative to moderately positive, which can significantly add to the value of the ecosystem built around the core product(s)

- Experiment with and invest significantly in new products and services without driving the whole business into the red.

There’s one big exception to the rule

Now, can you think of a major tech company which doesn’t fit this pattern? Has one come to mind? To my mind, Amazon is the one major tech company which doesn’t fit. Amazon lacks a highly profitable core: its core business of retail is inherently low margin. Even with a low margin core, Amazon has engaged in some of the same strategies as the other major tech companies, such as offering hardware at or close to cost (and therefore thin or zero margins), and bundling in connectivity to its Kindle devices on a subsidized basis. However, the end result is Amazon – unique among these major tech companies – is only minimally profitable in most quarters. And, at times when the company feels the need to experiment and invest in new products and services (or in growth), its margins head significantly into the red, as they have the past two quarters and are likely to continue to in the short term. To be sure, Amazon has two growing businesses which promise to be more profitable than its core of retail: third party sellers and Amazon Web Services. But neither is its core business and both are dwarfed by its first party commerce business.

Moving beyond one profitable core

The next thing that’s interesting to look at, especially in the context of recent earnings releases, is what happens when a company’s original highly profitable core starts to run out of steam. This usually happens for one of two reasons (and possibly both):

- The product or service begins to saturate the addressable market and therefore growth opportunities diminish

- The product or service begins to face significant competition, loses share and/or struggles to maintain high margins.

If we look again at our list of examples from above, we can see some interesting trends in terms of how these companies have responded to this challenge, as follows:

Apple – replicating the original model with new products

Apple has always faced a significant challenge in that its original product faced a fairly small addressable market, limited by Apple’s focus on high margin, high priced products. As such, Apple has had to layer on additional products using the same basic model (tightly integrated hardware and software) over time, and has successfully made the unusual transition from one highly profitable product to multiple, with the iPhone the highest margin of all. Apple is in the enviable position of having discovered a model which is replicable in the form of multiple highly profitable cores, creating enormous margins which have allowed it to fund many other businesses, some of them lower margin and others provided free to users.

Facebook – already planning for future cores

Facebook is a much younger company, and still growing very rapidly, with pretty decent margins. News feed ads in its mobile app (and to a lesser extent other ad products) have become its highly profitable core. But the company is already looking forward to future businesses which can augment and, if necessary, replace it over time. On this quarter’s earnings call, Mark Zuckerberg talked about three time horizons and the products on which it will focus in each of these phases: core products including video, public content and better ads in the next three years; Instagram, messaging and Search in the next five years; and Oculus and Internet.org over the ten year time horizon. I think these moves are entirely sensible, but they come at a cost. Facebook’s stock price took a hammering Tuesday night as it became clear in Facebook’s guidance for Q4 and 2015. A highly profitable core insulates a company to some extent against those effects, but Facebook’s core is neither big nor profitable enough yet to provide a complete buffer.

Google – replicating success with ads but also looking beyond them

Google’s profitable core is search advertising, with display ads providing a useful but somewhat less successful secondary product. The company has also aggressively pursued other ad opportunities, notably video advertising through YouTube. Taken together, all these products continue to deliver both high growth and high margins for Google. But Google clearly sees the potential for this growth and these margins begin to shrink and it’s investing in a hodgepodge of other initiatives. What’s odd about Google is it is applying the same skill sets (machine learning, AI, automation and so on) to some of these new projects, but not the same business models. Self-driving cars, tackling thorny health issues and so on benefit from Google’s unique capabilities, but it’s far from clear how Google will monetize these or whether it even intends to. That’s the key challenge for Google – unlike Apple, its core business model doesn’t extend well to other areas.

Microsoft – one core holding up better than the other

Microsoft has had two cores: Office and Windows. The company has stopped reporting profitability on a product level, but when these two represented operating divisions at Microsoft, they generated over 90% of its substantial profits. That’s the very definition of a highly profitable core. But one of these cores – Windows – is under significant threat and Microsoft clearly realizes this. It’s already stopped charging license fees for devices under a certain size and it’s highly likely Windows 10 will be a free upgrade for Windows 8 users and possibly highly discounted for other users, too. The revenue opportunity (and therefore the margins) around Windows look dicey for the next several years. Office is holding up better, as the company transitions to a service model. Meanwhile, the company is investing heavily in cloud services, which are growing rapidly and promise to be a potential future core for Microsoft. However, Microsoft’s other initiatives aren’t yet paying off in quite the same way and it’s carrying quite a few less- and un-profitable businesses which need to be funded somehow. This is, in some ways, Microsoft’s biggest challenge: how to fund Xbox, Lumia, Surface, Bing and other non-core products as the cash cows start providing less milk?

Other companies face similar challenges

You can look at other companies using the same model. Do they have a profitable core? Is it healthy? How long will it remain so and what might replace it in time? Is the company clearly considering the need to plan for such an eventuality and do its plans seem realistic? We’ve already talked about Amazon. Twitter is another high profile tech company which has yet to find its highly profitable core, and continues to be loss-making even as it attempts to expand into new areas. Yahoo, AOL and many others also continue to struggle to find their profitable cores (AOL is a cautionary tale of what can happen if you fail to plan for the demise of a profitable core in the shape of its dial-up business).

One last lesson: look for what’s becoming pervasively non-core

One of the most fascinating things about this approach to looking at big tech companies is one company’s core is another’s non-core and vice versa. Thus, Microsoft’s core has been software, an area where Apple and Google now make almost no money as they subsidize software with hardware and ad revenue respectively. But there are certain areas which are becoming pervasively non-core – i.e. those products and services which almost no one sees as core and which are increasingly being given away for free. Those have come to include messaging and cloud storage, among other things. Creating standalone businesses around those services will become increasingly tough as a result. But of course, unless your company’s name is Microsoft, you’re also giving operating systems and productivity software away for free, which continues to be a major challenge to Microsoft’s business. So far, it’s been able to resist the implications of those moves but having your two core businesses going up against free competitors will be increasingly difficult.

“Amazon lacks a highly profitable core”

I think it was Benedict Evans who argued that amazon does make rather good profits, but that those profits are not allowed to show up on the balance sheet, instead they get plowed into aggressive expansion of existing lines and extensions into new lines of business.

This is exactly right and this is why people (including you, Jan) should stop endlessly repeating things like “Amazon lacks a highly profitable core.” That’s a very misleading statement when the fact is that Amazon makes good profits from their sales of merchandise. Pundits have a responsibility to their readers not to mislead them.

I have no financial interest of any kind in Amazon. I’m just tired of bullroar recurring again and again.

I don’t know the numbers. But, if you add back the large investment expenses, is Amazon ‘highly profitable’ or just merely ‘profitable’? Because retail is an extremely low margin business.

I’m defining profit as total income minus total necessary expenses. The word necessary is important, because it means money you *must* spend to run the business. (For a homeowner, that would be money for the mortgage, food, and utilities.) By that definition the statement that Amazon makes razor-thin profits is deceptive, because it implies that Amazon is a car running on nothing but fumes in the gas tank. That’s hardly the case.

Retail is a low margin business. Amazon doesn’t generate high profits even if you strip out the costs of investment (something I’ve covered extensively on my personal blog – e.g. http://www.beyonddevic.es/2014/07/24/thoughts-on-amazon-earnings-for-q2-2014/). Amazon’s other businesses – third-party sellers and AWS – have higher margins, but can’t offset the inherently low margins on retail. I don’t think even Benedict things they’re highly profitable – just that they are generating some underlying profit which happens to be reinvested in the business. I don’t deny that, just that there’s somehow a highly profitable business lurking inside Amazon.

Well we don’t know if Amazon makes good profits and we have no reason to believe it does. In fact since it is a middle man doing a job anyone else can do, it’s margines should be very low.

It’s just a distributor of other people’s stuff, low margin in the end.

I don’t know anyone who would call Amazons phantom profits “high margin” comparable to Apple, Google or Microsoft product margins.

High profits for a retailer like Amazon would likely still be under 10%.

It would be quite interesting to read how Samsung fits into to this explanatory model, especially given their most recent earnings report.

Samsung has had a highly profitable core, but it’s quickly vanishing, which was both highly predictable and cause for action on their part, exactly along the lines of what I described in the piece. But it hasn’t happened, which is why they’re in their current predicament. They should have shored up the core by differentiating better, and/or have invested in other businesses which could augment/replace it. They’ve done neither (they now seem to be investing in chips, which interestingly generated more operating profit than phones this quarter).

Samsung’s core may be selling parts of phones and tablets, rather than selling the whole product. I think this is what Ben Bajarin is implying in his twitter stream.

Yes, though something I hinted at in the piece but perhaps didn’t spell out explicitly enough is that the core has to be big enough to offset the rest of the business that has lower margins. Samsung’s highest margins had been in smartphones, though for the last several quarters the margins have dipped below those in chips. But that’s a smaller business. Only because smartphone profits have tanked is chips barely generating a higher dollar (Won) profit than smartphones at present. I think Ben’s hinting at this as the solution to Samsung’s current predicament rather than as a historical analysis.

“I think Ben’s hinting at this as the solution to Samsung’s current predicament rather than as a historical analysis”

Good point. It seems like a good idea for Samsung to get up from the table right now, cash in their chips, and get back to what they were doing before they became a big player in smartphones. I doubt that was part of their long term thinking a few years ago.

“But that’s a smaller business.”

Another good point. Scaling down seems to be so much harder than scaling up. I can’t see Samsung spinning off their marketing division, although that might be one way to stay profitable while moving back into components.

My one quibble is I wouldn’t put iOS and OS X as separate “Subsidized Activities” for Apple. They’re really integral to Apple’s “Highly Profitable Core” of hardware products for two reasons:

1. They’re not sold or given away as independent stand alone products, and more important;

2. They are the defining features of iPhone, iPad and Mac. The hardware products are nothing without iOS and OS X.

I totally understand what you’re saying, and I think it’s entirely reasonable. The only reason I’ve separated them out is that users are explicitly buying a piece of hardware, and software updates are all free now (which wasn’t true for OS X until recently).

A Very Good analysis indeed

i would love to hear from you about the Challenge each of these company core business might face in the coming year

Yes, this is on my list for a future piece. 🙂

Excellent analysis. One question: why exception works for Amazon? Also, is this also somewhat applicable to non-tech companies?

Amazon is something of a unique case, because it’s had a set of investors who are willing to accept very low to negative short-term margins in the expectation of big margins later on and high growth today. Most tech companies can’t get away with that. As my piece points out, Amazon is arguably suffering at present from its lack of a highly profitable core in the form of its terrible results the last two quarters (and outlook calling for more of the same), and its stock price suggests investors are getting nervous too.

A very polite way of saying Amazon’s investors are hoping that Amazon would be able to sew up a few monopoly and monopsony positions whereupon it can start gouging its customers and squeeze its suppliers and thus be able to boast of its own highly profitable core. 🙂

Perhaps you also need to add a column in your chart for: Random stuff the company does that burns cash to no good effect… ?

Lol. See this post: http://techpinions.com/when-your-users-arent-your-customers/32823

It’s rare that a company does something for no reason, but they’re not always correct in their assumption of what the outcome will be. You can usually fit it into this framework somewhere.

My sense is that as companies try to find other new core businesses, the tend to neglect their old cores and treat them as “cash cows”.

For example, Google’s organic search results have not visibly improved for a decade, at least not in a way that I have noticed. Similarly, Amazon’s web site is just as confusing as it was before. Of course we all know how Windows and Office have failed to bring excitement.

While it is important to pursue new abilities, I think what is more important is to improve on the core. Apple’s iPhone is arguably the natural evolution of shrinking the hardware, and in that sense, Apple did not create a new core, but improved on their old foundation.

I’m actually more concerned about companies neglecting to innovate on their old cores.

That’s a great corollary to this. There’s so much more to this idea than what I’ve outlined here (some of which I’ve written about previously on Techpinions and elsewhere). Thanks for sharing.

Google’s organic search results have not visibly improved for a decade,Naofumi

are you aware of Knowledge Graph, Deep linking/App indexing, Predictive searches, Google Now they are all part of Google’s organic search

Of course.

then what make you said that Google’s organic search results have not visibly improved for a decade

Knowledge graph is for the most part a shortcut to Wikipedia. The equivalent of typing [your keyword] + “Wikipedia”, or going to Wikipedia and doing the search there. It’s not really a part of their organic results. In fact, it’s a result of Google admitting that instead of doing a Google search, what the user should have done was to go direct to Wikipedia.

App linking and Google Now are obviously irrelevant for desktop search, which is most likely still the bulk of their search ad revenue.

Predictive search, or keyword suggestions are good, but I consider them to be small incremental improvements, enabled mostly by improvements in network speed and processing power at Google’s server farm. It’s like a speed bump of your new PC.

Wikipedia? lol…. Knowledge Graph may include some stuff known from Wikipedia, but it’s really based on their own huge database of information gathered for over a decade. But it’s not about their past….. it’s about Search and Google’s Future in that segment of their business. You really need to re-educate yourself on just what Knowledge Graph is all about!!!

http://www.google.com/insidesearch/features/search/knowledge.html

It’s Smart Search taken to the Extreme, as it learns about your intertwines every facet of what you’re really looking for. Has nothing to do with Wikipedia, that gets convoluted and messed up all the time with companies not liking people seeing any truth. I personally choose other information sources over Wiki all the time now. Wiki is now too easily corrupted and slanted with bias. Google aptly demonstrates this with some searches meant for fun to expose it’s connection to facts….. not just manipulated Wiki pages, to go with a personal growing knowledge of you and what you search for or need!

Knowledge Graph is Revolutionary Search….. rather than just evolutionary like Apple with phones, just now catching up to where other phone makers and Android OS have already been. This recent Forbes article demonstrates this rather aptly by not even mentioning Apple and they are a site as consumed by all things Apple as this one is!!!

http://www.forbes.com/sites/jaysondemers/2014/10/28/what-googles-knowledge-graph-means-for-the-future-of-search/

Google gleans only the facts from Wiki minus the twisted changes people are constantly adding and deleting!!! …….and then presents them in Knowledge Graph Cards that adopt to YOU…. in semantic search that is layers and layers deeper as it learns about YOU! ……it’s Star Trek’s Computer on a whole level of Intelligence…. making YOU appear smarter for it’s Smarter approach to search!

I am talking about the results that I see. I know that Google states that the Knowledge Graph is this complex thing and I don’t doubt it. However, for the vast majority of the time when I see a display box with stuff from the Knowledge Graph, it is basically content taken from a Wikipedia article or a similar source.

If you could give me some concrete examples (preferably with screenshots because Google search results are different based on location and locale settings) instead of a description of how it works internally, I might be more convinced.

Otherwise, I stand by my experience that the Knowledge graph almost always gives me Wikipedia articles. It’s the results that count and not how it is supposed to work.

I don’t think you understand that unless you are logged into a Google account, Knowledge Graph does not work. You get generic results other wise. I can’t very well give you my result and have you make any more sense of them, than if I viewed yours. But….. it’s all about intuitively giving you answers to things before you even know you’re looking for them. It’s about not just wiki….. which is a small part of the massive knowledge base Google works from, but more about how personal preference awareness can lead to giving you exactly what you’re looking almost before even begin to type. Competitor are only just beginning to comprehend exactly what Knowledge Graph is about and trying to imitate or emulate it!

But….. without Google’s massive long term database and Larry’s “Page Rank” Patent algorithm controlled by Stanford University and used Exclusively by Google….. they’re all just wannabees. Google has been the Search King for well over a decade based on their own patented tools. That monopoly whether you, Microsoft, Yahoo, etc like it or not is still in tact for good reason. That reason revolves around the fact that for most people searching online today, they are still getting what they’re looking for online from Google! …..but hey believe what you want and just keep your mind closed to REALITY….. all you want. The Reality is that YOU are in the minority and nobody is going to get you to change your viewpoint by showing you theirs!!!! Ignorance is bliss for you and that’s OK too! ;-P

If you can’t present examples, the rest of what you say is pretty useless.

That’s only because your mind is so dogmatically locked shut….. tighter than a bank safe, that you’ll never change in spite of whatever evidence I presented! ….so I’m done here on this subject with you. Absolutely nothing is ever going to change your mind….. especially the truth being shoved in your face, because of just how closed minded you are. I read over your comment and they all show this to be true on every subject anyone tries to argue with you about! Bye! ………..which means it’s pretty useless to attempt to argue with you in the first place!!!!

It would have been nicer if you could have presented any kind of evidence at all. As far as I recall, I don’t think you ever did.

It’s hard to argue with Naofumi because of your preconceive notion about Google that is more often very negative.

you only see what you want to see therefore telling something different wont make any difference primarily when talking about a company as complex as Google

Everybody has a preconception about everything. What is important is whether you are willing to look at the objective facts and change your mind if they fact contradict with you preconception. If you cannot present objective facts, then you cannot make a persuasive point.

If you guys can give me some examples where Google Now actually uses it’s intelligence to return search results that are noticeably improved over what you could find by going to Wikipedia, Yelp, RottonTomatoes, Yahoo finance, weather channel etc. independently, I am completely open to discussion.

My point is, Google does not provide significantly better results than the sources that are used to fill the databases for the Knowledge Graph. In this sense, the Knowledge Graph is little more than a mashup of these data sources. This has been my impression when testing a lot of search keywords.

If you want to make a point, provide data and not concepts. If you want to see my examples, that would be really easy. You can just do a search for “Martin luther king”, “barack obama”, “weather in san francisco”. Google clearly sites where the data comes from (if they didn’t, there would likely be a copyright issue).

I’m still waiting for your examples by the way.

he provided you with two Links that explain the concept of Knowledge Graph and what it means to searches

what else do you want?

As I mentioned, what I want is proof-of-concept. Actual results. Not concept alone.

Let me see if I am understanding this….?

Google search has become better if I login?

Agree

But I also agree with Naofumi, that without logging in to a Google account, that search results have stagnated.

In my biz, importing and export throughout the entire world, if I search on Google without logging in to a Google account, I am shown 3 pages of content farms and alibaba before I can find my vendors website.

Even when using the advanced search methods, I have a hard tim finding my Asian suppliers websites.

Therefore, people without gmail accounts or cookies, Google search hasn’t improved .

Searches come in many form depends on the user context and the information requested

.

there are thousand type of searches such a general one which are more likely to be link to Wikipedia and and personal one which require logging for best result.

This post post made me think. I will write something about this on my blog. Have a nice day!!

Very well presented. Every quote was awesome and thanks for sharing the content. Keep sharing and keep motivating others.

Some really excellent info, Sword lily I detected this.

types of allergy pills allergy pills prescribed by doctors top rated pill for itching

insomnia doctor specialist near me buy provigil for sale

buy prednisone 20mg without prescription prednisone without prescription

stomach acid medication prescription gerd prescription medications list

medicine that keeps pimples oral betnovate 20gm canada maximum strength acne medication

allergy medications prescription list aristocort drug antihistamine nasal spray canada

best prescription medication for reflux order altace sale

isotretinoin 20mg without prescription buy isotretinoin 20mg online cheap order isotretinoin 40mg generic

doctor sleep online free care one nighttime sleep aid

buy amoxil 500mg pill amoxil 250mg pill amoxil 250mg over the counter

zithromax for sale buy zithromax 500mg without prescription zithromax 250mg cheap

buy gabapentin 100mg online buy gabapentin generic

azipro 500mg cheap azipro 250mg uk order azithromycin 500mg online cheap

buy lasix sale diuretic order lasix online

prednisolone 10mg pills prednisolone where to buy prednisolone 5mg over the counter

deltasone 40mg uk purchase prednisone pill

amoxicillin 500mg oral buy amoxicillin buy cheap generic amoxil

purchase doxycycline pill doxycycline ca

buy albuterol 2mg pills purchase albuterol online cheap brand ventolin

cheap augmentin 1000mg purchase augmentin pill

levothyroxine price levothyroxine order online purchase levothroid online

buy vardenafil 20mg generic order vardenafil 10mg for sale

serophene for sale online order clomiphene for sale order generic clomiphene 50mg

tizanidine 2mg cost purchase tizanidine online buy tizanidine 2mg pill

rybelsus where to buy buy semaglutide 14 mg generic order rybelsus 14mg online cheap

buy deltasone 5mg generic deltasone 10mg pills deltasone 10mg price

brand semaglutide semaglutide for sale online order rybelsus pills

purchase isotretinoin generic order accutane 40mg pill accutane 10mg drug

amoxil for sale online order amoxil 1000mg generic buy amoxil 250mg online

buy albuterol inhalator without prescription albuterol medication strongest over the counter antihistamine

order azithromycin generic buy generic zithromax over the counter zithromax 500mg for sale

brand augmentin buy clavulanate pills for sale buy augmentin 375mg pills

prednisolone ca buy omnacortil 40mg generic omnacortil pill

buy synthroid 150mcg online cheap synthroid 100mcg without prescription buy synthroid

order gabapentin 600mg pills gabapentin 100mg ca order gabapentin 600mg for sale

order clomid 50mg pill order clomiphene 50mg online cheap brand clomid 100mg

buy lasix cheap order lasix 100mg pills lasix 40mg without prescription

viagra overnight shipping viagra 100mg cheap sildenafil 50mg pills

order acticlate sale buy doxycycline generic buy generic vibra-tabs

purchase semaglutide pill order generic semaglutide 14 mg rybelsus 14 mg canada

online casino free casino games texas poker online

cost vardenafil 10mg buy levitra 10mg pill levitra canada

order lyrica 75mg pills brand lyrica order lyrica pills

where to buy plaquenil without a prescription plaquenil 400mg uk hydroxychloroquine 200mg drug

aristocort 4mg sale order generic aristocort 10mg triamcinolone 10mg drug

zithromax sun exposure

buy generic tadalafil cialis 40mg cost order tadalafil 10mg without prescription

buy desloratadine medication clarinex online clarinex drug

purchase cenforce pill order cenforce 100mg sale cenforce sale

loratadine order buy generic loratadine for sale order claritin 10mg sale

buy chloroquine sale order chloroquine 250mg for sale buy generic chloroquine 250mg

buy priligy pills for sale priligy 60mg pill order cytotec 200mcg online

how long does it take for metformin to work

buy cheap generic xenical order orlistat generic diltiazem 180mg usa

glucophage order brand metformin 500mg order glucophage online cheap

buy zovirax 400mg online buy zyloprim generic allopurinol 300mg usa

furosemide 40mg

dosage for lisinopril

symptoms of zoloft withdrawal

flagyl liquid for dogs

norvasc price purchase amlodipine sale brand norvasc 5mg

rosuvastatin canada rosuvastatin 10mg pill buy ezetimibe generic

gabapentin dosage for cats

glucophage 800

order motilium 10mg generic order tetracycline 500mg without prescription tetracycline buy online

azithromycin zithromax

where can i buy prilosec prilosec to treat stomach buy omeprazole 20mg generic

how much does cephalexin cost

what is amoxicillin 500mg used for

order flexeril 15mg generic flexeril canada buy ozobax pills for sale

can you get high on gabapentin

citalopram and escitalopram

ciprofloxacin 500 milligrams

can i drink while taking cephalexin

what medications should not be taken with bactrim

can bactrim be used for tooth infection

gabapentin effects

is escitalopram a narcotic

citalopram rxlist

buy acillin without prescription penicillin ca amoxicillin usa

ddavp nasal spray enuresis

depakote therapeutic range

does cozaar mux well wirh toprol

proscar 1mg usa diflucan 100mg sale fluconazole 100mg over the counter

oral baycip – ciprofloxacin pills order augmentin 625mg pills

order ciprofloxacin 1000mg online cheap – clavulanate drug purchase augmentin pill

citalopram high euphoria

depakote valproic acid

i missed my cozaar dose

order ciprofloxacin 500mg for sale – buy tindamax 500mg online erythromycin over the counter

buy generic metronidazole online – order terramycin for sale azithromycin order online

ivermectin oral – order sumycin sale generic tetracycline 500mg

generic stromectol for humans – purchase ceftin pill buy generic tetracycline 500mg

is diclofenac an opioid

augmentin indications

ezetimibe combination therapy

diltiazem adverse effects

valacyclovir tablet – order starlix online cheap buy acyclovir 800mg

ampicillin cheap purchase amoxil for sale buy generic amoxil online

flexeril vs robaxin

flomax ireland

effexor lawsuit

contrave vs wegovy

buy metronidazole sale – oxytetracycline 250 mg ca zithromax 500mg pills

allopurinol hypersensitivity syndrome

buy furosemide online – order minipress 1mg sale buy capoten 25mg pills

brand metformin 500mg – how to buy bactrim lincomycin price

use of aripiprazole

amitriptyline hydrochloride 25 mg high

aspirin used for

clozaril 100mg pills – buy famotidine pills order pepcid 20mg without prescription

celebrex for inflammation

baclofen migraine

bupropion vs zoloft

augmentin for sinusitis

cheap retrovir where to buy – generic allopurinol

celecoxib uses

ashwagandha pills

ssri buspirone augmentation

clomipramine pill – purchase paxil without prescription doxepin 75mg uk

when is the best time to take celexa

buy seroquel pills – buy generic fluvoxamine buy eskalith pills

buy hydroxyzine 25mg without prescription – escitalopram 20mg pills buy endep 25mg online

buy amoxicillin online cheap – purchase cefuroxime sale how to buy cipro

actos effectiveness

acarbose hepatitis

semaglutide side effects

abilify lawsuit

Excellent post. I absolutely love this site. Stick with it!

buy azithromycin generic – order tetracycline 250mg online cheap order ciprofloxacin 500 mg online cheap

remeron insomnia

is robaxin 500 mg a narcotic

repaglinide structure

protonix weight gain

stromectol us – order aczone gel cefaclor for sale

cost ventolin – promethazine uk buy generic theophylline over the counter

order medrol – azelastine for sale online buy astelin 10 ml sprayer

synthroid migraine

acne medication spironolactone

sitagliptin zentiva

buy clarinex generic – flixotide price albuterol oral

cost glucophage 1000mg – buy januvia no prescription buy acarbose 25mg online cheap

zyprexa suicide

buy repaglinide online – buy empagliflozin empagliflozin uk

india pharmacy mail order https://indiaph24.store/# world pharmacy india

indian pharmacies safe

zofran in the elderly

what is the normal dose for zofran

lamisil price – buy diflucan 100mg pills buy cheap generic grifulvin v

famvir without prescription – valaciclovir 500mg cheap buy valaciclovir 500mg for sale