Apu Kumar has held senior leadership roles at iconic technology brands as well as early stage start-ups, Hewlett-Packard, Phoenix Technologies, CNET.com, mySimon and is currently the SVP, Chief Deal Hacker at BlueStacks – GamePop. This is part 1 of a 2 part series from Apu on the PC industry.

Evolution

“We are the facilitators of our own creative evolution.”

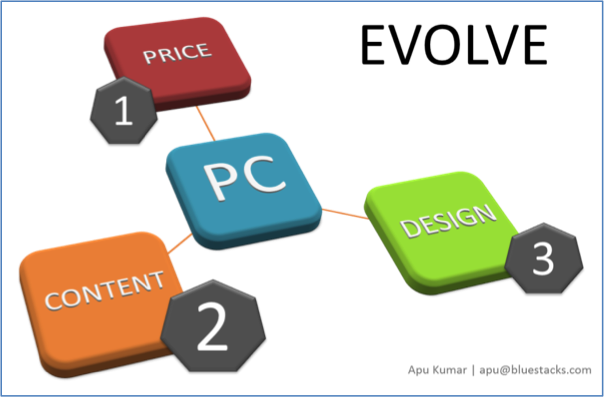

The PC needs to evolve along 3 vectors – Price, Content and Design.

Price is a very sensitive issue and affects the entire supply chain, from the chipset manufacturer, to the component suppliers and the branding companies. Price varies by market segment and by geography. The optimum pricing strategies involve many considerations that are best left for another write-up.

Content is directly proportional to the size of the installed base and the core capabilities of the platform. The PC ecosystem is acutely aware of the need for more content and apps. From the content standpoint, the PC OEMs have primarily gone down two paths to bring apps and games from Android over to the Windows PC:

(1) Android + Windows dual boot

(2) Android embedded in Windows

Dual Boot is an archaic solution with two operating systems on the same PC. End users can select the OS to boot into when they turn on the PC. To switch to the other OS, users would need to reboot the PC and wait fiddling till the device starts up again. This is a tedious process, a jarring experience and a test of patience. To make things worse, dual boot creates 3 distinct personalities on the PC, (i) the classic Windows Desktop, (ii) the Windows Modern UI, and (iii) the classic Android Home screen. The resulting experience leaves end users puzzled with questions like “Where are my apps? Will the apps installed in Android also show up on the Windows Desktop? Will I see Modern tiles for my Android apps? If I connect to the Internet on my Windows Desktop, will my Android apps also pick up my Internet settings? Can I share my files and photos between Android and Windows?” Fundamental doubts like these have led to the demise of dual boot, and rightly so.

Disruptive start-ups like BlueStacks have put on their thinking caps to embed Android in Windows by using a concoction of new and unique technologies including virtualization, binary translation and graphics acceleration. End users are blissfully oblivious to the complexity of the underlying technologies as they enjoy Android and Windows side-by-side or simultaneously on the same PC. Users can freely create app shortcuts and modern tiles in Windows 8 for Android apps. But the core system settings like Wireless, Internet, Display, Printers are only accessible and configurable through Windows. Sensors like cameras, accelerometers, gyros are detected and enabled automatically. Games and apps can run windowed or full screen. Touch screens and touch pads are supported, as are smart key mappings and keyboard shortcuts. CES 2014 validated this approach with many of the leading PC brands and x86 chipset vendors launching PC designs with Android embedded in Windows.

Good design is paramount to creating a successful product. Design-centric thinking has molded phenomenal products and great companies. Over the past years, PC design has progressed toward convertible form factors, also known as hybrid PCs or two-in-one PCs. Convertibles are an attempt to bring the goodness of mobile to the traditional laptop. By introducing touch screens and sensors, the ecosystem is hoping that consumers will see more value in the PC.

Good design is paramount to creating a successful product. Design-centric thinking has molded phenomenal products and great companies. Over the past years, PC design has progressed toward convertible form factors, also known as hybrid PCs or two-in-one PCs. Convertibles are an attempt to bring the goodness of mobile to the traditional laptop. By introducing touch screens and sensors, the ecosystem is hoping that consumers will see more value in the PC.

At CES 2014, PC brands justifiably paraded their convertibles with the glitz and glamor of an international auto show. The line-up contained a mix of impressive form factors and exotic designs. Some OEMs chose to detach the display from the keyboard of a traditional clamshell laptop PC to provide a tablet-like experience. Re-attaching the display to the keyboard enabled the classic laptop experience. Others OEMs chose to research, design and invest in fancy hinges to swivel, snap or contort the display to convert the PC turned into a tablet like magic.

Investing in design always pays rich rewards. It is refreshing to see the effort and focus on industrial design from the PC ecosystem. Convertible PCs are off to the races and the best designs will emerge victorious.

Resurrection

“If you can’t beat them right away, join them while you regroup and refocus.”

It used to be that the PC was the go-to device for all my computing needs. Now, I am tethered to my Android phone at all times as my main device for communication, social media, music and gaming. When I lean back, I put aside my phone and pick up my iPad, my preferred device for browsing, reading and watching movies. My phone and tablet also allow me to be creative and productive with a rich selection of apps for email, spreadsheets, document creation, sketching, ideation, 3D design, animation, project management and sales enablement. I can go so far as to dock my iPad to my Zagg Folio and viola, I have a functioning clamshell laptop – well almost.

Principal analyst at Creative Strategies, Tim Bajarin, is spot on in saying, “PCs continue to play a role in many people’s lives, but they are not as central as they once were. Tablets and smartphones have encroached on their place.” We are aware that the PC offers questionable value relative to mobile devices. This is in the matter of design, software, apps, services, simplicity and ease of use. Consumers are unwilling to overlook these glaring problems. Like analystß Ross Rubin wrote “it seems that anything that whiffs of the traditional PC has all the market appeal of a month-old banana”. The PC needs to wow consumers. Every PC needs a touch screen and a physical keyboard. Until such time that voice can be accurately interpreted, keystrokes will continue to be the input mechanism of choice. The classic hinge that connects the touch screen to the keyboard needs to be replaced with new connectors and hinges, both physical and wireless. The conventional “clamshell” form factor needs to transform into an origami of designs that unfold new modes of usage. Brands like Lenovo, Asus, Acer and Samsung have been creative in their industrial design with their new line of “Convertible PC” products. But that’s not enough; there needs to be a more concerted effort to innovate with a fierce sense of urgency. The PC needs to rip through its constrained design and race ahead to a new existence.

The PC can morph into a more relevant device, simple, useful and elegant. This will take a herculean effort on part of the PC manufacturers to innovate with new hybrid designs; they must be thinner and lighter and at lower price points. And then there’s software. Everyone agrees that the Windows PC needs apps by the hundreds of thousands to give it a fighting chance against Android and iOS. Microsoft will need to do its part in simplifying the new bipolar Windows OS and make it less power hungry. Startups like BlueStacks will need to work their magic to bring the full gamut of mobile apps, games and cloud services to the PC.

The PC industry needs to do all this and more and execute at lightning speed since their very existence is at stake. While they work to fix the bigger problems, it would behoove the PC industry to also find creative ways to connect and bridge the PC with the dominant mobile devices of today, namely Android smartphones and iPhones, with the goal to sync, extend and leverage the great content, apps, games and services from mobile devices and bring those to the PC. In short, what is need is total metamorphosis.

Empires rise and fall. From the ashes of fallen empires have risen new and more resilient worlds, with smarter and wiser constituents. The PC could face its destiny head on, or just lie down and be condemned to obscurity. The future of the PC hinges on this.

Real Genius assures us that we can remain fully ourself, with all our quirks, all our awkwardness, and still be welcome into its egalitarian world. The movie likewise reveals that to love what you do, love what you are good at, love working with others who feel just the same, then it’s not really work at all, its’ more a calling.

Real Genius assures us that we can remain fully ourself, with all our quirks, all our awkwardness, and still be welcome into its egalitarian world. The movie likewise reveals that to love what you do, love what you are good at, love working with others who feel just the same, then it’s not really work at all, its’ more a calling.

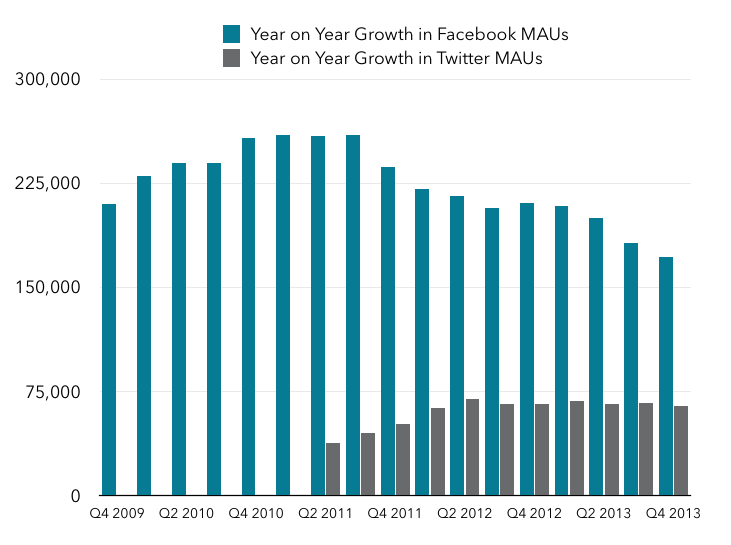

What’s clear is that both have peaked in terms of user growth. Facebook peaked way back in early 2011 at around 260 million new users year on year, whereas Twitter seems to have peaked in 2013 at around 70 million new monthly users year on year. Since user growth is the major lever for overall growth, this is notable in its own right, but it’s particularly worrying for Twitter at 232 million monthly active users than it is for Facebook at a billion more. To be clear, both are still adding subscribers at a decent clip, but the pace of growth has slowed at both, suggesting that if that growth happens in an S-curve as it typically does, both are already in the top half of the S. Twitter appears to recognize this, and on the recent earnings call CEO Dick Costolo talked about the challenge of shifting from a world where growth just “happened to” Twitter to one where the company actively has to seek growth. But recognition that something has to be done is not the same thing as knowing what to do about it. Unless Costolo and his colleagues can figure this out, Twitter’s future growth will necessarily be constrained and it’s doubtful it will ever come close to Facebook’s scale.

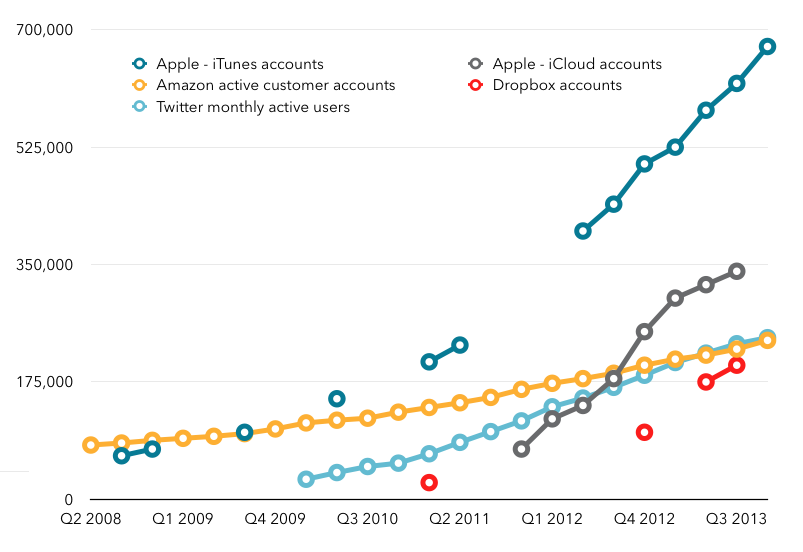

What’s clear is that both have peaked in terms of user growth. Facebook peaked way back in early 2011 at around 260 million new users year on year, whereas Twitter seems to have peaked in 2013 at around 70 million new monthly users year on year. Since user growth is the major lever for overall growth, this is notable in its own right, but it’s particularly worrying for Twitter at 232 million monthly active users than it is for Facebook at a billion more. To be clear, both are still adding subscribers at a decent clip, but the pace of growth has slowed at both, suggesting that if that growth happens in an S-curve as it typically does, both are already in the top half of the S. Twitter appears to recognize this, and on the recent earnings call CEO Dick Costolo talked about the challenge of shifting from a world where growth just “happened to” Twitter to one where the company actively has to seek growth. But recognition that something has to be done is not the same thing as knowing what to do about it. Unless Costolo and his colleagues can figure this out, Twitter’s future growth will necessarily be constrained and it’s doubtful it will ever come close to Facebook’s scale. Twitter is shown in light blue, and although it’s recently passed Amazon’s number of active user accounts, it’s far behind Apple’s iTunes and iCloud user numbers, and just barely ahead of the number of Dropbox accounts, which is also growing more rapidly. If Twitter is going to be a mass-market phenomenon globally it needs to both grow significantly more quickly and achieve significantly greater scale.

Twitter is shown in light blue, and although it’s recently passed Amazon’s number of active user accounts, it’s far behind Apple’s iTunes and iCloud user numbers, and just barely ahead of the number of Dropbox accounts, which is also growing more rapidly. If Twitter is going to be a mass-market phenomenon globally it needs to both grow significantly more quickly and achieve significantly greater scale. The good news for both companies is that these metrics are very much heading in the right direction. The exception is the most recent quarter for Twitter, where timeline views per MAU actually fell, but this was the result of tweaks to the Twitter mobile apps, which led to less going back-and-forth to and from the timeline, depressing overall numbers[ref]See Dick Costolo’s remarks on the earnings call[/ref]. So it’s a one-time downward adjustment of the curve rather than a sign of a longer-term downward trend.

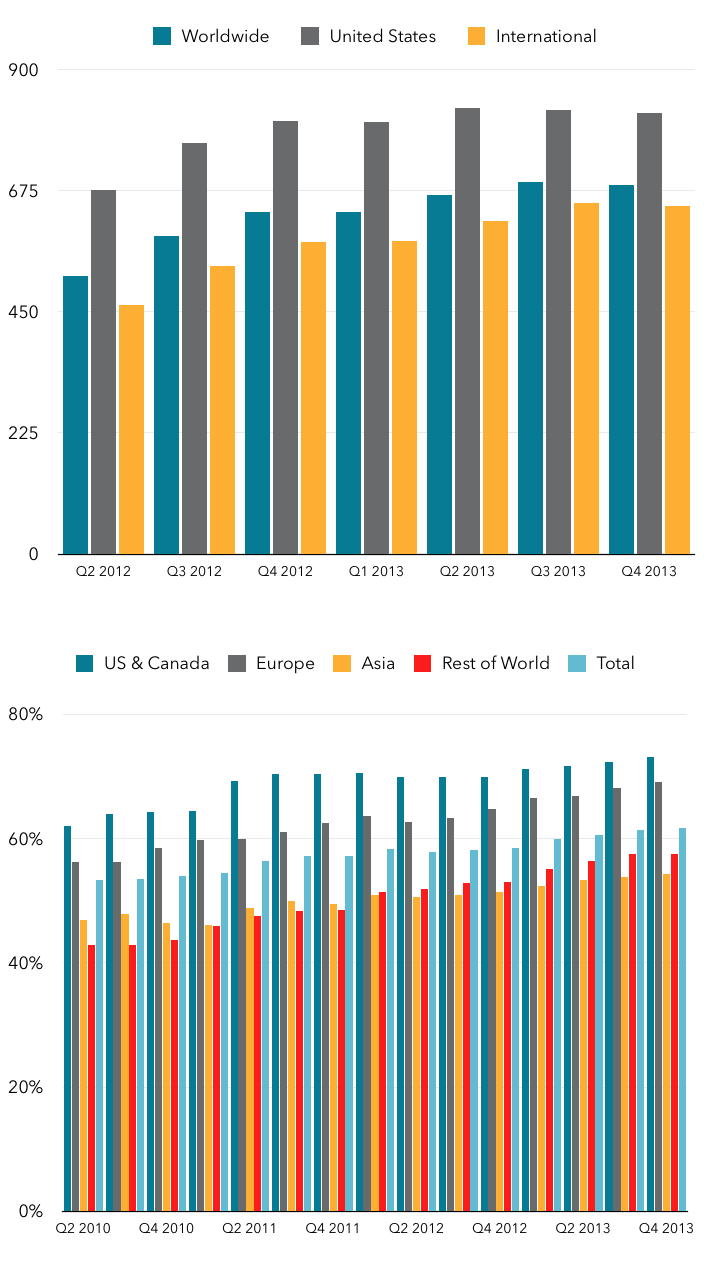

The good news for both companies is that these metrics are very much heading in the right direction. The exception is the most recent quarter for Twitter, where timeline views per MAU actually fell, but this was the result of tweaks to the Twitter mobile apps, which led to less going back-and-forth to and from the timeline, depressing overall numbers[ref]See Dick Costolo’s remarks on the earnings call[/ref]. So it’s a one-time downward adjustment of the curve rather than a sign of a longer-term downward trend. The first obvious thing is that Facebook’s ad revenue per user is much higher, which of course reflects its greater maturity and experience in providing advertising to users. But both are rising in a healthy way, which is helping to drive overall revenue growth when combined with user growth and user engagement. Interestingly, though, both companies do far better at monetizing their US users than they do international users:

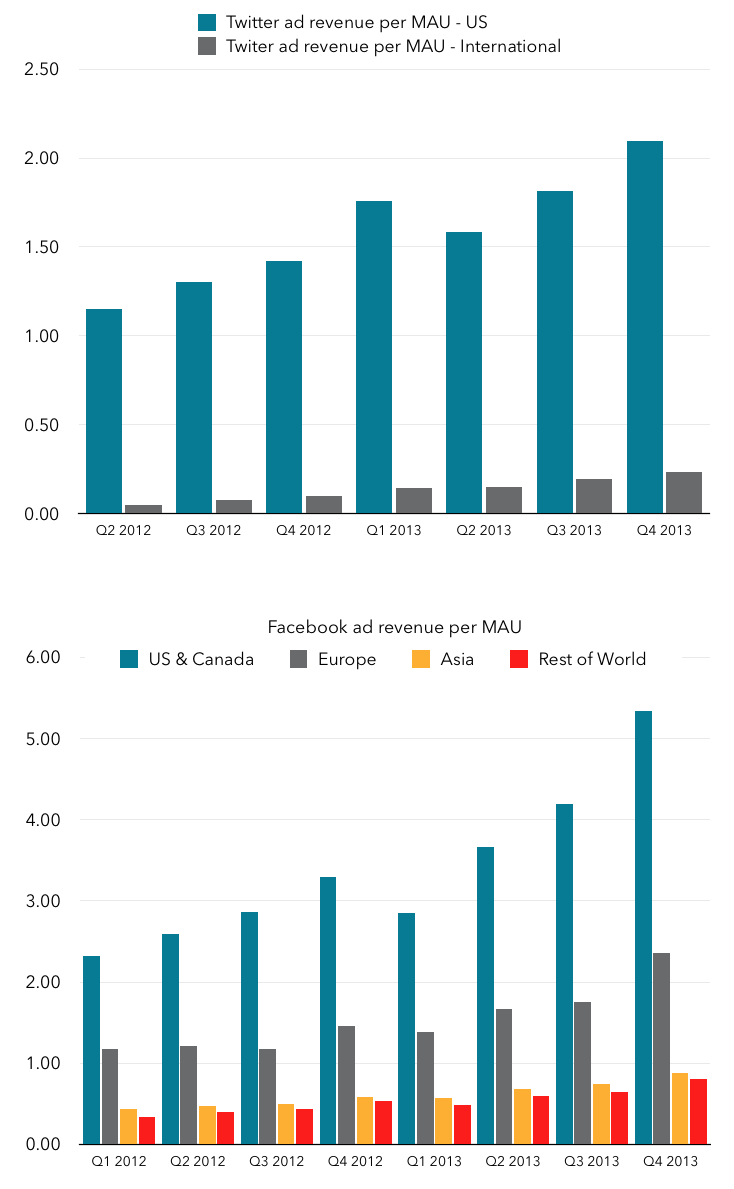

The first obvious thing is that Facebook’s ad revenue per user is much higher, which of course reflects its greater maturity and experience in providing advertising to users. But both are rising in a healthy way, which is helping to drive overall revenue growth when combined with user growth and user engagement. Interestingly, though, both companies do far better at monetizing their US users than they do international users: This is particularly dramatic for Twitter, which generated just 23 cents per MAU in the fourth quarter outside of the US, compared with over two dollars per MAU in the US. Facebook sees a greater spread between its various regions, with the US generating over $5 per quarter per MAU, Europe at $2.36 in Q4, and its other regions at under a dollar per quarter per MAU. Again, the good news though is that each company is successfully growing revenue per user.

This is particularly dramatic for Twitter, which generated just 23 cents per MAU in the fourth quarter outside of the US, compared with over two dollars per MAU in the US. Facebook sees a greater spread between its various regions, with the US generating over $5 per quarter per MAU, Europe at $2.36 in Q4, and its other regions at under a dollar per quarter per MAU. Again, the good news though is that each company is successfully growing revenue per user. Google clearly generates enormously more from its US users than Yahoo does at over $30 per quarter. Yahoo, on the other hand, generates just over $4 per quarter from its US users. Facebook has already passed that amount, and Twitter is about halfway there at this point. But neither is anywhere near catching Google yet. This obviously tells us a lot about Yahoo’s struggles too: applying the same growth strategy framework to Yahoo suggests that it’s maxed out user numbers in the US and it’s engagement and monetization where it needs to make significant progress. The big challenge here is that Google has long since hit upon the holy grail in online advertising: search. Search is unique in that it pairs advertisers with users who have expressed an explicit current interest in the item being advertised, resulting in very high hit rates. By contrast, Facebook and Twitter can only hope to derive enough about their users’ general interests to offer up profile-based targeting, which is inherently less effective (though it may help explain Facebook’s interest in graph search and other forms of search). See this

Google clearly generates enormously more from its US users than Yahoo does at over $30 per quarter. Yahoo, on the other hand, generates just over $4 per quarter from its US users. Facebook has already passed that amount, and Twitter is about halfway there at this point. But neither is anywhere near catching Google yet. This obviously tells us a lot about Yahoo’s struggles too: applying the same growth strategy framework to Yahoo suggests that it’s maxed out user numbers in the US and it’s engagement and monetization where it needs to make significant progress. The big challenge here is that Google has long since hit upon the holy grail in online advertising: search. Search is unique in that it pairs advertisers with users who have expressed an explicit current interest in the item being advertised, resulting in very high hit rates. By contrast, Facebook and Twitter can only hope to derive enough about their users’ general interests to offer up profile-based targeting, which is inherently less effective (though it may help explain Facebook’s interest in graph search and other forms of search). See this

From an article in the New Yorker, Ms. Kane opines on the present state of the post-Steve Jobs Apple:

From an article in the New Yorker, Ms. Kane opines on the present state of the post-Steve Jobs Apple: Let’s take a quick look at just two of the examples used by Ms. Kane in her essay.

Let’s take a quick look at just two of the examples used by Ms. Kane in her essay. Apple is certainly not above fair criticism. But they’re not below it either.

Apple is certainly not above fair criticism. But they’re not below it either.