Facebook and Twitter are at different points in their histories: Facebook just celebrated its 10th anniversary, generates profits each quarter, and has become a dominant force in global social networking, while Twitter has a fraction of Facebook’s users, loses money and seems to suffer from a crisis of identity about its role in the world. But the two companies share a common path to growth, and it’s instructive to look at where each of them is on that path.

Fundamentally, both companies need to do three things: grow users, get their users more engaged, and then find ways to monetize that engagement. Twitter actually makes this pretty explicit, but both companies provide metrics that allow us to measure how they’re doing on each of these three strategic objectives.

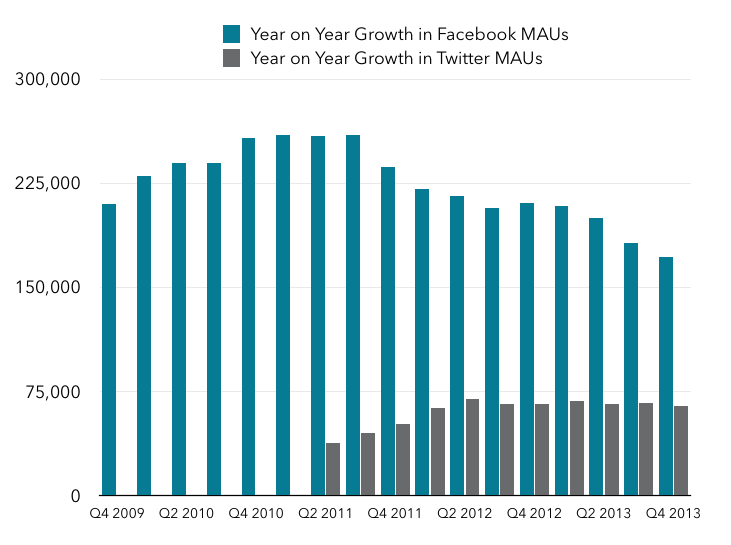

User growth has peaked at both companies

First, user growth. The chart below shows the growth in the number of monthly active users (MAUs) year on year at both companies, as reported by each of them.

What’s clear is that both have peaked in terms of user growth. Facebook peaked way back in early 2011 at around 260 million new users year on year, whereas Twitter seems to have peaked in 2013 at around 70 million new monthly users year on year. Since user growth is the major lever for overall growth, this is notable in its own right, but it’s particularly worrying for Twitter at 232 million monthly active users than it is for Facebook at a billion more. To be clear, both are still adding subscribers at a decent clip, but the pace of growth has slowed at both, suggesting that if that growth happens in an S-curve as it typically does, both are already in the top half of the S. Twitter appears to recognize this, and on the recent earnings call CEO Dick Costolo talked about the challenge of shifting from a world where growth just “happened to” Twitter to one where the company actively has to seek growth. But recognition that something has to be done is not the same thing as knowing what to do about it. Unless Costolo and his colleagues can figure this out, Twitter’s future growth will necessarily be constrained and it’s doubtful it will ever come close to Facebook’s scale.

What’s clear is that both have peaked in terms of user growth. Facebook peaked way back in early 2011 at around 260 million new users year on year, whereas Twitter seems to have peaked in 2013 at around 70 million new monthly users year on year. Since user growth is the major lever for overall growth, this is notable in its own right, but it’s particularly worrying for Twitter at 232 million monthly active users than it is for Facebook at a billion more. To be clear, both are still adding subscribers at a decent clip, but the pace of growth has slowed at both, suggesting that if that growth happens in an S-curve as it typically does, both are already in the top half of the S. Twitter appears to recognize this, and on the recent earnings call CEO Dick Costolo talked about the challenge of shifting from a world where growth just “happened to” Twitter to one where the company actively has to seek growth. But recognition that something has to be done is not the same thing as knowing what to do about it. Unless Costolo and his colleagues can figure this out, Twitter’s future growth will necessarily be constrained and it’s doubtful it will ever come close to Facebook’s scale.

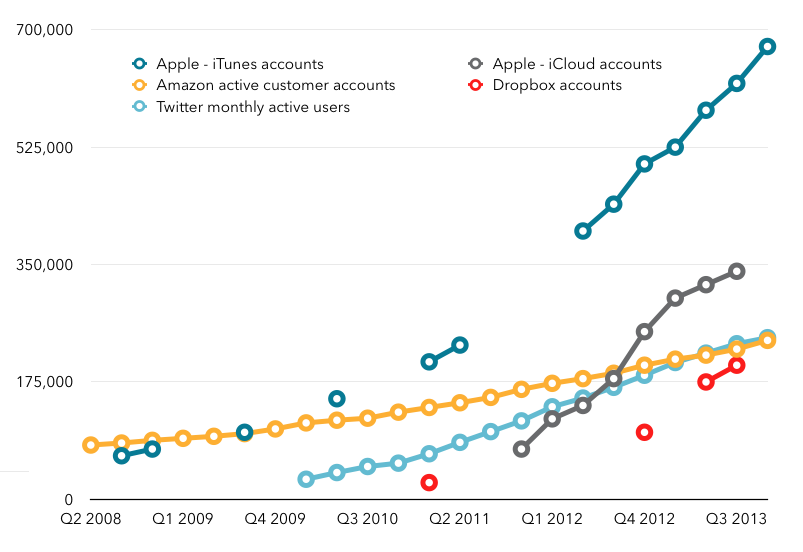

As context for Twitter’s current scale, here’s a chart that shows user numbers for various other popular services:

Twitter is shown in light blue, and although it’s recently passed Amazon’s number of active user accounts, it’s far behind Apple’s iTunes and iCloud user numbers, and just barely ahead of the number of Dropbox accounts, which is also growing more rapidly. If Twitter is going to be a mass-market phenomenon globally it needs to both grow significantly more quickly and achieve significantly greater scale.

Twitter is shown in light blue, and although it’s recently passed Amazon’s number of active user accounts, it’s far behind Apple’s iTunes and iCloud user numbers, and just barely ahead of the number of Dropbox accounts, which is also growing more rapidly. If Twitter is going to be a mass-market phenomenon globally it needs to both grow significantly more quickly and achieve significantly greater scale.

Engagement

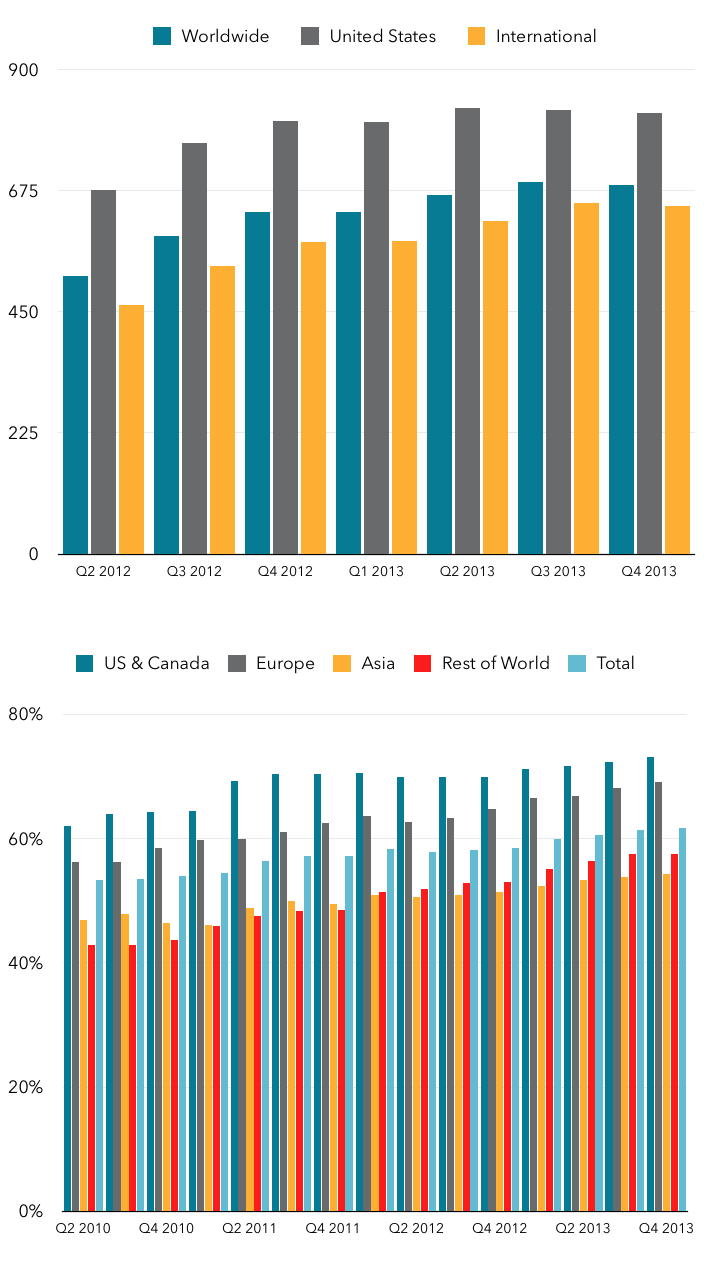

Twitter talks explicitly about engagement, and uses timeline views per MAU as its chief measure of engagement. Facebook doesn’t talk about it in quite the same way, but it does provide regular reporting on its daily active users, which are a good proxy for the proportion of users who are actively engaged. The chart below shows these engagement metrics for Twitter and Facebook. The first chart shows timeline views per MAU for Twitter, while the second shows the percentage of MAUs who are also daily active users at Facebook.

The good news for both companies is that these metrics are very much heading in the right direction. The exception is the most recent quarter for Twitter, where timeline views per MAU actually fell, but this was the result of tweaks to the Twitter mobile apps, which led to less going back-and-forth to and from the timeline, depressing overall numbers[ref]See Dick Costolo’s remarks on the earnings call[/ref]. So it’s a one-time downward adjustment of the curve rather than a sign of a longer-term downward trend.

The good news for both companies is that these metrics are very much heading in the right direction. The exception is the most recent quarter for Twitter, where timeline views per MAU actually fell, but this was the result of tweaks to the Twitter mobile apps, which led to less going back-and-forth to and from the timeline, depressing overall numbers[ref]See Dick Costolo’s remarks on the earnings call[/ref]. So it’s a one-time downward adjustment of the curve rather than a sign of a longer-term downward trend.

The other thing that’s worth noting is the variation by region. For both companies, engagement is significantly higher in the US than for their other regions. Facebook actually has a very balanced business in terms of users across the several regions it reports, with between 200 and 400 million in each of its four territories. Twitter, on the other hand, still has a very US-skewed user base, with 179 million domestic users and only 53 million overseas users, which only adds to the concerns about its slowing growth: it’s clearly struggling to achieve anything like its US penetration levels outside the US. However, both companies are successfully increasing engagement both domestically and abroad, to the extent that engagement numbers in overseas regions today are close to engagement levels from earlier periods in the US. This suggests that they are successfully matching US user behavior with overseas user behavior, just with a time delay of one to several years.

Overall, though, both companies are successfully increasing engagement, which means that there is at least one driver of growth even as user growth slows. However, Facebook’s engagement growth is slowing in the US, its dominant region, which is likely a sign that it is reaching saturation among its existing base, so it’s not all rosy.

Monetization

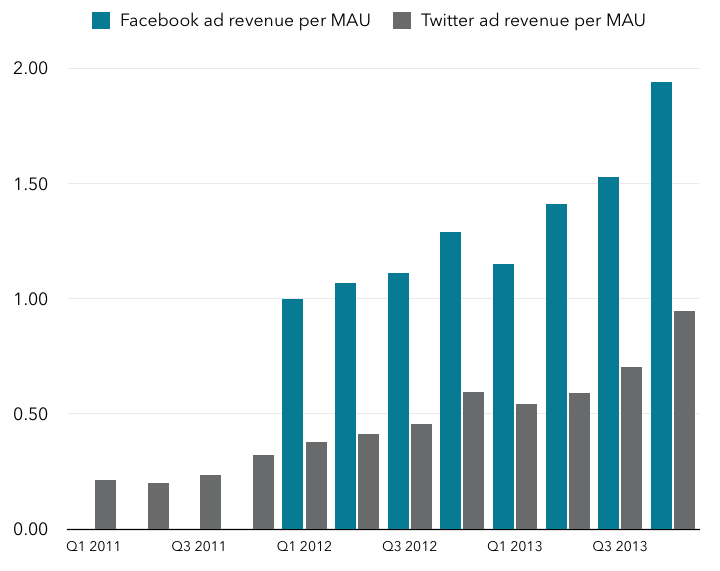

Both companies’ revenue is directly tied to advertising, which is another way of saying that they both have to find ways of monetizing the user growth and related growth in engagement in order to grow revenues. So the third lever for growth is increasing the amount of revenue per user, which is shown in the next chart:

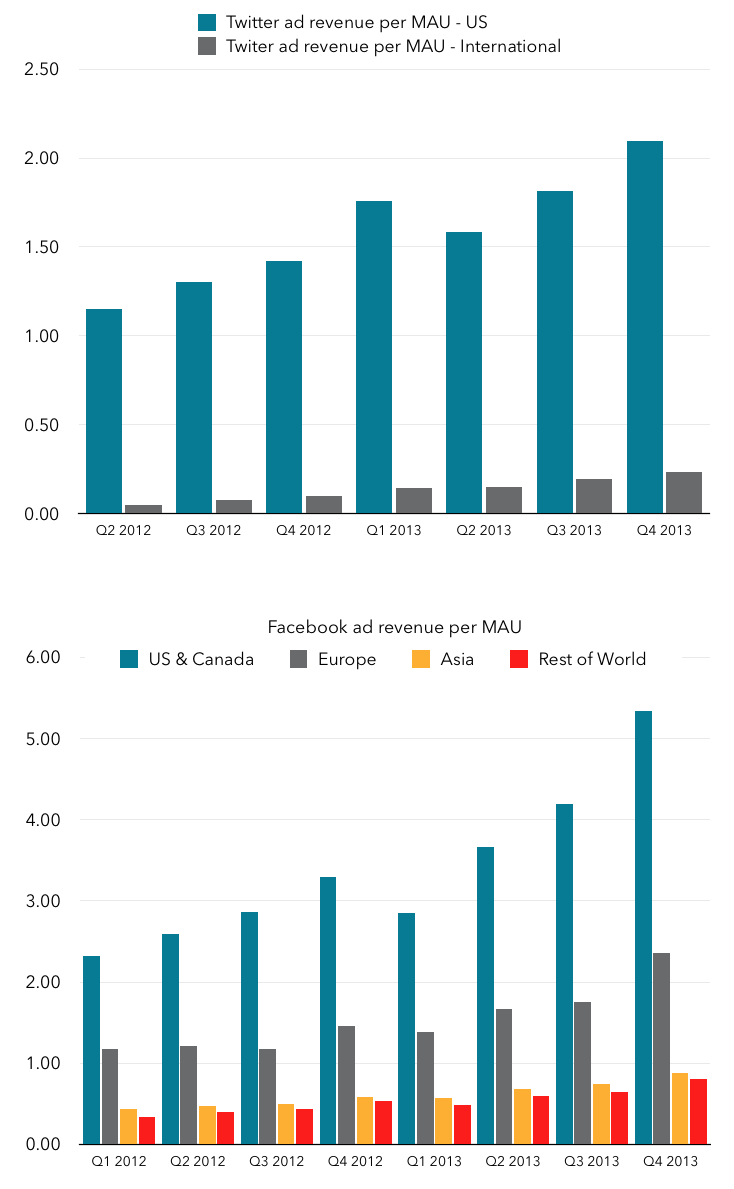

The first obvious thing is that Facebook’s ad revenue per user is much higher, which of course reflects its greater maturity and experience in providing advertising to users. But both are rising in a healthy way, which is helping to drive overall revenue growth when combined with user growth and user engagement. Interestingly, though, both companies do far better at monetizing their US users than they do international users:

The first obvious thing is that Facebook’s ad revenue per user is much higher, which of course reflects its greater maturity and experience in providing advertising to users. But both are rising in a healthy way, which is helping to drive overall revenue growth when combined with user growth and user engagement. Interestingly, though, both companies do far better at monetizing their US users than they do international users:

This is particularly dramatic for Twitter, which generated just 23 cents per MAU in the fourth quarter outside of the US, compared with over two dollars per MAU in the US. Facebook sees a greater spread between its various regions, with the US generating over $5 per quarter per MAU, Europe at $2.36 in Q4, and its other regions at under a dollar per quarter per MAU. Again, the good news though is that each company is successfully growing revenue per user.

This is particularly dramatic for Twitter, which generated just 23 cents per MAU in the fourth quarter outside of the US, compared with over two dollars per MAU in the US. Facebook sees a greater spread between its various regions, with the US generating over $5 per quarter per MAU, Europe at $2.36 in Q4, and its other regions at under a dollar per quarter per MAU. Again, the good news though is that each company is successfully growing revenue per user.

The other thing worth thinking about in this context is what’s possible longer-term. Unlike other forms of revenue generation, advertising has a natural saturation point at which it becomes off-putting to users, which puts a cap on revenues per user. The revenues per user in the US of Google and Yahoo, long-established US-based online advertising businesses, are vastly different, and show the range of what’s possible. For this exercise, I’ve used Comscore’s numbers for desktop unique users for both Yahoo and Google sites as a good proxy for their number of US users. It obviously excludes mobile users, but my guess would be that neither number would rise dramatically if mobile-only users were factored in since the total numbers are both so close to the size of the US online population. The chart below shows US revenue per US user (using that Comscore data) over the last few quarters for Google and Yahoo[ref]Yahoo hasn’t reported its US revenue numbers for Q4 2013 yet[/ref]:

Google clearly generates enormously more from its US users than Yahoo does at over $30 per quarter. Yahoo, on the other hand, generates just over $4 per quarter from its US users. Facebook has already passed that amount, and Twitter is about halfway there at this point. But neither is anywhere near catching Google yet. This obviously tells us a lot about Yahoo’s struggles too: applying the same growth strategy framework to Yahoo suggests that it’s maxed out user numbers in the US and it’s engagement and monetization where it needs to make significant progress. The big challenge here is that Google has long since hit upon the holy grail in online advertising: search. Search is unique in that it pairs advertisers with users who have expressed an explicit current interest in the item being advertised, resulting in very high hit rates. By contrast, Facebook and Twitter can only hope to derive enough about their users’ general interests to offer up profile-based targeting, which is inherently less effective (though it may help explain Facebook’s interest in graph search and other forms of search). See this separate post on advertising business models for more on this.

Google clearly generates enormously more from its US users than Yahoo does at over $30 per quarter. Yahoo, on the other hand, generates just over $4 per quarter from its US users. Facebook has already passed that amount, and Twitter is about halfway there at this point. But neither is anywhere near catching Google yet. This obviously tells us a lot about Yahoo’s struggles too: applying the same growth strategy framework to Yahoo suggests that it’s maxed out user numbers in the US and it’s engagement and monetization where it needs to make significant progress. The big challenge here is that Google has long since hit upon the holy grail in online advertising: search. Search is unique in that it pairs advertisers with users who have expressed an explicit current interest in the item being advertised, resulting in very high hit rates. By contrast, Facebook and Twitter can only hope to derive enough about their users’ general interests to offer up profile-based targeting, which is inherently less effective (though it may help explain Facebook’s interest in graph search and other forms of search). See this separate post on advertising business models for more on this.

The other thing that’s worth noting is that Google still generates a large proportion of its overall revenues from the US, even though its overall user base is obviously much larger in the rest of the world. This suggests that even mature online advertising businesses will always see much higher average revenues per user in the US than in the rest of the world, and it’s not just a question of a lag as with engagement. This is another important factor for Facebook in particular to bear in mind as its growth in the US slows to a crawl.

Conclusions

So where do we stand in evaluating Facebook and Twitter’s growth challenges? Both companies have stopped growing their user bases as fast as they once did, though Facebook has hit that point with about a billion more users than Twitter and is still adding about a quarter billion each year. Twitter’s slowing growth is worrying and should be a major priority for the management to fix. However, both companies are successfully finding ways to get their users to spend more time on their services, which combined with increased efforts to develop effective advertising products has led to significant growth in revenue per user. Both companies could continue to grow revenue significantly in the coming years even with slowing user growth simply by growing engagement and revenue per user, though at some point both companies will hit up against the natural limits imposed by advertising based business models.

delta 8 thc bad for you

Thank you for great information. I look forward to the continuation.

Thank you for great article. I look forward to the continuation.

There is some nice and utilitarian information on this site.

Great post Thank you. I look forward to the continuation.

Kudos to the author for delivering such an informative piece. Thanks for sharing your knowledge!

Hi would you mind sharing which blog platform you’re working with? I’m planning to start my own blog soon but I’m having a tough time choosing between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design and style seems different then most blogs and I’m looking for something completely unique. P.S Apologies for getting off-topic but I had to ask!

Seducing you with my awkwardness online live adult webcams. Your girl next DORK!