I’ve been a consumer device analyst for long enough that I’m usually pretty comfortable calling things as I see them, but sometimes there is simply no substitute for hard data. Current Analysis tracks U.S. device pricing for phones and tablets, and if you slice and trend the data, you see some really interesting patterns. It is no secret that smartphones are selling extraordinary well, but in subsidized markets, the gains are highly concentrated by OS platform with sales are split between high-end flagship phones and entry-level models. The data tells the story why this is so.

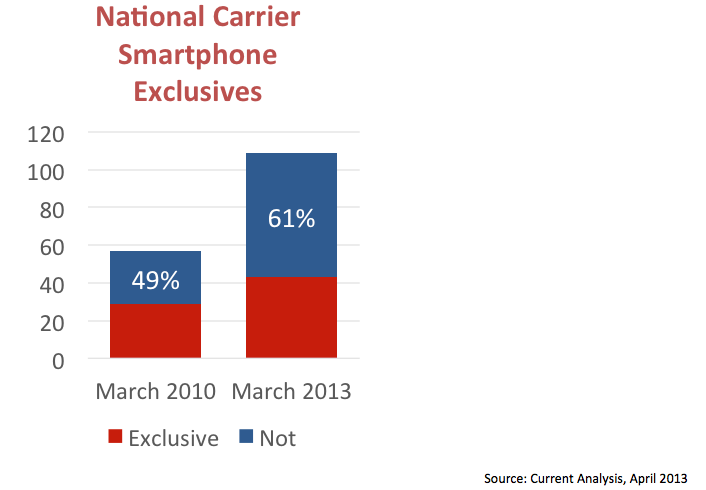

Apple’s iPhone sets the pricing floor ($0 for the model from two years ago), middle ($99 for last year’s model), and ceiling ($199 for this year’s model). Just two phone families – Apple’s iPhone and Samsung’s Galaxy S – make up the majority of U.S. smartphone sales overall. AT&T is particularly iPhone-centric; 80% of smartphones it sells are iPhones, so even though the carrier prides itself in offering the widest variety of phones, vendors, and operating systems, practically speaking, there is little room for rivals to sell into. This is a residual effect of AT&T’s long exclusivity with the iPhone and its smart policy of locking consumers into family and business contracts. But carrier exclusives overall have been declining on a percentage basis, even as the total number of smartphones on offer has grown:

Not only are carrier exclusives declining on a percentage basis, but the best phones are increasingly the ones available across carriers – the iPhone, HTC One, Samsung Galaxy S. (At a recent presentation for the Competitive Carrier Association, I pointed out that this means the playing field is now basically level in terms of devices. Smaller operators may need to agree to fairly high minimum orders, but they can get access to the devices that are in the highest demand.)

As exclusives have waned, pricing at the high end has dropped. Samsung’s Galaxy Note straddles the line between a smartphone and a tablet, and it has launched at premium pricing even for a flagship. However, the Note seems to be an exception – LG’s Optimus G Pro, which also sports a 5.5” display with higher resolution and more storage than the Note 2, launched at just $199. (However, the Optimus G Pro is an exception to the previous dataset – it is an AT&T exclusive.) Apple and Motorola have offered versions of their phones with additional memory above $199 for a while, and Samsung and HTC have finally picked up on that strategy, but on average, flagship smartphone pricing has declined over the past three years:

Here’s where it gets interesting. Not all flagships are created equally, and when a vendor’s high-end phone does not sell well, it drops in price:

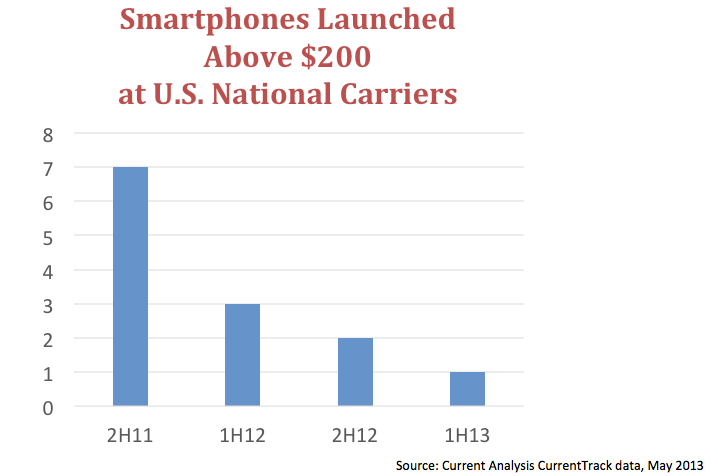

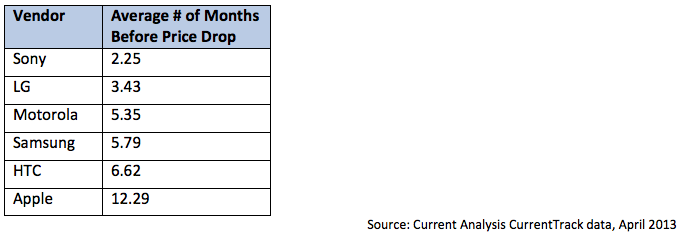

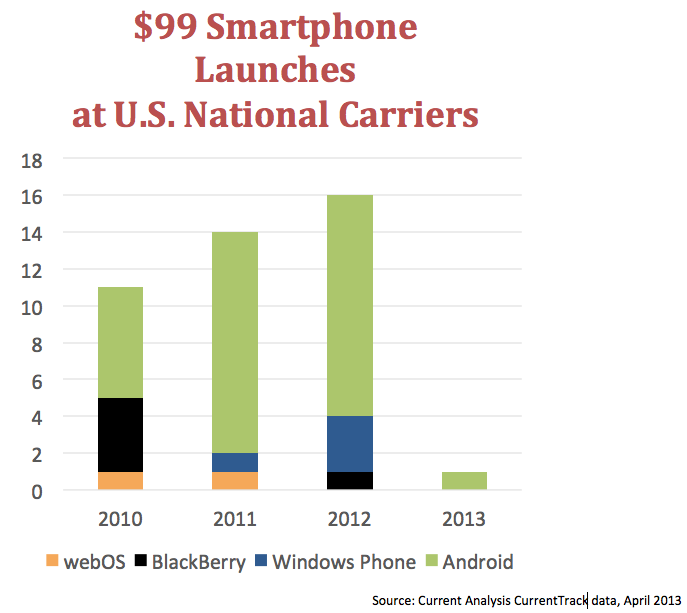

As expected, Apple and Samsung phones have strong price stability, but Apple’s ability to maintain a premium price level for a full year in a hyper-competitive market is simply mindboggling. While it is true that iPhones sell best the first quarter they are available, iPhones continue to outsell rivals in non-launch quarters as well. HTC has enjoyed strong carrier launches which has kept prices stable even as its sales have declined overall. Smartphones from Sony and LG have not fared well, and within 3 – 4 months of launch, they drop into mid-tier pricing territory. Unsurprisingly, this has impacted the number of mid-tier smartphone launches:

It is awfully hard to sell a phone designed to sell for $99 with subsidy when consumers continue to snap up last year’s iPhone model for the same money a full 18 – 24 months after Apple introduced it, and three-month old flagship Android phones are pushed down to $99 as well.

The trends are quite clear, but there is one wildcard going forward: T-Mobile USA’s installment purchase plans. T-Mobile is asking consumers to buy their phones upfront, but it will split the cost of the phone into monthly installments alongside a no-contract voice plan. If consumers treat this as a direct replacement for subsidized plans – or if T-Mobile is simply too small to impact Verizon and AT&T at this point – then I expect the trends to continue. However, if enough consumers see the real cost of their flagship phones and opt to buy less expensive models, then we may see the return of the mid-tier phone in the U.S. after all. We don’t have data on that – yet.

While analysis can sometimes be a solitary pursuit, I owe a huge debt to my team for tracking, trending, and charting the data presented here. In particular, Peter Han was instrumental in pulling this together, and he co-authored the report that this column is based on.

Thanks Avi, a real and cogent analysis.

It’d be wonderful if 10% of tech articles matched your quality, but my guess is only 1% rival you today.

I guess you are the 1%! Congrats!

The graph shows more mid-tier phone launches over time, but the text implies there should be fewer over time as the high end become mid-tier within a year. Can you clarify this contradiction?

It shows a rise through 2012 and a precipitous decline in 2013 (even allowing for the fact that we are only five months into the year.)

I discounted the 2013 bar because we’re only partway into the year. I’ll take your word for it that compared to Jan-May last year, it’s a steep decline. The article could have been more clear on that point.

I keep forgetting that although Apple has had a 2 generations old phone available for zero dollars on contract for a couple of years now, this is the first year that they’ve had a zero dollar CDMA phone, and thus the first year that we’re seeing the impact of the Iphone at the low end of the contract market on carriers other than AT&T

Thanks for the excellent analysis. Today though NPD reported that prepaid is rapidly increasing in the US, up to about 32% share in 1Q13. Because prepaid US iPhones are sold from $650 down to $450 (some carriers include a small subsidy), the price range is greater, and I would think that mid-tier and low-tier phones do very well. Could Current Analysis perform and report on a similar analysis for US prepaid?

There’s obviously a limit to what I can share in free columns, but, yes, we have that data.

There’s no such thing as a free phone. With early termination fees starting at $350, and declining per month, even a “free” phone costs $350.

There’s no such thing as a free phone. With early termination fees starting at $350, and declining per month, even a “free” phone costs $350.

But wanna say that this really is quite helpful Thanks for taking your time to write this.

As I website owner I believe the content material here is really good appreciate it for your efforts.

Superb post however I was wanting to know if you could write a litte more on this topic? I’d be very grateful if you could elaborate a little bit more.