Google is the new kid on the block with smartphones, but they are being treated like an established player. Their sales of the Pixel 1 and likely sales of Pixel 2/XL are likely to be very small, maybe 5m units total in 2018, but because they are Google, they are being taken seriously. While I completely agree Google should not be graded on a curve, and many media outlets are slowly waking up to this reality, I am willing to give them the benefit of the doubt for at least the next few years.

Why should we give them the benefit of the doubt? Well making hardware is hard. Microsoft made a decent product with their first Surface, but it took them until generation 3/4 of the Surface before it became a great product. The Pixel 1 was decent, and the 2/XL is better, but I know Google is playing the long game here and knowing this product will not be mainstream anytime soon, they have a little bit of time to get things right. But there are an awful lot of things they need to work out before any reasonable person would recommend a Pixel to a loved one.

I have experienced a number of these issues first hand, so I want to talk about my observations buying, and using a Pixel 2 XL since last week.

The Purchase

There are a few observations about purchasing a Pixel through Google’s online store worth pointing out. The purchase process was fine, a few too many steps for my liking but I easily picked the Pixel 2 XL and checked out. The pain didn’t begin until about the time my product was ready to ship.

I got a notice from Google that my Pixel 2 XL had been shipped and the delivery date would be November 2th; it was October 31st when I got this email. November 2nd rolled around, and nothing came, so I decided to look at the tracking number to see if the delivery date had changed. Google’s tracking software showing the package delivery time said the package should have arrived. However, upon clicking the link, I was taken to OnTrac’s website and saw that the package had still not been received to be shipped out.

My first thought was one about OnTrac. While there may be nothing inherently wrong with OnTrac, despite a few issues I’ve had before, as a consumer I felt Google was cutting corners using OnTrac instead of FedEx or UPS. Right or wrong that was thought that crossed my mind. If I’m not alone then by not using a service like UPS or FedEx Google may cause consumers to concern and worry about their package being delivered safely and on time. But the fault here was not OnTrac’s it was Google’s.

As soon as I saw OnTrac had not received the package from Google yet, I called OnTrac to understand what was happening. I quickly was patched into a customer service rep, and they explained to me that Google printed the shipping label on the 2nd and confirmed they had not yet received the package from Google to get it on a truck and out for delivery. So it was time to contact Google.

I went through the steps to contact Google customer support. It had been a while since I last had an experience with Google support, so I was a bit concerned because those didn’t go so well. As luck would have it, a customer support representative came into the online chat within two minutes.

I explained what was happening and the customer support agent started looking into it. After about 25 min I was told they would need to check with a specialist and the process will take 24 hours before I get an email with an update. 24 hours later, no email, no update. I got onto Google’s customer support chat again and was again told a specialist was needed and it would take 24 hours. Next day, no email, no update. Checked OnTrac, still nothing from Google.

I gave up and figured it would just get here when it gets here. This was not going to be my primary phone, so I was fine being patient, even if minorly irritated. The Pixel 2 XL showed up five days later. IF I had been super excited to order this phone and couldn’t wait to get it, I would have been extremely angry at the whole situation. I asked around on Twitter and found this was common with those who ordered Pixel’s, cases, and Daydream headsets, that they commonly missed the delivery window. Not a good experience for Google’s current customers wanting these products who tend to be fans and techies who love Google/Android.

And to make an observation, Apple has been shipping iPhone X orders in advance of their estimated shipping dates to the surprise and delight of their customers and Google is missing delivering windows by days and weeks in some cases.

Device in Hand

The Pixel hardware is pretty great regarding design and fits and finish. I liked how it felt in hand and, the OLED screen was great. I had no issues that others had with the OLED screen. But the camera is really what I wanted to test since so many reviewers were remarking on how it was better than the iPhone 8 Plus and iPhone X. I’ll be doing a separate post analyzing the camera between the iPhone X, Pixel 2XL, and Galaxy Note 8 shortly.

I got the Pixel 2 XL set up and went right to the camera. I took a few portrait’s using the rear-facing camera for some tests then moved right into testing the front-facing selfies. I took around 10, and the portrait feature was never applied to any of my photos. I talked to a few friends who had Pixel 2s to make sure I was doing things right, and I was. Nothing I did could get the portrait selfies to work.

After some searching on Google, I found a article on Android Authority addressing this issue and saying I needed to update the camera app but had to use the link in the article because the app isn’t actually in the Play Store. Shocking.

So I clicked the link, updated the camera app, and now portrait selfie mode was working. Google didn’t ship me a device with the most recent camera app on it, which contained the more anticipated feature most people would get most excited about. Furthermore, I had to dig into the interwebs to find a solution, which was entirely non-obvious, just to get the feature working. How many normals would do that? Not many.

Concluding Observations

These are two examples of things that just can’t happen when you ship a mainstream piece of hardware. Nor can the larger display issues and other hardware problems that have led most review sites to no longer recommend the Pixel. That being said, There are some things Google can build on.

The camera is very good. In the post where I’ll compare cameras, you will see that the iPhone rear-facing portrait photos are better than Google’s but Google front-facing selfie portraits are better than the iPhone X. What’s more interesting to me over the long-haul for Google is how they can seemingly update their camera technology via a software update thanks to machine learning. So, to make a point, an element about Google’s camera with the Pixel 2 that is interesting is how they can further upgrade it or add new features via software instead of hardware. The camera can get better through software which would allow Google to be quite nimble in adding features faster or catching up to Apple faster through hardware.

Software enhancements to the camera is an area I wish we could see Apple do more. A software or app update to the camera, like making portrait lightning mode work better, or fixing a problem I keep having with portrait selfies where it says subject too bright because of how much light is coming off the subject making portrait mode selfies not work. Little things like this, if they could be fixed via software updates, not entirely new hardware or even OS updates would allow Apple to add new features quickly to the camera. Continually updating the camera to get better without new hardware would be highly attractive to the market.

Lastly, using both the Pixel 2 XL and the iPhone X makes Apple’s custom silicon efforts stand out. If you have used Android for any length of time, you know techies have criticized its lack of smooth scrolling for years. Recent years it has gotten much better, but I was surprised using the Pixel 2 XL, running Qualcomm’s latest and greatest, how there were still jitters when you scroll. Scrolling down websites, Twitter, Facebook, Instagram, etc., all still had visually apparent jitters and was not buttery smooth (official technical term) like the iPhone.

All in all, if I were forced to use another smartphone other than iPhone, I’d pick the Google Pixel 2 XL. Mostly because I have always favored the cleanest version of Android and the only Android smartphones I liked using were Google Nexus devices using stock Android. I like the design, and the camera is really good, and will only get better. But Google has a long hard road to go down with hardware, and if they can’t fix some of the basic issues I addressed then I have no hope Pixel brand will ever go mainstream.

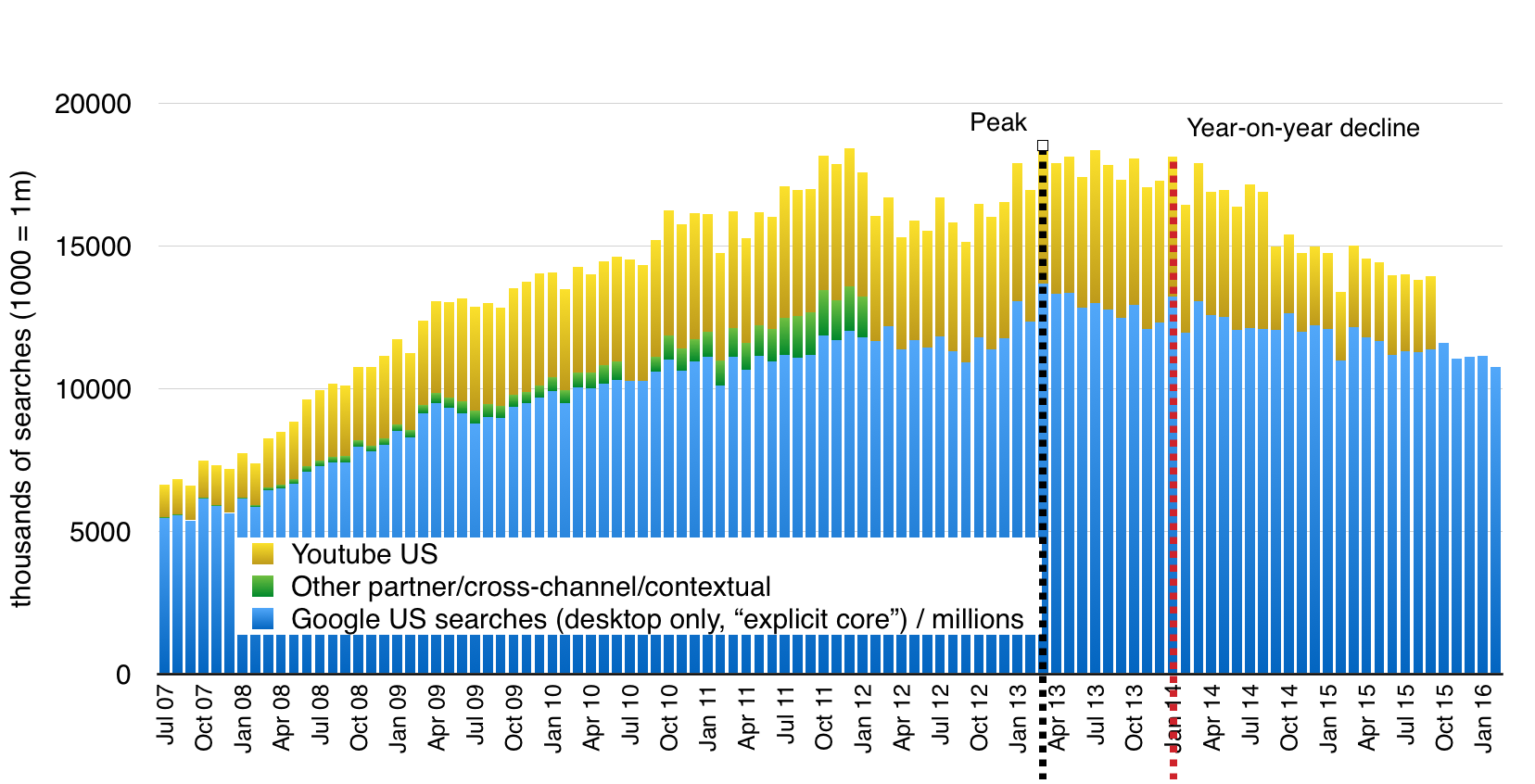

Source: ComScore. Later data for YouTube and for ‘other’ sites (eg Blogger, shown in green) not available.

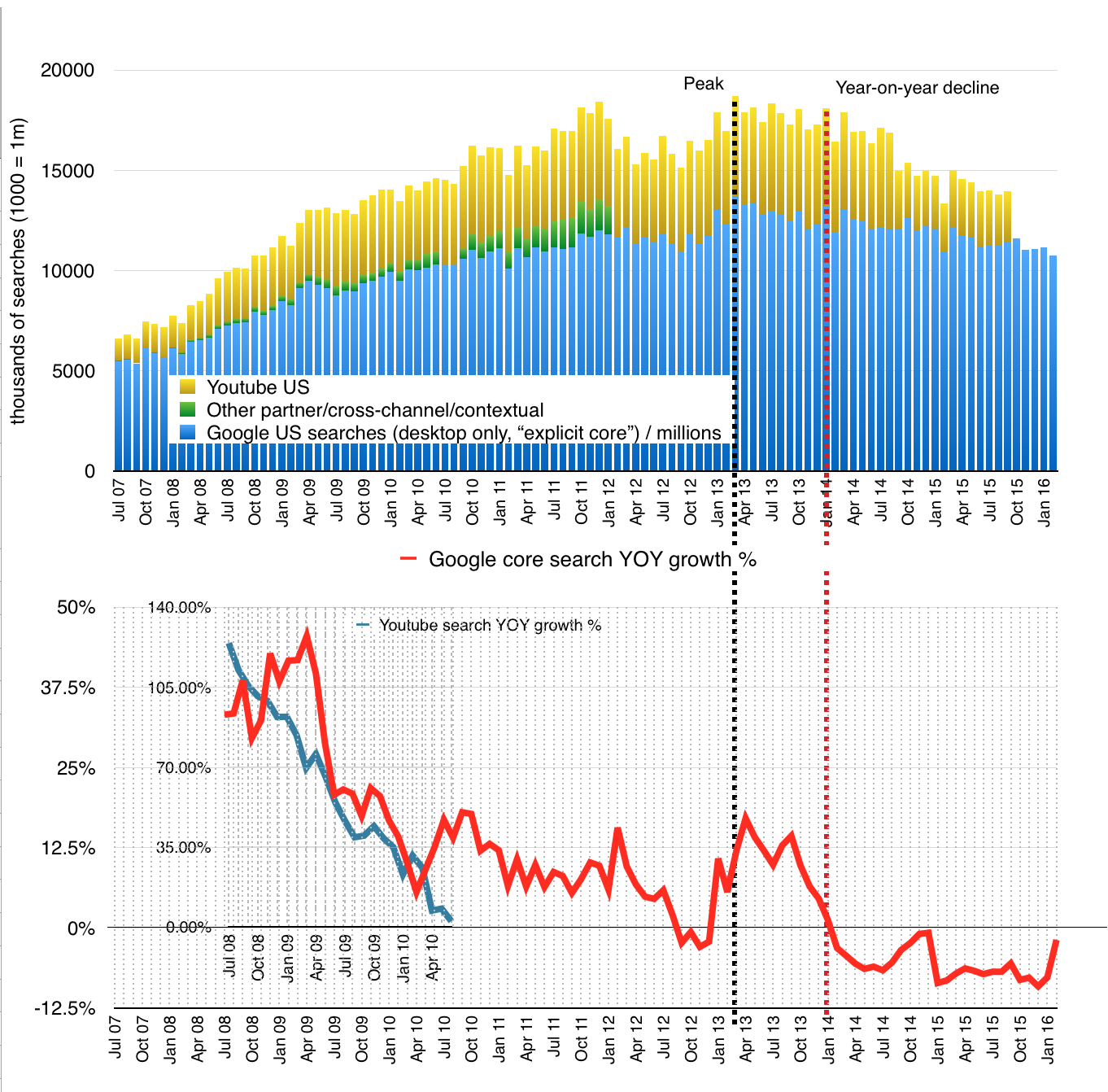

Source: ComScore. Later data for YouTube and for ‘other’ sites (eg Blogger, shown in green) not available. ComScore data says Google desktop search has been declining since January 2014

ComScore data says Google desktop search has been declining since January 2014