This week’s Techpinions podcast features Carolina Milanesi and Bob O’Donnell analyzing the CES 2021 digital trade show and the news and trends coming from it and discussing Samsung’s Galaxy Unpacked Event and the launch of their new Galaxy S21 smartphones.

Category: Android

Podcast: Qualcomm Snapdragon 888, AWS reInvent Conference, Android Enterprise Essentials

This week’s Techpinions podcast features Ben Bajarin and Bob O’Donnell discussing the debut of Qualcomm’s Snapdragon 888 chip and its potential impact on the premium smartphone market, analyzing the news on custom chips, new computing instances and new hybrid cloud options from Amazon’s AWS Cloud computing division, and chatting about the debut of Google’s Android Enterprise Essentials for simply and securely managing fleets of business-owned Android phones.

Podcast: Samsung Unpacked, T-Mobile 5G, Apple App Store, Microsoft-TikTok

This week’s Techpinions podcast features Carolina Milanesi and Bob O’Donnell discussing the announcements from the Samsung Unpacked event, including their new Note 20 and Galaxy Z Fold 2 smartphones as well as their partnership with Microsoft on software and gaming services, chatting about T-Mobile’s launch of the world’s first 5G SA (Standalone) network, controversies around Apple’s App Store policy and cloud-based gaming services like Microsoft’s upcoming xCloud, and analyzing the potential purchase of TikTok by Microsoft.

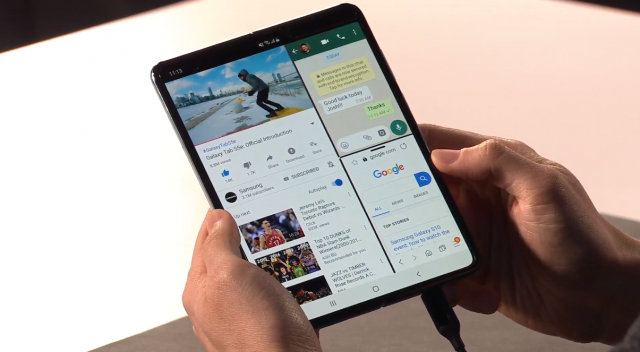

Samsung Galaxy Fold Unfolds the Future

I have seen the future. I have touched the future. I’ve experienced the future. And I love it.

How you ask? I’m one of the lucky few who has gotten to play for a few hours with the world’s first commercially available foldable phone, the Samsung Galaxy Fold (set for official release on April 26), and it’s amazing. The experience of looking at the normal-sized 4.6” front display on the device, and then unfolding it to unveil the same app in much larger form on the beautiful 7.3” screen is something I don’t think I will get tired of for some time.

But, it’s not perfect. First, at a price of nearly $2,000, it’s clearly not for everyone. This is the Porsche of smartphones, and not everyone can or will want to pay that much for a phone. Second, yes, at certain angles or in certain light, you can notice a crease in the middle of the large display when the phone is unfolded. In real-world use, however, I found that it completely disappears—it didn’t bother me in the least. Finally, yes, it is a bit chunky, especially compared to the sleek, single-screen devices to which many of us have become accustomed. However, it’s not uncomfortable to hold, and most importantly, it will still easily fit into a pants pocket (or nearly anywhere else you store your existing smartphone).

More importantly, the Galaxy Fold completely transforms how we can, and should, think about smartphones. Open up the phone and you’ll immediately recognize that this is an always-connected computer that you can carry in your pocket. Practically speaking, it lets you do all the digital activities we’ve grown attached to in an easier, faster, and profoundly more satisfying way.

Want to watch TV shows or movies on the go? You can’t get a better or more compelling mobile experience right now than what you’ll see on the Galaxy Fold. Looking for directions? Start your map search on the front screen of the device, then unfold it to display the entire area around your destination. It’s a revelation. Want to web surf, and chat, and check out social media at the same time? The Fold’s ability to simultaneously show three different applications in reasonably-sized windows—a feature Samsung calls Multi-Active Windows—matches the kind of experience that has required a large tablet or PC in the past.

I could go on, but I think you get the idea. The Galaxy Fold radically changes how we’re going to think about and use mobile devices, and frankly, makes most of our existing phones look a bit—no, a lot—old-fashioned. I realize it may sound somewhat hyperbolic, but I honestly haven’t been this excited about and fascinated with a tech device in a very long time…as in, since my original experience with a Sony Walkman (yes, that long ago). It’s the kind of device that makes you look at other existing products in a profoundly different way. Having said that, with a device this different, and this expensive, you’re going to want to try it out yourself to really see if it works for you.

While the Galaxy Fold is radically different from all other smartphones in some critical ways, it’s also important to remember, however, that it is, fundamentally, still an Android phone, with all that entails. For existing Android phone owners, this means that—other than a few, simple new ways Samsung has created to work with multiple apps on the large display—it works like your existing phone. App compatibility is supposed to be very good on the Fold—though there are some apps, like Netflix, that don’t currently support multitasking windows—but it’s still too early to tell for sure.

For iPhone owners who may be tempted to switch over to the dark side (and I’m guessing there could be a reasonable number of those with this new product), it does mean getting used to Android, finding a few new apps, and—if you can handle it—giving up the blue bubbles of iOS-only threads in your messaging apps. In exchange, however, you’ll get access to an experience that Apple isn’t likely to offer for several years. Plus, given the level of multi-platform application and services support that now exists, it’s nowhere near as big a concern as it used to be.

For everyone, you’ll get six cameras—including the same three-camera package of wide angle, telephoto, and ultrawide on the S10 series—two built-in batteries, and the ability to share your battery power with others. Inside the box, you also get a set of Samsung’s Galaxy Buds wireless earbuds that can also be charged with the power sharing feature.

There’s been an enormous amount of speculation and build-up around not just the Galaxy Fold, but the foldable smartphone category in general, with many naysayers suggesting they’re little more than a gimmicky fad. While on the on one hand, I can appreciate the skepticism—we’ve certainly seen more than our fair share of products that ended being a lot less useful than they initial sounded—I really don’t think that will be the case with Galaxy Fold.

In fact, looking back historically, I wouldn’t be surprised if the release of foldables is seen as being just about as important as the release of the iPhone. It’s that big of a deal. Of course, as with the iPhone, we will undoubtedly see several iterations over time that will make the current Galaxy Fold look old-fashioned itself. But for those of us living in the present and looking to the future, the revolutionary new Galaxy Fold offers a very compelling path forward.

Podcast: Google Cloud Next, Qualcomm AI Day

This week’s Tech.pinions podcast features Carolina Milanesi and Bob O’Donnell analyzing the Google Cloud Next event, including the company’s announcements around its Anthos multi-cloud offering, their AI-focused additions to GSuite, and the software-based, FIDO-enabled privacy key coming to Android smartphones, and discussing the data center and smartphone-focused AI announcements from Qualcomm.

If you happen to use a podcast aggregator or want to add it to iTunes manually the feed to our podcast is: techpinions.com/feed/podcast

Google’s Fading Focus on Android

Google is holding its I/O developer conference this week and Wednesday morning saw the opening day keynote where it has traditionally announced all the big news for the event. What was notable about this year’s event, though, was what short shrift Android – arguably its major developer platform – received at the keynote and that feels indicative of a shift in Google’s strategy.

Android – The First to Two Billion

One of the first things Google CEO Sundar Pichai did when he got up on stage to welcome attendees was run through a list of numbers relating to the usage of the company’s major services. He reiterated Google has seven properties with over a billion monthly active users but also said several others are rapidly growing, including Google Drive with over 800 million and Got Photos with over 500 million. But the biggest number of all was the number of active Android devices, which passed two billion earlier this week. Now, that isn’t the same as saying it has two billion monthly active users, since some of those devices will belong to the same users as others (e.g. tablets and smartphones), while others may be powering corporate or unmanned devices. But Android is a massive platform for Google and arguably the property with the broadest reach.

Cross-platform Apps and Tools at the Forefront

Yet, Android was given only a secondary role in the keynote, a pattern that arguably began last year. Part of the reason is Google has been releasing new versions of Android earlier in the year than before, giving developers a preview weeks before I/O and then fleshing out details for both developers and users at the event, rather than revealing lots of brand new information. But another big reason is a concession to two realities that have become increasingly apparent over time. First, Google recognizes it’s lost control over the smartphone version of Android, as OEMs and carriers continue to overlay their own apps and services but also slow the spread of new versions. It takes almost two years for new versions of Android to reach half the base. Second, Google also recognizes its ad business can’t depend merely on Android users because a large portion of the total and a majority of the most attractive and valuable users are on other platforms, mostly iOS.

Together, those realities have driven Google to de-emphasize its own mobile operating system as a source of value and competitive differentiation and, instead, to focus on apps and services that exist independently of it. As such, the first hour of Google’s I/O keynote this year was entirely focused on things disconnected from Android, such as the company’s broad investment in AI and machine learning, but also specific applications like the Google Assistant and Google Photos. No transcript is available at the time I’m writing this, but I would wager one of the most frequently repeated phrases during that first hour was “available on Android and iOS” because that felt like the mantra of the morning: broadly available services, not the advantage of using Android. As Carolina pointed out in her piece yesterday, that’s not a stance unique to Google – it was a big theme for Microsoft last week too.

Short Shrift for Android

But for developers who came wanting to hear what’s new with Android, the platform the vast majority of them actually develop for, it must have made for an interesting first 75 minutes or so before Google finally got around to talking about its mobile OS and, even then, not until after talking about YouTube, which has almost zero developer relevance. When it did, Android still got very little attention, with under ten minutes spent on the core smartphone version. Android lead Dave Burke rattled through recent advances in the non-smartphone versions of Android first, including partner adoption of the Wear, Auto, TV, and Things variants, and one brief mention of Chromebooks and ChromeOS.

The user-facing features of Android O feel very much more like catch up than true competitive advantages. In most cases, they’re matching features already available elsewhere or offsetting some of the disadvantages Android has always labored under by being an “open” OS, including better memory management required by its multitasking approach or improved security required by its open approach to apps. From a developer perspective, there were some strong improvements, including better tools for figuring out how apps are performing and how to improve that, support for the Kotlin programming language, and neural network functionality.

A New Emerging Markets Push

Perhaps the most interesting part of the Android presentation was the segment focused on emerging markets, where Android is the dominant platform due to its affordability and in spite of its performance rather than because of it. The reality is Android at this point, stripped of much of its role as a competitive differentiator for Google, has fallen back into the role of expanding the addressable market for Google services. That means optimization for emerging markets.

Android One was a previous effort aimed at both serving those markets better and locking down Android more tightly but it arguably failed in both respects. It’s now having another go with what’s currently called Android Go. This approach seems far more likely to be successful, mostly because it’s truly optimized for these markets and will emphasize not only Google and its OEMs’ roles but those of developers too. That last group is critical for ensuring Android serves emerging market users well and Google is giving them both the incentives and the tools to do better. I love its Building for Billions tagline, which fits with the real purpose of building both devices and apps for the next several billion users, almost all of which will be in these markets.

The Best Automotive Tech Opportunity? Make Existing Cars Smarter

Everyone, it seems, is excited about the opportunity offered by smart and connected cars. Auto companies, tech companies, component makers, Wall Street, the tech press, and enthusiasts of all types get frothy at the mouth whenever the subject comes up.

The problem is, most are only really excited about a small percentage of the overall automobile market: new cars. In fact, most of the attention is being placed on an arguably even smaller and unquestionably less certain portion of the market: future car purchases from model year 2020 and beyond.

Don’t get me wrong; I’m excited about the capabilities that future cars will have as well. However, there seems to be a much larger opportunity to bring smarter technology to the hundreds of millions of existing cars.

Thankfully, I’m not the only one who feels this way. In fact, quite a few companies have announced products and services designed to make our existing cars a bit smarter and technically better equipped. Google, T-Mobile, and several lesser-known startups are beginning to offer products and services designed to bring more intelligence to today’s car owners.

While there hasn’t been as much focus on this add-on area, I believe it’s poised for some real growth, particularly because of actual consumer demand. Based on recent research completed by TECHnalysis Research and others, several of the capabilities that consumers want in their cars are relatively straightforward. Better infotainment systems and in-car WiFi, for example, are two of the most desired auto features, and they can be provided relatively easily via add-on products.[pullquote]I’m excited about the capabilities that future cars will have, but there seems to be a much larger opportunity to bring smarter technology to the hundreds of millions of existing cars.”[/pullquote]

On the other hand, while fully autonomous driving may be sexy for some, the truth is, most consumers don’t want that yet. As a result, there isn’t going to be a huge demand for what would undoubtedly be difficult to do in an add-on fashion (though that isn’t stopping some high-profile startups from trying to create them anyway…but that’s a story for a different day).

In the case of Google, the company’s new Android Auto app puts any Lollipop (Android 5.0)-equipped or later Android phone into an auto-friendly mode that replicates the new in-car Android Auto interface. The screen becomes simplified, type and logos get bigger, options become more limited (though more focused), and end users start to get a feel for what an integrated Android Auto experience would be like—but in their current car.

The quality of the real-world experience will take some time to fully evaluate, but the idea is so simple and so clever that you have to wonder when Apple will offer their own variation for CarPlay (and maybe why they didn’t do it first…).

T-Mobile partnered with Chinese hardware maker ZTE and auto tech software company Mojio to provide an in-car WiFi experience called SyncUP DRIVE that leverages an OBD-II port dongle device that you plug into your car (most cars built since 1996). While several other carriers offer OBD-II dongles for no cost (you do have to pay for a data plan in all cases), the new T-Mo offering combines the WiFi hotspot feature with automotive diagnostics in a single device thanks to the Mojio-developed app.

Several startups I’ve come across also have other types of in-car tech add-ons in the works, many of which are focused on safety-applications. I’m expecting to see many compute-enabled cameras, radar, and perhaps even lidar-equipped advanced driver assistance systems (ADAS) add-ons at next year’s CES show, some of which will likely bring basic levels of autonomy to existing cars. The challenge is, the more advanced versions of these solutions need to be built for specific car models, which will obviously limit their potential market impact.

Car tech is clearly an exciting field and it’s no surprise to anyone that it’s becoming an increasingly important purchase factor, particularly for new cars. However, it may surprise some to know that the in-car tech experiences still lag the primary car purchase motivators of price, car type, looks, performance, etc. In that light, giving consumers the ability to add-on these capabilities without having to purchase a whole new car, seems to make a lot of sense—especially given the roughly decade-long lifetime for the average car.

Obviously, add-ons can’t possibly provide the same level of capabilities that a grounds-up design can bring, but many consumers would be very happy to bring some of the key capabilities that new cars offer into existing models. It’s going to be an exciting field to watch.

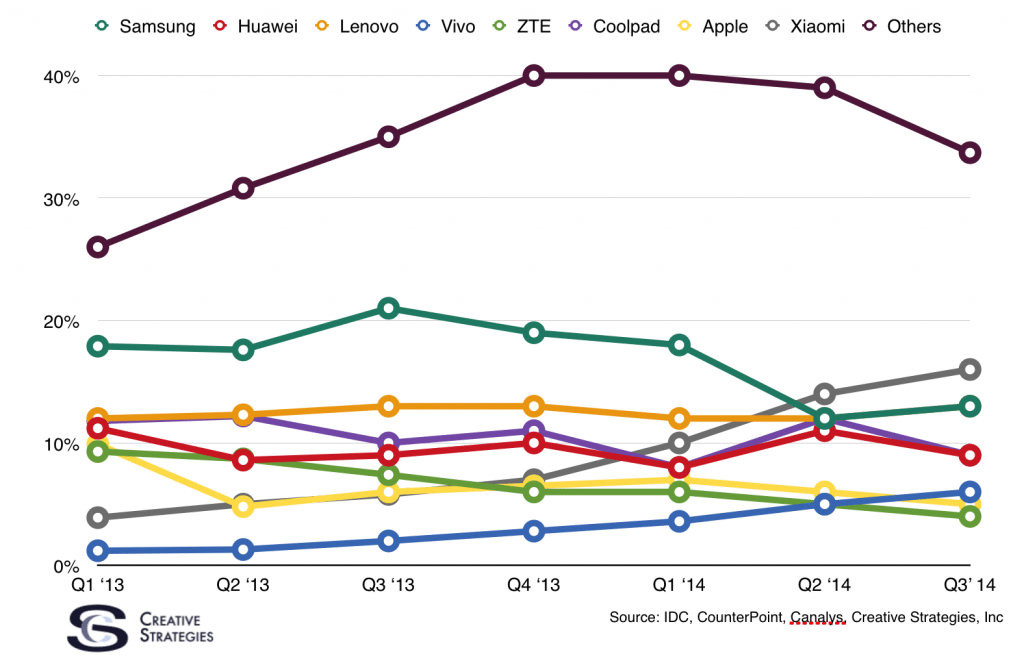

Samsung’s Challenges Reveal Need for Greater Vendor Diversity

Much has been written about how a debacle like the Note7 happened and what Samsung might do to repair its reputation. Samsung’s challenges also shed light on a unique fact about the U.S. smartphone market: the high degree of vendor concentration. Industry research houses show Apple and Samsung represent nearly 75% of smartphone share in the US (Apple about 45%, Samsung 29%) and about 90% of the profits. The remaining share is spread among several vendors, with LG at nearly 10% and Motorola at about half that. Concentration has been creeping up in recent years. Four years ago, the combined Apple/Samsung share was just under 60%.

The picture is quite different in other parts of the world. Globally, as of Q2 2016, Samsung was the leading vendor at 23%, Apple had a 12% share, Huawei had 10%, and all others had 55% combined, according to IDC. The vendor share picture varies quite dramatically by region and even by country. Chinese vendors Huawei and ZTE have made significant progress in Europe, having captured some 25%+ share between them in certain countries. China, the world’s largest handset market, is a veritable vendor free-for-all. Nowhere is the market as concentrated as in the US.

Why is this the case? Well, one factor is our iOS-centricity: Apple’s share in North America is some 2x that of just about anywhere else. We also like our flagship devices. Average selling prices here are among the highest in the world, and US consumers show a particular penchant for the ‘latest, greatest’ iPhone or Galaxy. Another factor is the strong role the carriers play in the US market. Many of their pricing promotions and ad campaigns are centered around iconic iPhone and Galaxy launches.

This fall’s handset developments have revealed why this might be a problem. First, Apple introduced the iPhone 7 which, although a terrific device, received mixed reviews. I am sensing a bit of Apple ennui, particularly among younger users. Sales have been pretty good but replacement cycles are creeping up. Then there’s the Note7 debacle. It is hard at this point to gauge the long-term damage to Samsung’s reputation and whether it will significantly affect the company’s market share. But this has been both difficult and costly for Samsung’s major customers in the US, the wireless carriers, who play an outsized role in distribution compared to operators in other countries. We learned last week that Samsung is offering $100 vouchers to consumers, among other measures, but little has been said about what Samsung is doing to repair its reputation with the operators.

I believe US operators and consumers are left vulnerable by this concentrated market. First, Apple has never been all that operator-friendly — in fact, it continues to do things in the crosshairs of the operators, such as last year’s move into equipment financing. Second, what if the next iPhone is a dud or gets delayed by a few months? Operators have become pretty addicted to that clockwork September iPhone launch to meet their 4Q numbers. What if Samsung’s supply chain and QA problems are more far-reaching? What are the fallback options?

The challenge other handset OEMs have had in capturing share in this market over the past several years is a bit baffling. LG, Motorola, and HTC, among others, make excellent devices. In segments of the market where price is more of a factor, such as prepaid and MVNOs, their combined share is proportionately higher. But they can’t compete with the gargantuan ad budgets of Apple and Samsung and the carriers just haven’t given them all that much love.

I’m surprised the operators haven’t pushed harder. Why are they leaving themselves so vulnerable to an Apple or Samsung hiccup? Why haven’t they put more pressure on pricing? Why aren’t they exerting more influence on the phone’s user experience? With a leveling off of smartphone growth and longer replacement cycles, I am a bit surprised at operators’ order-takery mentality on devices.

Perhaps this is why Google is taking a renewed and more vigorous crack at the handset business with the recently announced Pixel phones. It realizes the market is increasingly tilting toward ecosystems and software—areas where it can exert an influence as long as the hardware is good (which seems to be the ante needed to play in developed country markets). Consumers buy iPhones, in large part, because of the Apple ecosystem. There is no single torchbearer for the Android ecosystem or even a device that maximizes Android’s potential to deliver a fantastic user experience. So, Google is thinking that embedding Google Assistant into the Pixel, plus the ability for Pixel to integrate with other announced Google hardware, such as Home, Hub and even the fledgling Project Fi service, could be part of a next-generation ecosystem play.

Why would vendor diversity be good? As protection in case of an Apple or Samsung hiccup (or worse); a hedge against said vendors’ occasional arrogance; a lever on inflated prices; and as a spur for innovation. This would also give the operators more skin in the game—a position they had not so many years ago.

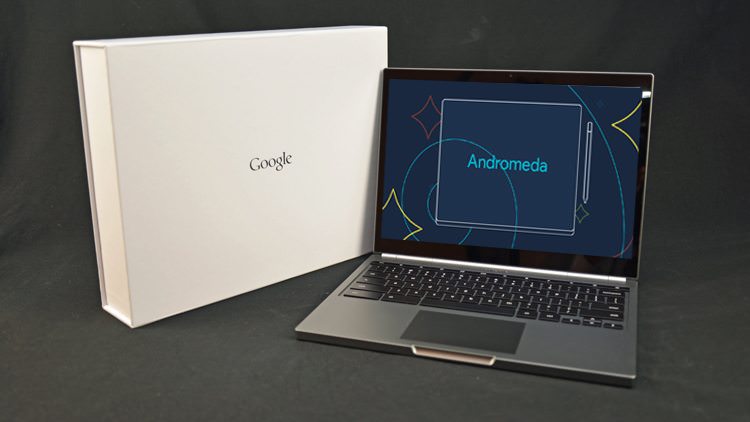

The Andromeda Strain

Veteran fans of thriller author Michael Crichton may recall that his career kicked into high gear with the 1969 release of a novel entitled “The Andromeda Strain.” The book described the impact of a deadly microbe strain delivered to earth from space via a military satellite.

Next week in San Francisco, Google is heavily rumored to announce the release of a new strain of operating system codenamed “Andromeda.” The new OS is expected to combine elements of Chrome with Android. Unlike current efforts to bring support for Android apps into Chrome, however, the new Andromeda OS is expected to bring some of the desktop-like capabilities of Chrome into Android to form a super OS that could work across smartphones, tablets, and notebook-style form factors.

Though details remain sketchy, the new OS is expected to offer true multi-modal windowing, as well as a file system and other typical accoutrements for a desktop-style operating system. In essence, this means that Google’s next OS—expected to be released late this year or sometime next year—will be able to compete directly with Microsoft Windows and MacOS X.

On many levels, the development of a single Google OS is an obvious one. In fact, I (and many others) thought it was something they needed to do a long time ago. Despite that, its impact is bound to be profound, and cause a fair amount of stress and, yes, strain, for users, device makers and developers alike.

For consumers and other end users, Andromeda will first appear as yet another OS option, because Google isn’t likely to immediately drop standalone versions of Android or Chrome OS after the announcement or release of Andromeda. Over time, as the transition to Andromeda is complete, those potential concerns will fade away, and consumers, in theory at least, should get a consistent experience across devices of all shapes and sizes. This would be a clear benefit for users, because they should have access to a single set of applications, consistent access to all their data, and all the other obvious benefits of combining two choices into one.

At the same time, however, the transition could end up taking several years, which is bound to cause confusion and concern for end users. Trying to choose which devices and operating systems to use, particularly as device lifetimes lengthen, could prove to be frustrating. Plus, if Google does move away from Chrome, as some have suggested, existing Chromebooks become relatively useless.

For device makers, Andromeda could represent an exciting new opportunity to sell new form factors, such as clamshell, convertible, or detachable notebooks running the new OS. They may also be able to create true “pocket computers” that come in a smartphone form factor, but offer support for desktop monitors and other peripherals, similar to Microsoft’s Continuum feature for Windows 10 Mobile.[pullquote]The launch of a new OS from a major industry player is always fraught with potential concerns, but the merger of two existing options (including the most widely used OS in the world) into a single new one heightens those concerns exponentially. [/pullquote]

Initially, however, Andromeda is going to be more of a challenge for device makers because of their need to deal with product categories like Chromebooks, that could potentially go away. Plus, like Microsoft, Google seems to be moving aggressively towards doing its own branded hardware products, and that takes away potential market opportunities for some of its partners. At the same time, the launch of a new OS with new capabilities and new hardware requirements seems like the perfect time for Google to make a serious play into their own branded devices.

For developers, Andromeda will undoubtedly prove to be a strain for a longer period of time because of their likely need to rewrite or at least rework their applications to take full advantage of the new features and capabilities that will inevitably come with a new OS. Plus, any confusion that consumers face about which version of the different Google OS’s to use will negatively impact future app sales and, potentially, development.

The launch of a new OS from a major industry player is always fraught with potential concerns, but the merger of two existing options (including the most widely used OS in the world) into a single new one heightens those concerns exponentially. As with Mr. Crichton’s book, the initial drama and tension are bound to be high, but eventually, I think we’ll see a positive ending.

Competition is Shifting to the High End

The consumer electronics industry has always fascinated me. I spent my first ten years as an analyst covering the telecom industry, which historically has had very good margins. But, when I started covering the consumer electronics industry, I was struck by the fact the vast majority of players in that market make razor-thin margins, if they’re profitable at all. Even more striking is Apple, which might be described accurately, if incompletely, as a player in the consumer electronics market, makes telecom-like margins while competing with those barely profitable vendors. And just as interesting is the fact that, as players that have historically only competed indirectly in the consumer electronics business enter it, at least some of them are choosing to follow Apple’s route to the high end of the market.

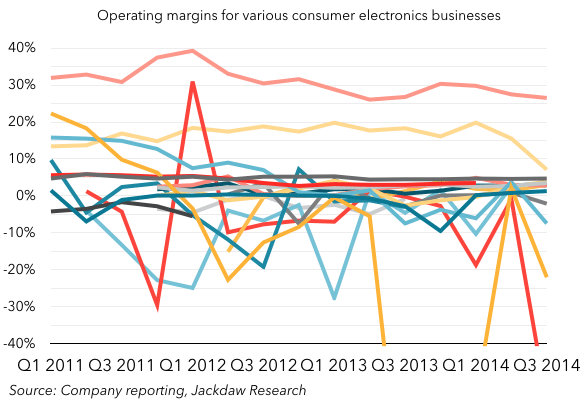

Historic consumer electronics margins are abysmal

It’s been quite a while since I updated this chart, but the broad picture it shows remains largely unchanged. It shows operating margins for most of the major companies in the consumer electronics business. The point isn’t to highlight specific companies, but to show the broad pattern of there are only two companies consistently above the 5% mark (Apple and Samsung) and Samsung was rapidly reverting to the consumer electronics mean (shown in yellow):

As I mentioned, Apple is the one exception to all of this, with between 25% and 30% operating margins during the latter half of this chart, while everyone else scrambles at 5% or lower margins. How does Apple achieve this distinction? Well, it’s due to a combination of factors but it’s probably best summarized this way: Apple provides premium products at a premium price, and is able to justify the premium through differentiation based on a tightly integrated approach to hardware and software.

Three new players: three different strategies

So far, we’ve largely focused on those vendors who make the bulk of their revenue from selling consumer electronics hardware. But there are three relatively new players in this business who have traditionally participated only indirectly in this competition and who are entering the computing hardware market (in its broadest sense) in new and interesting ways. Google and Microsoft have traditionally participated mostly by providing operating systems to hardware vendors, while Amazon has participated largely as a seller of other people’s hardware. Each of their strategies is unique and different but, with two of them, there’s an emphasis on the high end which I find interesting.

Look at Microsoft’s most recent hardware event: it announced the Surface Pro 4, a Windows tablet which starts at $899, and the Surface Book, a Windows laptop which starts at $1499. Both of those price points are well above the average prices in their respective categories and very much represent premium products. These (along with older versions of the Surface line) are essentially the only computing hardware products Microsoft sells, and they’re very much premium merchandise. In fact, the Surface Book starts at a higher price than the vast majority of Windows laptops on sale today and almost all the products announced by OEMs during the same period had lower prices. Microsoft is very much pursuing the same “premium product at a premium price” strategy as Apple and attempting to provide the same levels of optimization and integration as well (with mixed success).

Arguably at the opposite end of the scale here is Amazon, which has moved increasingly down-market with its tablet strategy. One of the reasons people were so surprised by the pricing of the Fire Phone was it seemed to fly in the face of the clear strategy Amazon had laid out with its tablet line: decent hardware at prices that undercut the competition. Since the Fire Phone launched, Amazon has lowered the prices for its low-end tablets even further and it’s increasingly clear this is the main focus of Amazon’s hardware strategy today. Yes, it has some “premium” devices too, but even these tend to sell at prices that fall much more into the mid-tier rather than the high end. I’m still unconvinced as to whether this is a good idea, as I’ve explained elsewhere, but there it is.

We come now to Google, who also had a hardware launch event this past fall and where its strategy was on display. Google’s approach has arguably been something of a mix of Microsoft’s and Amazon’s. Attacking the low end with devices like the Chromecast but also moving increasingly upmarket in the smartphone and tablet categories. There was no new Chromebook at this event but the only one Google has sold under its own brand so far is the Pixel, which retails at $1000, well above any other Chromebook. In smartphones, the Nexus line is an odd mix of Google branding and OEM manufacturing but even that line has been moving steadily up-market, while taking something of a cue from Amazon’s higher-end tablets, with premium hardware at discounted prices. But the product that perhaps signifies Google’s pursuit of the high end best is the Pixel C tablet, with high-spec and well-designed hardware, but at a starting price of $500, with an optional keyboard for another $150. In a world of cheap Android tablets, the Pixel C is as unrepresentative as the Surface Book is of Windows laptops.

The only Android and Windows vendors not struggling

Even though Google continues to pursue a low-end strategy with some of its own hardware, it’s increasingly clear that both OS vendors turned hardware vendors have decided to embrace the high end along with its high margins, while leaving the scale and the thin margins to their OEMs. Meanwhile, their OEMs continue to struggle to make the business work, with several exiting segments of the market entirely and several others clearly having a hard time staying afloat. Sony has abandoned PCs and continues to struggle in smartphones, HTC increasingly looks like it’s on its last legs as an Android vendor, Toshiba is considering spinning off its PC business, and Samsung’s smartphone business – once the poster child for success making Android phones – continues to slip. It sometimes seems as if the only vendors making Android phones and Windows PCs who aren’t struggling in some way are the licensors of the operating systems. And though we don’t have detailed financials for either company’s hardware business, they’ve both done it by focusing on selling premium devices at premium prices, and by tightening the integration between hardware and software.

What’s interesting is we haven’t seen any of the OEMs pursue this strategy. That likely reflects, in equal parts, a lack of capability and a lack of will, as these OEMs have neither the experience nor the desire to pursue the high end of the market. And yet it’s been clear for years that, while scale may be in the mass market, the margins are in the high end. These OEMs’ continued focus on the low end and mid-tier of the market, combined with their licensors’ focus on the high end, is likely to make life increasingly difficult as saturation and even decline begins to set in within the markets they serve.

How Apple Prompted Google to Create “Chromedroid”

News broke last week that Google was in the process of possibly merging Chrome and Android into what perhaps we should call “ChromeDroid”.

Although Google has not confirmed this (yet), Eric Schmidt’s recent comments at an event in Asia suggests this is likely. If you have read my columns in Tech.pinions recently, I have often suggested this was inevitable. Although Chromebooks have been successful in education, their lack of an apps ecosystem made it unlikely Chrome would be Google’s long term OS beyond its use in this vertical market.

I have also argued Apple’s iPad Pro, with its iOS operating system, would be targeted at business users and upper-end consumers and that Apple would make iOS the cornerstone of a broader push into business. As Tim Cook stated recently at the last launch event in San Francisco, “People can do 80% of what they need to do in iOS” — regardless of whether it is used for business or consumers’ needs. One of the more interesting facts about iOS is this is the OS Gen Z, Gen Y and younger Millennials cut their teeth on when it comes to their introduction to personal computing. It seems logical that, when this younger generation goes into the business world, they could or would want 2-in-1s or even laptops running iOS instead of being forced to use Windows or even the Mac OS X. Ironically, I was told recently that, to some of this younger generation, Mac OS X is now considered “their parent’s OS” in the same way the Mac generation of users referred to Windows in the past.

Using this logic, it is reasonable to ask the question of whether Android could also be the OS a portion of this younger generation wants to take with them into the business world? Although iOS dominates as an OS for most millennials in our country, Android actually outsells iPhones around the world. Many Gen Y and Gen Z, even in the US, start their computing journey on Android instead of iOS. Would they, like their iOS counterparts, prefer more powerful Android tools to take with them into the corporate world? If this happens, it seems this move could be highly influenced by Apple taking iOS mainstream. Depending how they craft these merged operating systems and their ability to scale to things like 2-in-1s and laptops, it will determine if Google will be competitive beyond smartphones in the future.

Google seemed hellbent to make Chrome OS their desktop and laptop OS and push this Web-based OS to be the one that transcends their tablet and smartphone Android platforms. But there is one problem with this. What makes iOS and Android so appealing is that each has over 1.5 million apps in their stores and Gen Z , Gen Y and millennials crave the versatility an app ecosystem gives them. Add to that the fact these operating systems are the ones they use day in and day out with a plethora of apps that meet pretty much every digital need they have and you can see why taking their mobile OS of choice to larger form factors in the business world makes sense.

With the iPad Pro (and a potential MacBook with iOS on it some day), iOS could be the enterprise OS of the millennials. Apple seems to understand this well. The new iPad Pro as a 2-in-1 makes it easy for this demographic to go from their current mobile first approach of using technology to making it possible for them to use a powerful new mobile form factor with the same OS in their jobs. Couple this with next generation iOS applications, such as the apps IBM is creating for iOS, why would they want or need to move to Windows if they can do the same tasks as powerfully and efficiently on iOS in a 2-in-1 form factor or lightweight clamshell?

It is clear to me Google realizes what Apple is doing with iOS and that Chrome would not cut it with this younger generation who want greater flexibility and versatility in the devices they use. While I doubt they’ll completely abandon Chrome, since it is getting serious traction in education due to its low cost and Web-based curriculum being designed for it, I am saying Google now sees that, for this younger generation, Android may need to be able to move out of its smartphone and tablet confines and into new designs that are more acceptable for use as a business tool when this younger generation moves into Corporate America. Merging Chrome and Android does this.

This is not a knee-jerk reaction to Apple’s iOS strategy, although I think Apple’s recent moves pushed them to do this sooner rather than later. The merger of Chrome and Android has been coming for some time. Google has stated they want Android apps to work within Chrome. It’s a good idea but, with Chrome being grounded in HTML, it does not provide the level of flexibility Android users want in various form factors. Merging the two and using Android as the core OS for cross-platform and cross-device implementations keeps them competitive with Apple and Microsoft.

Google has not publicly clarified the merger of Android and Chrome but I can’t see them doing otherwise if they want to stay relevant in a fast moving world where mobile is driving the future of technology.

Is it Time for Apple to Open the Apple Watch to the Android Crowd?

We now know Apple has done well with the Apple Watch and that it outperformed the iPhone and iPad in terms of units shipped during their first 9 weeks on the market. However, they are doing these strong sales with the watch only connected to the iPhone. Of course, this makes sense. If the watch becomes popular and only works with an iPhone, it could cause many users of other smartphone operating systems to switch. Also, it creates great incentives for those who want the Apple Watch to buy or upgrade their current iPhones too. Strategically, this move to have it only work with the iPhone is important during the Apple Watch’s initial roll out.

But I have an interesting question about the Apple Watch’s future. Is it, strategically, a side product to the iPhone to help sell more iPhones or was it created to also be a viable standalone product with its own profit potential and market impact? It is clear that, at least initially, it’s designed to help sell more iPhones and, since the iPhone is Apple’s real cash cow, one could argue it needs to continue to be a side product to the iPhone in order to help boost sales of the iPhone itself.

However, if you listen to the rhetoric from Tim Cook and Jony Ive, it is actually a piece of well-designed fashion jewelry and should be thought of in that context too.

On the surface, this seems contradictory since it would be hard for Apple to push both positions and still do the Apple Watch justice due to its great design and place in the fashion world.

Apple actually has a precedent for supporting other operating systems with mobile devices. When the iPod came out, it only worked with the Mac. It was basically a “side loaded” device in that you had to connect to the Mac to get the music downloaded to the iPod. The iPod sold well but its audience of users was small since the Mac had only about 4% of the PC market at that time. In those early days, it did influence some to buy Macs so they could use an iPod but to really deliver the type of audience they promised the music industry to help save off piracy, Apple clearly needed to expand the iPod’s audience. To do that, they made it work with Windows-based PCs and that is what really made the iPod a mass market hit. Interestingly, they did this so well they basically dominated the market for mobile MP3 players and, even now, nobody has been able to compete with them in the dedicated MP3 player market.

Over time, as the iPhone included all of the functions that were in an iPod, demand for the iPod decreased. Only recently has Apple refreshed the iPod line as there is still interest, albeit small, for a dedicated mobile MP3 player tied to a great music store and app ecosystem. However, if Apple does want the Apple Watch to have a real impact in the marketplace and change the market for smart watches, they eventually need to open the Apple Watch up to those who use Android. A few weeks back, I wrote a piece that suggested Android is the new Windows. For the Apple Watch to reach its real potential as the game changer Apple wants it to be, it needs to have a broader audience than just iPhone users.

But the question is, will Apple do this and if so, when? Put yourself in Apple’s position. The iPhone is a global success that continues to grow and bring a huge amount of cash and profits to Apple, not unlike Windows was to Microsoft in the past. But, unlike Windows, Apple owns the hardware, OS, software and ecosystem which gives them tighter control. More importantly, they also control the channels. The iPhone drives their profits and, with each iteration of the iPhone, they seem to get more and more switchers and followers. But this also presents somewhat of a dilemma in that they have positioned the Apple Watch as a tech and fashion game changer and suggested that everyone will want an Apple Watch. But to achieve that goal I have to believe, at some point, they must make it compatible with Android and perhaps even the Windows Phone if they want the Apple Watch to have the global impact they hope it will have.

My personal guess is Apple will keep it proprietary to the iPhone for at least the first 18-24 months but eventually make it compatible with at least Android in order to help them gain the kind of impact they desire and allow it to be a broader industry game changer. Yes, there will be Android smart watches coming out that could rival the Apple Watch. But even so, if Apple made their watch compatible with Android, I am willing to bet they would get the lion’s share of the smart watch market. Their styling and channel make it hard to compete and the Apple Watch would be a big hit with those users too.

Is Android the New Windows?

For most of my career as a PC analyst, I have followed and chronicled the evolution of the PC. My first project when I came to Creative Strategies was to work with a new group formed inside IBM that created the original IBM PC. By the time I was asked to be involved in some design strategies and retail projects, the IBM PC had just become a hit and was in the process of solidifying the role of a PC in business.

A short time after the IBM PC became successful, clones started hitting the market. The most successful one of its day was the Compaq computer. I was privileged to attend the first ever Compaq analyst event in which all (four) PC analysts at the time were invited. In the early days of the PC, there really weren’t any PC analysts per se and those who had the title had been covering mini-computers — PCs were added to our research roles.

During the visit we spent time with Compaq Chairman Ben Rosen and Compaq co-founder Rod Canion to learn about their new PC clone and why they thought they would be successful. IBM had become a force with their PCs and I found it curious an upstart like Compaq would even challenge them. In fact, I asked Rod Canion during that visit why he decided to put up his own money and go after funding to take on IBM. He told me when he was at Texas Instruments, he learned early on that whatever IBM did, it would become a standard. He saw the success of the IBM PC and understood it was created with off the shelf parts and placed what he called a “sure bet” to create a competitor, knowing full well that IBM’s PC would become the standard for business computing. Not long after, Dell and others brought out clones too.

However, the one constant for all of these computers was an OS created originally for IBM known as MS-DOS. Since it was not proprietary, it was also licensed to Compaq, Dell, Acer, and about a couple of dozen other PC vendors in the heyday of the PC. MS-DOS eventually became Windows and this OS has been dominant for PCs and laptops for over 30 years. Of course, Apple created a computer OS for the Mac but Apple’s OS is proprietary and, even though it has done and is still doing very well, PCs running Windows out sell Macs exponentially.

It is interesting to note that, for most of Windows’ life, it was a local PC and laptop OS but Microsoft had visions of this OS becoming a standard for use in tablets and smart mobile devices as early as 1990. However, due to a lot of infighting inside Microsoft and a huge emphasis on productivity, they were never able to really establish Windows as a dominant OS beyond the PC. This opened the door for Apple and Google to create new operating systems designed just for mobile computers and IoT.

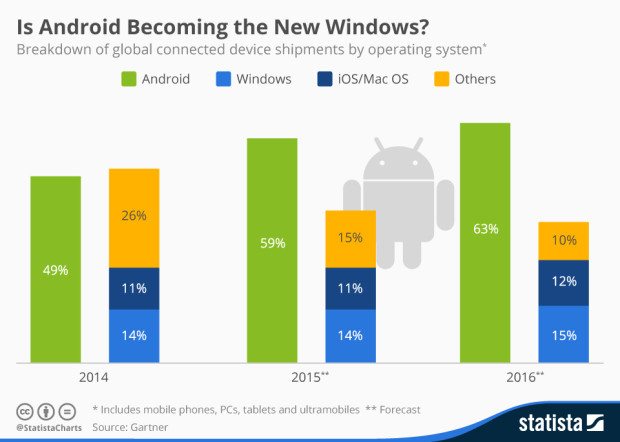

While Apple’s iOS is a huge success in its own right, like OS X, it is proprietary and used only on Apple products. On the other hand, Android has a lot of the original characteristics of Windows in that it is a licensable OS that can be used by any PC, tablet, smartphone and IoT vendors in the world. Indeed, if you look at the number of mobile devices on the market today running Android, it makes up about 75% of all products shipped.

At Googles recent I/O developer conference, Google’s leadership clearly stated they want Android to be the dominant OS for connected devices and IoT. Like Windows, Android is hardware agnostic and can easily be applied to any mobile or IoT device. Even more important is that Android serves as Google’s OS/UI to their overall cloud vision and are building most of their worldwide ecosystem of products and services channeled through Android.

Almost from the beginning, Bill Gates and Microsoft wanted their OS, and especially Windows, to be dominant on devices around the world. I still see that as their goal but, due to various choices and infighting, they are far behind Google and Apple in this quest — I don’t see that Windows outside of the PC could ever become a dominant device OS worldwide. Apple, with their proprietary approach, has made major strides in their quest to dominate the device market and with the iPhone, iPad, HealthKit, HomeKit, Car Play, Apple Watch and Apple TV they have emerged as a serious powerhouse of their own in this space. However, while in the past their main competitor was Microsoft and Windows, this time it is Google and Android and Android has become the Windows of our generation.

The big difference between Microsoft and Google is Microsoft still has to protect their legacy devices as well as try and move everything to their One Microsoft strategy. That is not easy to do. When it comes to mobile devices, their Windows mobile phones are a very distant third in the overall market of smartphones. As for IoT, iOS and Android clearly have an edge and momentum over Microsoft. Market projections from most research houses see Android basically dominating the market for mobile and IoT because it is device agnostic and is a free license for anyone that wants it.

From where I sit, it really does seem Android is the Windows of our day and Google is in a place to broaden their lead in mobile and IoT barring any serious missteps. Apple will be a worthy competitor and I don’t expect Microsoft to rest on their laurels and let Google dominate this space without a fight. However, Android’s lead in these two markets is quite huge and, if Google keeps moving in this direction and keeps their customers happy, I suspect Android, at least from a numbers viewpoint, will continue to be the dominant mobile and IoT system for many years to come.

The Electronic Car: Today and Tomorrow

What is an electronic car?

To some, it’s the model of the future, the complete electrical car with the Tesla as the winner. For some, it is a car with improved electronic entertainment and information systems. Another view is that, while petroleum may power most engines, nearly everything in the car, from fuel injection to tire pressure, is monitored and controlled by dozens of computerized electronic systems.

The day of dominant electric powered cars will come but it will take years before prices fall and the availability of battery charging sites rise enough to dominate the market. And despite speculation, it seems unlikely Apple or Google will become major players in the field. For now, this is an important but fairly small piece of the car market and one where no one has figured out how to earn money.

Information and entertainment is a much hotter area. The field consists of two different systems. Microsoft tried to get away with its plan to combine both the control of the gear in the car–audio, maps and routing, displays, and all the gear–and the system that receives and plays locally stored and wireless content. After years of struggling effort, with Sync as the most recent version, Ford has dropped Sync and Microsoft has largely left the field. Instead, the two sections have been split.

Where QNX came from. QNX, a service based on a real time operating system, appears to be the leader. Oddly enough, QNX is a unit of BlackBerry, which had bought it as the source of an operating system for its new, and unsuccessful, family of smartphones. Support of auto systems came along with the deal and may now be one of the few sources of profit for BlackBerry (the company’s statements do not include details). This system is critical yet effectively invisible to users. The system controls the entertainment and communication equipment built into the car including amplifier and speakers for music and voice, microphones, and a dashboard display.

The stuff that shows up in the car is getting the attention. Both Apple and Google are moving aggressively with Apple CarPlay and Android Auto with deals with car makers. These approaches, which are more than a little similar to each other, consist of an app installed on a relatively recent Android phone or iPhone ((Apple CarPlay supports all phones since the iPhone 5. Android has not yet specified which phones will comply with Auto.)) and assume support, such as QNX, built into the car.

The phone links to the car system with Bluetooth and can be controlled by voice, touch of dashboard screen, or built-in knobs and buttons. Content includes music–either on the phone or available through services–maps and navigation, phone calls, and messages. At this point, they do not support video; this will probably come eventually for rear seat video, but they are going to need guaranteed safety.

Fast growing service. The vehicle systems are appearing now and will become standard in cars. Both Apple CarPlay and Android Auto have arrangements for support from most U.S., European, Japanese, and Korean companies. Each has a list of about 30 companies with relatively few differences, the major one being both Mercedes-Benz and BMW support Apple but not Android.

Of course, Apple CarPlay and Google Auto will only work on new cars. But there is a way to add the function to existing cars. Pioneer’s high-end, display-equipped systems will support Apple and Google. Similar systems from Alpine support CarPlay, though Android support is probably coming.

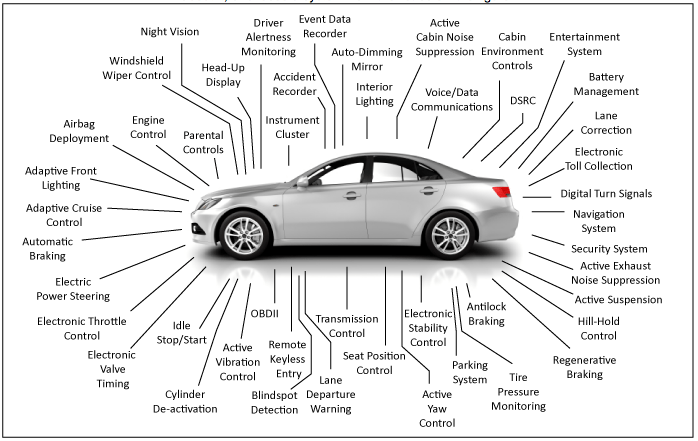

The many, many systems in a car are a complex story for the future. The drawing from the Clemson University Vehicular Electronics Lab shows more than 50 units, many including a computer of some sort. Some, such as airbag deployments and windshield washer controls, are independent. Others, such as automatic and antilock braking, have to work together though they may not be connected.

Getting components together. The next challenge is getting these components to work together. Many of these functions will be much improved if they can communicate and work together far more efficiently. But everything has to be done right and nearly everything has to pass government inspection.

The long term game is for all of those car components to become part of a network of an Internet of Things. With IoT, the devices will be able to communicate with each other and control each other as allowed. They will be able to send information to both internal car controls and also to sensors and control centers outside the car. But this is a very complex job, both technical and legal, for this system and it will take years to be completed. Gartner, for example, projects that 250 million cars will include some IoT components by 2020, probably a reasonable estimate.

I suspect this is a computer industry that computer and software companies are unlikely to dominate. Apple and Google may be interested, but it is a very tough business for them–and one the auto makers will not want to see them run. I suspect most of the moves will be made by car makers themselves, in cooperation with technologists like Intel and Texas Instruments and auto specialists such as Siemens and Bosch.

Samsung Pay May Add Opportunity — or Confusion (ADDITION)

Someday, sooner rather than later, we’ll be using our phones instead of credit cards for all our purchases. But the big question as the technology spreads today is are we — customers, merchants, finance companies — getting into a field that is better or worse for us?

Someday, sooner rather than later, we’ll be using our phones instead of credit cards for all our purchases. But the big question as the technology spreads today is are we — customers, merchants, finance companies — getting into a field that is better or worse for us?

The latest move came from Samsung, which announced at the Mobile World Congress the new Galaxy S6 phones that feature a service called Samsung Pay. It will let you use the phone to pay for purchases by holding it near a receiver at a store and touching your fingerprint to the phone.

Sound familiar? Samsung’s move is similar in more than name to Apple Pay, though it has some different functions. There’s also Google Wallet. And if you are really confused by the names, Google’s Sindar Pichai has announced Android Pay, which is quite different. It’s an API that allows developers to build a credit card payment function into Android apps. (We won’t bother discussing an app called Samsung Wallet in Google Play.)

PayPal enters. And there’s more. PayPal announced it has just bought Paydiant, a builder of mobile payment software specifically for retailers that use their own credit cards. And, of course, there is still the CurrentC plan, backed by big retailers, that will allow a phone to make a credit card purchase with a QR image that appears on the screen. CurrentC was built on Paydiant software and anything PayPal does is likely to have much in common with CurrentC.

Five separate apps on two different approaches are not all going to make it. For Samsung, the big question is what Samsung Pay–the company’s choice of the name showed off its lack of imagination once more–will accomplish. Samsung moved quickly after Apple’s launch of Apple Pay by using the software programming on LoopPay, which Samsung acquired just last month. The design depends on EVM and NFC semiconductors, just like Google Wallet and Apple Pay. [pullquote]For Samsung, the big question is what Samsung Pay–the company’s choice of name showed off its imagination once more–will accomplish.[/pullquote]

Samsung Pay will be available immediately on the Galaxy S6, although Samsung’s announcement did not made it clear whether it will be pre-loaded on the phones or left to be added to S6s through Google Play. Samsung left a mention of Pay out of its preliminary web site promotions on the Galaxy S6, while Apple and Google both promote the credit card offering. If Samsung steps up its promotion, it could easily become more popular than Google Wallet, at least among Galaxy customers with whom it has never promoted the Google offering. Samsung claims it also provides additional security protection through its KNOX mobile security, a potential match for Apple and advantage over Google.

Samsung’s finance interest. Samsung has some support from credit finance companies and retailers, but its position seems some distance behind Google Wallet, let alone Apple Pay. Visa Jim McCarthy, executive vice president of Visa offered a tepid endorsement: “Mobile commerce just got a lot more interesting. Combining Visa’s expertise in payment technology with Samsung’s leadership in creating innovative mobile experiences, gives more choice to financial institutions who want to enable their customers to pay by phone.”

It does seem unlikely that five rival systems will all survive. A grouping into two rival systems seems more likely–Apple, Google, and Samsung combining on the one hand and CurrentC and PayPal on the other. Apple Pay, Google Wallet, and Samsung Pay have significant design differences, but they are very similar at their cores. A critical question remains whether Apple, which has by far the deepest relationship with the credit card industry, wants to control the effort through a union of some sort or whether it wants to keep Apple Pay limited, as it now is, to iPhones.

The roles of PayPal and CurrentC is more obscure. The purchase of Paydiant means PayPal owns the technology behind the design of CurrentC, but commonality beyond that isn’t clear. While the approach is not tied to hardware requirements like the competition, it does not provide the security or ease of use. What it has going for it is mainly distaste for Apple and for banks in the retail industry, but that could offer some success.

———

ADDITION: Though Apple Phone was blamed for the use of fraudulent cards, the error was the fault of banks, not Apple, and was as likely to go on with the Google or Samsung apps. The problem was that banks were accepting the registration of credit cards stolen, including some of the big card thefts. The problem was a lack of proper checks before registering the card accounts and the banks are now toughening it,

A Deeper Dive on Android and iPhone in China

I’ve received a number of questions from readers about why I don’t talk as much about the US market for smartphones. It’s primarily because the US doesn’t offer any new interesting questions or problems. It’s about a 50/50 split between Android and iOS and Apple controls over 60% (and growing) of the premium smartphone space. iOS is on track to gain share into Android’s each quarter of 2014 and it will likely be more of the same in the US in 2015. However, other markets like India and China pose much more interesting questions and problems to be solved. I’ll do a few deep dives on the US market with some of our updated data sets, but what we find will likely not contain major surprises. Now, onto the iPhone and China.

First, Android Context

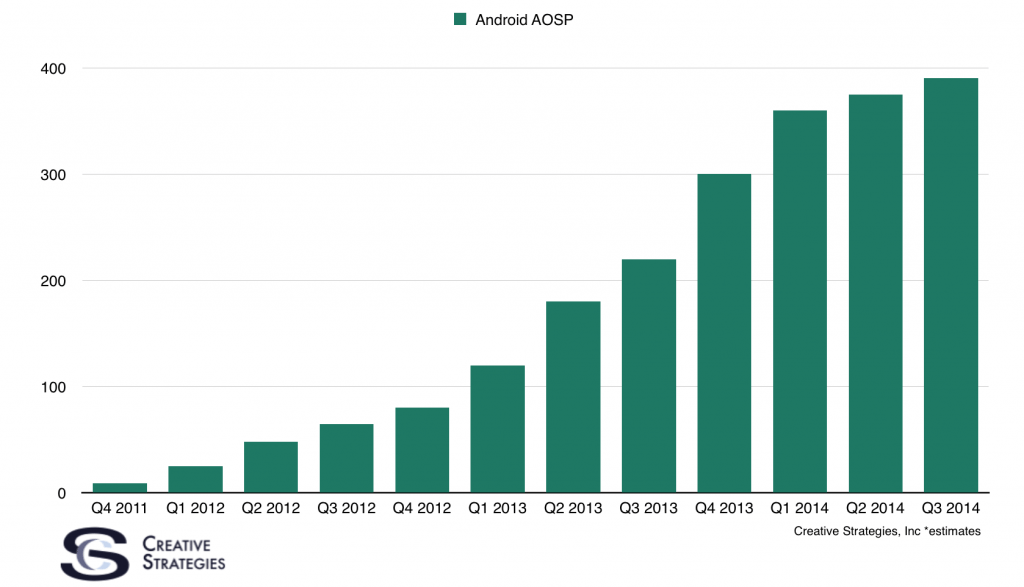

A fascinating data point came from Baidu yesterday. Baidu, the largest browser in use with an over 80% share in China, reported to Tech In Asia that they count 386 million active, individual Android customers. This is Android AOSP, not Google-approved Android, and a few things are unclear about the numbers. First, it is uncertain if these are smartphone-only owners. The report simply states active Android devices. Given China runs both AOSP on smartphones and tablets sold there, either device connecting to the Internet and accessing Baidu’s search engine would be counted. Through my supply chain checks, I learned that, on average, about 20m low cost Android tablets are sold in China each year. As I have discussed before, most of those are used simply as portable media players and large percentages likely do not connect to the internet. Which means, while some of the 386m active Android devices are tablets, the majority are smartphones. ((Even if the report said they were all smartphones, I would still believe a small percentage were tablets since my research there found that even 7-inch tablets in China use smartphone components; therefore they show up in analytics as smartphones.))

Baidu similarly reported last year a total of 270m active Android users. So there is impressive growth for AOSP. For some time now, I have been building a model of AOSP’s growth in China and was pleased to see Baidu’s data for Q3 2014 matched very closely to my own model.

You’ll note growth is slowing, as is the China smartphone market in general. There is certainly more growth to be had as more of rural China gets online, but these will mostly be with very low cost smartphones. Where things start to get interesting is when we look at the nearly 400m Android AOSP customers in light of the total smartphone user base. A number of Chinese research firms like iResearch China and analytics engines like Baidu/Umeng came out and said over 550m smartphones were in use in China by the end of June of 2014. My model would estimate that number to be around 575m as of today. Now we turn to the iPhone.

All local app analytics sources I have access to in China, and major network statistics I see, show Android and iOS as the two dominant smartphone platforms. So, if ~386m of them are on Android, then the iPhone fills most of the gap between 386m and ~575m. Based on my model, I had estimated iPhones were likely in the 130-150m range and I have believed for some time there were more iPhones in use in China than the US. It seems Baidu’s data is confirming much of what I thought my model was suggesting was true.

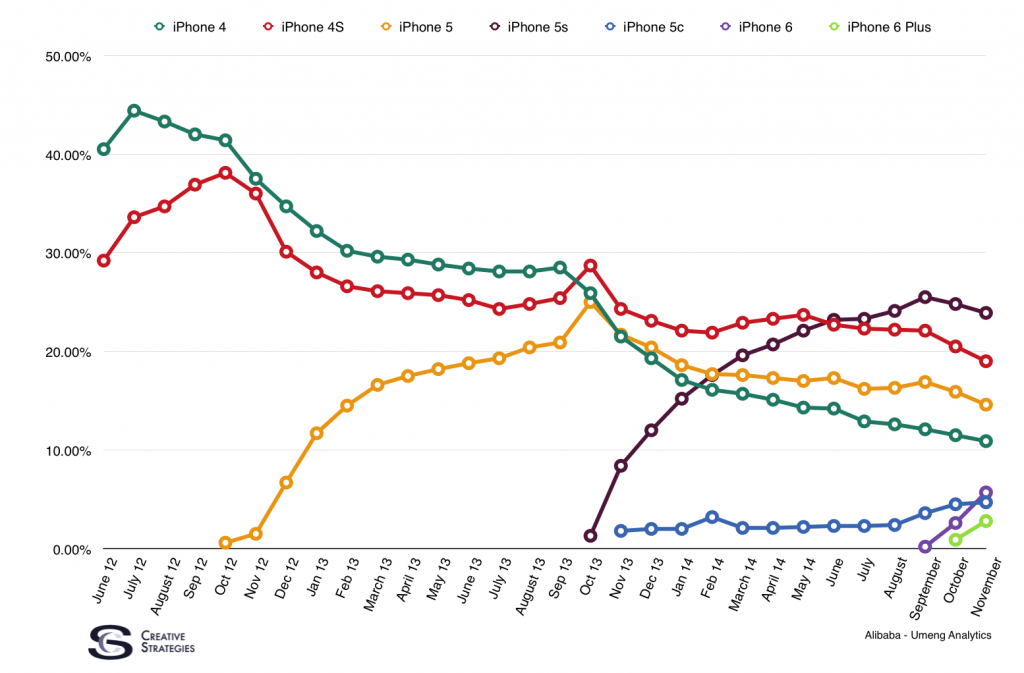

However, the bulk of that iPhone active installed base is on much later generation hardware sold through the grey market. This chart is the most updated data — now containing a a month and a half of iPhone 6/6 Plus availability. Keep in mind iPhone 6s starting showing up in September in this data because of grey market imports.

As Apple offers more models for sale in China, we are seeing the continued rise of primary market sales of iPhones. There remains a large installed base of later generation phones but, as you can see, it is actually more of a mix than domination by a few models. This data comes from Baidu’s app distribution network so it does not cover the entire market but it does cover over 100m devices. I can’t imagine the picture is much different on other app distribution platforms.

What I’m left thinking about is what will happen with the large percentage of current iPhone owners who are using later generation iPhones they bought from the secondary market for prices around $300-$400. It is hard to believe every one of those owners can afford a $700 phone but will they stay in the Apple camp and get another later generation phone like the 5s? Or will they stay in their price range and go with Xiaomi? These will be interesting questions for most of 2015. However, once the current iPhone 6/6 Plus gets discounted in China when the iPhone 7 comes out, I think Apple’s offering in China will be very competitive.

Lastly, it is worth pointing out the China smartphone market is unlike anything out there at the moment. Much of it has to do with WeChat. WeChat is undeniably functioning as an alternate or “para” operating system that runs on iOS and Android. As I look at what lock-in Android AOSP, or Xiaomi’s Android skin, or Apple’s ecosystem has, I observe the true lock-in in China is WeChat. Apple has the benefit of playing as a luxury brand; status is a huge part of their lock-in in China. But as this financial analyst correctly points out, we are hoping to see Apple continue to create more services/cloud lock-in rather than just status. Services like UnionPay integration will help with this but Apple’s services stickiness in China is a story to watch.

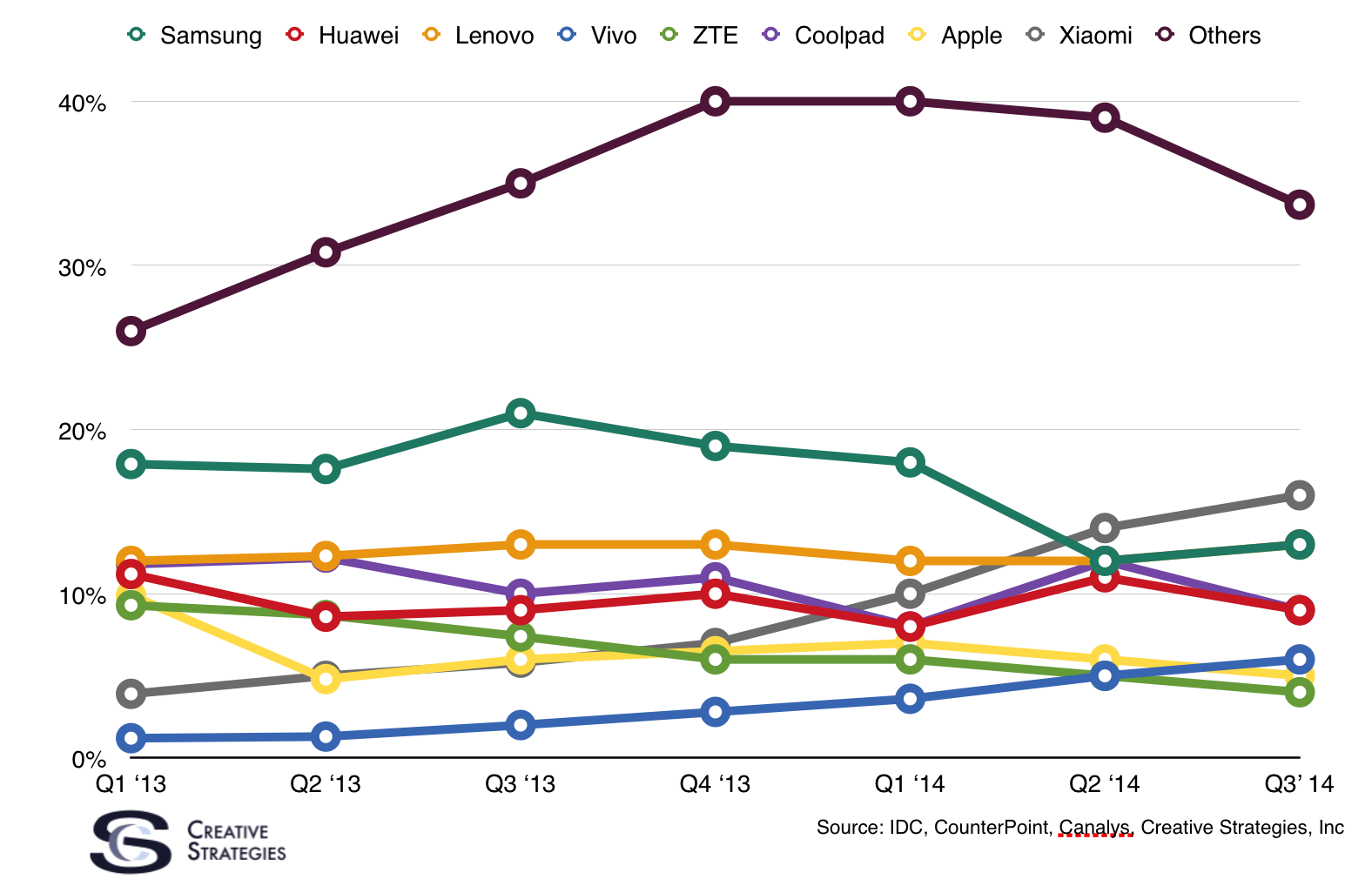

With Chinese consumers’ loyalty to WeChat, it means Android vendors could come and go. Xiaomi is doing a decent job building some loyalty and all on-the-ground research I get from China indicates a growing pride of Chinese consumers for local Chinese tech brands. This will continue to pose challenges to Samsung. We are watching a number of Chinese brands closely, but Vivo (charted below) is one to keep an eye on as they are positioning a number of their products to the high end.

There are many story lines to watch and analyze throughout 2015 with regard to China and I’ll keep updating my narratives on all of them.

Mobile Is Eating The Car

I attended last week’s Los Angeles Auto Show, as I do every year. While the norm among native Californians seems to be to fly from San Francisco to Los Angeles, I always drive. I make my way over to I-5, confirm there are no patrol cars nearby, then torch the accelerator. Soon I’m in LA, checking out all the new models and the many concept cars.

This year was different.

This year it was incontrovertibly clear just how much mobile is eating the car. We still need cars, of course. Some of us still desire cars. But their value is being eaten away by our smartphones.

While it may not seem the tiny smartphone would impact the car industry, car design, or our massive, decades-long commitment to car infrastructure, the fact is smartphones are disrupting this giant 20th century ecosystem just as they are so many others.

1. Jobs To Be Done

A primary reason for the car’s existence is to get us to work. In the mobile age, work is everywhere we are.

Mobile devices enable us to work anytime, from anywhere. They are even changing the meaning of work, its urgency, how we collaborate, how we respond, and what data is available.

Plug in from the coffee shop. Have a video conference while walking the dog. Check sales reports, site data and support emails from the couch. In this new world, cars are less important, less valuable.

2. Location Location Location

We need to know where we’re going and want to know the best route. Smartphones are already better at this than cars:

- We are more familiar with smartphone mapping tools.

- They offer real time traffic data, including data from the crowd.

- They know our history, previous locations and preferences better than our (dumb) cars.

- They know our schedule and contacts better than our cars.

All of this means smartphones, not cars, can better predict where we need to be, where we should be, which path is best, and which mode is superior — car, public transit, ride service, walk or staying put. Yes, we still need the car to physically get us from Point A to Point B, but the value of the location data — more prevalent in our smartphones — is ascending.

3. Entertainment

We are human. We need to be entertained. The more (and better) our smartphones entertain us — while we are in a car — the less important the car itself. The car’s value is diminished. Don’t believe me? Try this: commute in a $20,000 Honda Civic for one month, with your smartphone. Next, commute in a $90,000 Cadillac Escalade, fully tricked out, also for a month — but without connectivity. No streaming, no Siri, little to keep your and your passengers entertained.

4. Interface

We deserve simple, instant access to our music, our contacts, our friends, our status updates. I have examined multiple cars at multiple price points and every smartphone I’ve ever used offers a superior interface to mapping, entertainment and other data — despite a 120 year head start for the car industry.

Apple’s CarPlay and Google’s AndroidAuto will deliver simpler, more responsive interfaces, better data, richer options. Expect these to become the norm, not the car maker’s lesser, more confusing dashboard configurations.

As the more personal, interactive interface of the smartphone evolves — from inside the car — the more the car itself becomes merely a vehicle for transportation. Again, this will diminish the car’s value.

5. Ownership

Uber and similar services, all thriving due to the smartphone, are further undermining the value of a car. Consider that if you live in an “exurb” and commute to the big city for work every day, and your commute totals a whopping 20 hours per week, you are still only using your expensive car for no more than 20% of the day.

That’s a wasted asset. Why pay tens of thousands for a car that will rarely be used when someone else can take you to wherever you need to be?

Yes, the convenience of owning still trumps “ride sharing.” Owning a car means it’s always right outside your door, available at a moment’s notice.

This will change. Smartphones will soon enough be able to proactively tell any available car to be waiting and ready for us, wherever we are. Knowing our calendar, preferences, history and habits, our present location, our to do list, and knowing who we are with — and who we may need to impress — will become more valuable than having the same owned, under-used car always nearby, eating up our limited wealth.

6. Freedom

Cars are freedom. Every teenager knows this.

Or, once did.

The open road may beckon some but with constant connectivity to friends and family, with our favorite musical groups via social media, with our favorite TV stars via Twitter, with our favorite books on Kindle, it’s time to accept a new truth: we now have more freedom inside our smartphone than is available anywhere our car may take us. No wonder fewer teens are interested in getting a driver’s license.

7. Under The Hood

For decades, car owners loved to get under the hood, tinker with the engine, make modifications and personalize their cars. Look at today’s engines, especially those that are hybrid or electric, and know that one of the glories of car ownership is rapidly being stripped away. Only trained experts using the right tools can safely modify your purchased vehicle.

Mostly, it’s the same with smartphones. Still, after-market accessories and efforts such as Google’s “Project Ara,” which lets users customize their own mobile device, may foster a generation of smartphone tinkerers who previously might have liberated their mechanical creativity on the internal combustion engine.

We are rapidly approaching a world where a $250 smartphone is more important than a $25,000 car. The world will never be the same.

Understanding the Global Mobile Web

In the latest mobile focused podcast with Benedict Evans and myself, we touched on a theme that needs more fleshing out. That of a future only possible because of mobile computers/smartphones. When I detail the mobile first world in articles, presentations, and reports, what I highlight is not only the impact but the necessity of mobile to move computing forward. The PC in the shape of a notebook or desktop took computers as far as those shapes would allow. There are very few new users for PCs of that design. The PC in the shape of a tablet can take computing even farther, particularly in business environments, and that form factor gets a PC into the hands of more people. The PC in the shape of the smartphone, however, brings computing to everyone. Perhaps more importantly, the smartphone can bring the internet to everyone. More revolution will come from the PC in the shape of a smartphone than from any previous computing product in history. It is because of this, we will see countless opportunities emerge and it is a future only possible because of mobile.

The smartphone opens the door to new possibilities because it is the first time the technology industry is accessible to everyone. In fact, over the next decade or so, we will watch smartphones become a commodity. Estimates are, by 2020, quality, powerful smartphones could cost $10. The mobile web is already bigger than the desktop web and, in a few years, the mobile web will dwarf the desktop web. It is a cold hard fact, the future of the Internet is mobile. This reality brings out some interesting implications.

Global Mobile Web Browsing

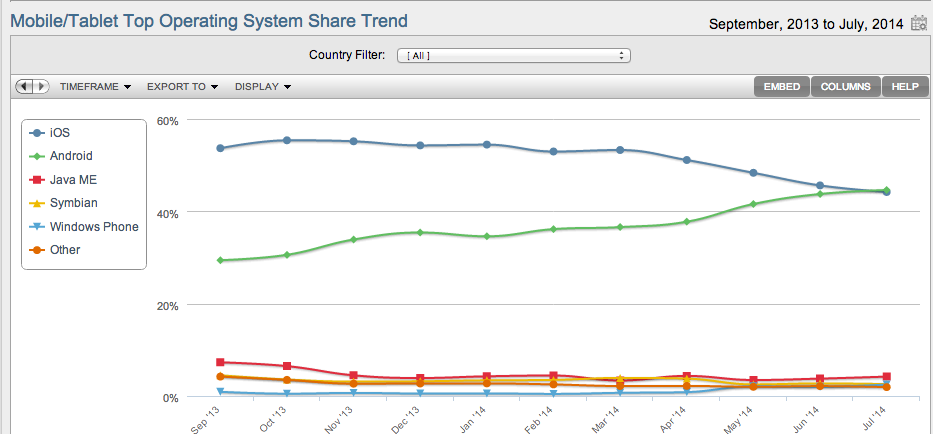

There was a debate last year around the disparity between iOS web browsing and Android web browsing. It seemed a conundrum — Android had 2x the user base but much less of the global browsing share. As you see from this chart from NetMarketShare, only recently has Android overtaken iOS in global web browsing share, and it is still very close.

When we include Android AOSP and Google’s Android, there are well more than double the active devices compared to iOS. But why did it take so long? There are many theories but there is one in particular I find insightful and adds a bit of needed clarity to the global mobile web discussion.

The bulk of Android’s growth and market share is in the lower tiers of smartphone price bands. My estimates put premium Android price tiers at roughly 15% of the global Android installed base. Meaning much of Android’s installed base globally consists of non-premium/lower price tier smartphone users. This explained quite a bit of the global web browsing paradox. Apple has a significant installed base of premium users, larger than Google’s premium users, and those customers spend more time browsing the web and consuming internet data. As I started researching the mobile web in emerging markets, it became clear one of the factors for this disparity was, because of Apple’s premium customer base, this audience could afford to liberally browse the web. Where much of Android’s installed base, having to deal with pricey and slow internet connection times, and no wi-fi at home, could not.

This insight becomes even more clear when we look at this chart from Jana.com showing the number of hours of minimum wage work required to pay for the average data plan.

Due to the infrastructure challenges in many of these markets, consumers are very aware of not only how much data they are using, but also the size of the application they are downloading. This is a fascinating quote from a post from LightSpeed Venture Partners, an investment firm focused on India.

So, what is an ideal app size, especially in markets like India with challenged infrastructure?

The ideal size is 10-15MB globally. Idea size for an app for tier 2/3 countries (like India) is below 5MB. 500MB+ is a non-starter. At 50MB+ the conversion rates fall off dramatically. On Android and iOS, conversion rates dip by 50% in tier 1 nations for non-game apps above 50MB. In tier 2 and tier 3 nations, conversion rates dip by 50% for games above 15MB.

It is becoming clear the high cost of data plans in many emerging markets are influencing how they use the mobile web and the apps they use and download.

The Light Web

Understanding this leads me to consider the role web apps may play in these markets. There is a web app called Zomato, which is sort of like Yelp for India. Zomato is a great example of a light application that is useful via a web app in those regions where light applications are necessary. It is true native apps are still dominant in these markets, however, we are still dealing with only the top 30-40% of the global mobile audience that has a smartphone and a data plan. As we extend that reach into the broader 60-70%, a healthy portion of those customers will be even more sensitive to the costs of data and size of applications they consume.

This is why the “light web” is a reality for the next billion users. Whether by lighter/more efficient native apps or, as I believe, web apps, the light web is better positioned for the next billion. Interestingly, even Uber has a robust web app. It is possible the powerful cloud and light, thin client computing paradigm is destined for emerging markets.

It is clear, thanks to PCs in the shape of a smartphone and the inevitable inclusion of robust sensors in these devices even at low prices, that we are heading to a fascinating future not only made possible because of mobile devices but empowered by them. This future will pose great challenges to many incumbents but even greater opportunities for the innovators.

The Consumer Tablet Growth Opportunity

A great deal of my tablet market analysis has been spent exploring opportunities for a PC in the form of a tablet. Opportunities not fulfilled by a PC in the form of a desktop or laptop. As I explained here, the enterprise or commercial tablet market’s upside is still quite large. But the question about the tablet opportunity for the consumer market looms.