There are fascinating things afoot in the semiconductor industry, particularly in ARM’s ecosystem. For those who don’t understand how the ARM IP licensing works, I need to explain this to tie my overall point together.

There are two types of licenses a company can acquire from ARM. There is a standard ARM license, where you are given the IP and you take it to market under your brand, making little to no architectural changes to the chipset design. Companies like TI, Mediatek, and a host of other companies do this. It helps them get to market faster and use a standard set of libraries for fabrication.

The other license one can acquire from ARM is called an architectural license. This means you can acquire the IP and make some fundamental architectural changes to the libraries in order to differentiate your chipset from the market. Generally, companies who do this such as Qualcomm, AMD, Nvidia, Broadcom (even Apple is an architectural licensee) focus on more premium markets for their products. If you are going to spend the money to be an architectural licensee, develop your own custom chips on the ARM process, do R&D around the advancement of your ARM architecture, you certainly can’t justify commodity markets from a revenue perspective. Usually, offerings from an architecture licensee cost a bit more, due to the underlying economics involved in customizing a proprietary ARM process. It is this light that makes the latest ARM IP very interesting and potentially disruptive.

I’ve always watch the ARM ecosystem with a careful eye. Looking at the dynamics, it seems as though the ARM IP licensing model is inherently disruptive. There is an distinct trickle down flow of the IP that allows today’s highly differentiated and premium Qualcomm SoCs to be the standard in a generic ARM chipset next year. Meaning, the innovations Qualcomm, Broadcom and others invest in, essentially become the mainstream for their competitors in a matter of time.

During the first phase of mobile, this was not a huge issue. During the heyday of the PC, Intel had predictable performance gains that mattered on a regular basis. Their continued investment in R&D justified this. Similarly, Qualcomm benefited in two ways that made them dominant. There was the need for more performance, both in CPU speed and graphics, as the smartphone industry was maturing. There was also modem advancements which are still relevant today. In fact, the continued increase in wireless broadband is the performance measure that matters in today’s world, not graphics, cores, Ghz, or any other spec. Yet, when we look at ARM’s new IP there are certain implications to tease out.

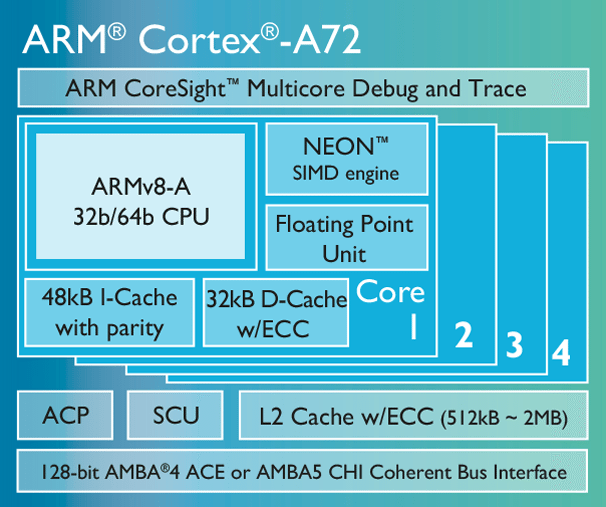

ARM announced their new A72 which is loaded with features. They are positioning this as the “standard” in premium mobile experiences. Note, this is a tagline Qualcomm would use for their chips. When you dig into the feature set, it becomes clear they have added nearly every major point a company like Qualcomm uses in terms of performance benchmarks for their premium chips. Except, ARM does not touch the modem, which is Qualcomm’s biggest advantage. But if we look at all of what I’ve just outlined, through the lens that the customers for premium parts like Qualcomm’s latest Snapdragon 810 is shrinking as I described on Monday, then we have to question the value of paying the fees and doing the R&D as an architectural licensee with where the world is heading.

Interestingly, Qualcomm showed shades of this as they embraced 64-bit. Rather than take their custom Krait architecture and spend the time and R&D to make it 64-bit, they just used the generic ARM 64-bit process and added some of their secret sauce to it to get it out the door quickly. They can still use their Krait architecture in new 64-bit processes but we have to ask, is it even worth it?

If Apple seals up the premium market and is the only real customer (by large volume) for premium components, then isn’t it logical ARM’s latest premium specs are good enough for the lower tiers? If this is true, then that means companies like MediaTek, or any other upstart branded CPU, can take premium features and make them mainstream at lower prices. So if the real market for Qualcomm or Broadcom or name-the-premium-SoC company, has to start focusing more on mid-range and the low end, then what happens to their premium feature focus and R&D?

This is why I feel the ARM IP ecosystem is inherently disruptive. The layering on top of the challenge to differentiate for an architectural licensee. I study the architectures and premium features of those companies and, looking over ARM’s latest IP, I have to ask if it is worth the effort. Especially when all the growth is coming from lower tier prices of smartphones, I’m not sure there are enough customers for premium SoCs to justify the R&D. Fascinating times in the semiconductor ecosystem and one that will make for some interesting story lines in 2015.

I don’t quite understand the relationship between ARM and it’s licensers, and I would appreciate it if you could help me.

In this article, you imply that standard ARM designs are for low- to mid-range devices. Qualcomm and others take that design and create chips for high-end devices. My first question is, is this intentional on ARM’s part, or is ARM somehow incapable of designing high-end chips?

My second question is, has this changed with the A72? Is it possible to create a high-end smartphone that can compete with iPhones, based on chips derived from a standard ARM licence? Or to compete with iPhones, do you still need to customise the ARM chips (which I think you are saying, but I’m not sure)?

It’s intentional. ARM would rather be the keystone owning the very top of the stack in a modular ecosystem than own the full stack like Intel. Less risk of being disrupted.

It hasn’t really changed with A72. As I read the move it seems to be a defensive maneuver to fill in a niche that would be left open if high end Android became marginalized. This goes back to the being the keystone in a modular system. They have the ability and latitude to read ahead and make such a maneuver without incurring greater levels of cost and commitment.

That’s very interesting, thank you. Sounds like ARM’s business model and their strategic choices are an interesting case-study in itself.

ARM is a licensing company. They create IP, which advances the architecture and allows chip vendors to adopt new IP advancements. This would be like Intel, developing a new process technology /architecture like 14nm for example, then allowing anyone to take it to market. However, with Intel being vertical they take their own IP advancements to market. ARM does all the work to build new libraries for SoC companies to take silicon to market. In this case ARM is simply building the next version, based on ARM v8 and support for 16nm and beyond.

I’m not saying ARM does not or has not built high-end chips, just that they have focused on a baseline architecture. Up to now we have not seen a non-architecture licensee really attack the high-end with a generic ARM chip. This has always been up to the licensee who has the resources to customize the chip with their secret sauce.

That is what has changed here. If you just look at the specs, it is not that far off from Qualcomm’s 810. So if ARM is giving their generic licenses like MediaTek, the ability to compete with Qualcomm on all levels then it gets very interesting. Especially, since MediaTek is not incurring all the RND and infrastructure costs to be an arch licensee, they could technically take this chip, which is competitive with Qualcomm’s premium chip, and offer it at lower prices.

The big caveat here is the modem. Qualcomm is still one of only a very small number of companies who has a globally certified LTE and backward compatible modem/SoC. Only Intel is the other. So MediaTek who has a modem, does not have it certified in every market. Samsung has the same problem, their modem can’t enter the US yet for this reason. They also likely have to pay Qualcomm a license to enter the US with a modem anyway. But that is not the big money win for Qualcomm. Qualcomm makes more money selling their own SoC. This is why what I outlined above makes things very interesting in this ecosystem.

Thank you. Got it.

Very interesting. Have to think it through…

It’s fairly symmetric w/ Android: ARM create IP on which to build a SoC/CPU *and* sell you an incarnation of that IP in a ready-made SoC/CPU; Google create an OS on which to build an ecosystem *and* give you an incarnation of that ecosystem via GMS.

I thought of that comparison as well, but im not sure that it’s relevant.

For example, with ARM, they actually encourage you to customize and create a better performing chip. That’s the opposite of what Google does; they persuade OEMs to adhere closely to their own guidelines. In fact, pure and plain GMS is what Google at least considers to be the best.

In as many ways as ARM and Android are similar, I think they are also opposites.

And it seems like high-end Android is marginalized. The part I think is interesting is how “premium” Android has essentially moved to the middle part of the price tier market. Meaning $300-$400 devices. This is what I think makes this A72 interesting. It means a non-arch licensee, not straddled with infrastructure and RND costs, can offer a premium class chip at lower costs than someone like Qualcomm. And its certainly good enough for this price tier.

Obviously the modem is still a differentiating factor, but I’m just not sure how long that lasts.

How do you define high end ? I’m confused between high-end, premium, luxury… Is it price-based (in which case it’s kind of a self-fulfilling prophecy), features-based (which ?), brand/line/model-based ?

Yes, this is getting tricky, I see what you are bringing up. I typically do this by price tier. Since I track device sales by price tiers first of all.

Then we can move to capabilities. This is too hard to define in a good enough world. So perhaps we move to experiences? so 4k capture, slow-mo, security, things that get commercialized in the high end experientially can fall into this tier. Trickier in a good enough world. But relevant when we look at what is a high-end experience and the market for truly innovative parts.

The issue with being price-based is that similarly-specced phones can get thrown into the high-end or mid-range bucket based on price only. For example, the Galaxy S5 is below $500/€500 now, the LG G3 below $/€400 does that make them midrange, while they were high-end at launch ? What about the 2nd-tier handsets with pretty much the same specs available for $100 less ?

I’ve got the same issue with specs-based, especially when the specs that make a phone high-end are not clearly stated. We can all agree on a high-res, low-light camera, but then ? DPI ? Screen size ? FM radio ? 4G ? SD slot ? RAM ? Storage ? Half of those will be irrelevant to most, the other half terribly contentious (to me, anything w/o an FM radio, a 24+hr battery and either 64GB or an SD slot isn’t high-end, not even mid range, just crippled, and that disqualifies all iPhones).

When I read “high end”, I mostly understand “iPhone & Galaxies S+Note”, which makes the whole thing meaningless nowadays, with <$500 phones being comparable, and Samsung losing as much to other brands as to Apple. I could understand "luxury", which means customers are paying as much for the brand as for the device itself (think Vuitton bags, Hermes scarves…) and a whitelist of "luxury" brand/lines.

The low or mid range positioning is a chicken and egg problem: because it’s ARM’s standard design, which will be adopted as-is by 80%+ of SoCs and phones, it becomes the mainstream, ie mid-range then low-to-mid a year later, by definition. It’s still 2x faster than last year’s core, so very high end by that standard…

At some point, labels confuse the underlying reality…

At least from my point of view, definition of high-end is pretty clear. I don’t define it as absolute performance, but by performance relative to the leader, which is likely to be the iPhone for a while. I don’t really care if performance is 2x what it is now because, I assume, developers will still come up with ways to consume that power in the near future.

Hence the question I have is what the performance of the ARM designs will be relative to the iphone. If it can compete, then that will define the high-end Android market, at least as I think of it. If it cannot, then there will be no high-end Android market.

2 issues

1- you’re comparing an SoC and a platform (SoC + OS + App). That fraught with issues, and those are compounded by the fact performance evolves differently in different tests. Looking at the latest Anand test ( http://www.anandtech.com/show/8701/the-google-nexus-9-review/7 ) , just for the application (not low-level, those are even more inconsistent) tests, the nVidia Shield is sometimes 2x faster than iPad, sometimes 3x slower. Which is high-end ?

2- You’re making high-end about performance. At least in the end product (the phone), we know that isn’t quite true, with features, brand and price also factors somehow. I think that applies to the SoC too, say an SoC that’s 20% slower browsing but can handle a 40 megapixels camera or last 2x longer might be considered higher-end.

That said, if we trust ARM’s and Google’s performance pre-announcements, depending on how fast Apple moves their needle on performance, the A72 has a shot at being competitive, extrapolating from current benchs.

1.

Both are high end. I think that’s pretty simple.

2.

Apple dominates in brand. Hence Android offerings have to be comparable at the very least in performance, otherwise they stand no chance at competing in the high end market. That’s why I’m focused on performance. Not because it alone is sufficient to be high-end, but because it is the bare minimum requirement.

I think you’re right about a certain level of performance being a minimum requirement. It’s interesting, obarthelemy (and klahanas to some extent) continue to deny that Apple products are premium or high end at all. That reality doesn’t seem to compute.

We just got the answer for the current gen: ARM A57 is at par with the A8 on the performance front: http://www.anandtech.com/show/8718/the-samsung-galaxy-note-4-exynos-review/8

And that’s with a not-yet optimized OS, pushing twice as many pixels (3.7 vs 2mpxels), and for $250=25% less money @64GB.

That is definitely encouraging. The first encouraging benchmark I’ve seen.

There still a few unanswered questions like why doesn’t Samsung use these chips in the major markets (of course there are modem issues, but I wonder why they can’t work around them). Hopefully the next Galaxy will provide some answers.

yes this is the point, I hope I sort of made, that the mid-range becomes the premium tier spec wise. But as I tease, out this has implications for those who spend massive amounts and need to commercialize those investments with higher-tier customers who will pay for premium components.

head to head spec wise, there is not a ton different between Apple’s SoC and ARMs. All the difference comes into the integration capabilities across the hardware, which they can do an no one else can. Hence a differentiated experience. But others things like Swift and Metal play into the differentiations in their designs they can leverage.

If you take as fact that Apple owns the premium market, then how could Qualcom invest in selling premium chips? There’d be no at scale premium buyer.

From this point of view ARM has done the obvious: getting its std SoC as competitive with Apple’s as well as it can.

Now Apple, of course, has been working under its architectural license on the A72 for quite a while.

What will Apple’s A9 relative performance be as it must be a turbocharged A72?

Something I think is very interesting to watch is if Apple embraces the benefits of big.little under this new architecture. When you dig into he A72 you see ARM did a number of optimizations both in performance and in low-power consumption if the big.little elements of the architecture are embraced.

Since it is an option, but one that seems to have clear perks with this new architecture over others, it will be interesting to see if Apple embraces it. Also, the continual knock I hear from semi experts, is Apple’s design’s team challenge to design low-power. So embracing and designing big.little into future A chips could be an interesting development with positive outcomes.

Thanks Ben,

Apple’s likely to improve its A8. I’d overlooked that Apple with its dual and triplet CPU cores is a continent away from Big.little A72.

This is a bridge too far for me, but could you hazard a guess about how the A9 will match up with A72 perf/battery wise? And what IP in A72 would likely be adopted in the A9?

Well they are likely only to take the primary cortex A72. They don’t need the graphics bits or other interconnects really. That is sort of why I’m intrigued on the possibility of them using big.little as a part of the standard design. Obviously this chipset is the second version on ARM V8 so efficiency is getting better.

In my briefing with ARM on this they highlighted the A72 gets a 50% power reduction over A-57 at 16nm process. So that is a baseline Apple can expect, however, with big.little they claim an additional 40-60% reduction on average workloads.

So already solid gains. Interestingly for the generic ARM community, and the devices that are not running A-57 today, those devices will see a 75% power reduction at 16nm. So major battery life improvements appear to be across the board.

Ben,

Apple had an opportunity to choose Big.little already. Do you think this next design will be so much better that Apple will abandon its own (until now at least) superior Ax dual and triplet CPUs?

I don’t think they will, but you seem to think that this Big.little is something very special that would even outperform Apple’s Ax SoCs.

So, the issue I had is I didn’t think big.little really that interesting given the last few architectures. I do feel it offers some tangible benefits this time around. So we will see if it is enough to appeal to Apple, but as I said, its been clear low-power has been an sticky point for them and designing for sub 1w is key for them going forward. So maybe this helps, but either way Apple needs to take the next step in low-power.

Also thinking about that this architecture may mean for Apple Watch in the future as well.

The CPU is around 15% of a smartphone’s consumption ( http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.395.5855&rep=rep1&type=pdf ). Getting a 50% reduction in that on a 10-hr smartphone means an extra 45 to 60 minutes. Nice, but about equivalent to 0.5mm extra width for a bigger battery. I’ll take 2mm extra width ^^

Well it’s no surprise, due to the subjectivity of the matter, that it all depends on what premium means? Premium performance? I don’t see Apple as “owning” that. Premium “experience” is more likely.

Yes I pointed that out somewhere in a thread below.

“I don’t see Apple as “owning” [premium performance]…”

In terms of performance, I believe Anandtech has measured significant premium perf in the A8 and A8x.

If some Android ARM chip is better which is it and has it shipped in more than a million phones?

I mean over time you will see various vendors claiming the crown. Right now it’s Apple, next year it will be someone else. This is good, competition raises everyone.

I agree Android has lagged.

So it seems like this is likely to hurt Qualcomm and help MediaTek et al, in the near to mid term. In the mid to longer term, it may hurt all of them as Shenzen is likely to be able to source fabbed chips with ARM’s higher end designs without having to go through MediaTek.

I guess the question would be to what degree does ARM want to cut Qualcomm and MediaTek out, i.e. can it gain more by broadening its non-arch licensees 5x as in the above scenario than what it loses from QCOM et al?

This development is probably good for Android, as having ARM take a stronger leadership role in developing ready-to-use high quality chips can help. That said, the price for these high-end chips could still be higher than what most Android OEMs want to or can pay, if Apple does continue eating the high end.

As for Apple, this development seems like a negative as it creates a new contender to keep Android SOCs competitive with Ax. But as you say, ultimately it’s the integrated package -how the SOC is integrated, how the OS takes advantage of it, how it interacts with or enables other high-end differentiated capabilities- that matters for Apple.

Thank you for great content. I look forward to the continuation.

This is my first time pay a quick visit at here and i am really happy to read everthing at one place