Three very exciting new technologies on the horizon have much of the tech world buzzing about, and billions of dollars are being invested into this new area of tech.

The first technology that hit the scene about two years ago was VR or Virtual Reality when Oculus Rift introduced their VR Glasses at CES in 2015. This product was the big hit of that CES, and shortly after, Facebook bought Oculus For $2 Billion.

Shortly after, after that Microsoft introduced their HoloLen’s project. It was entirely different from Oculus Rift’s VR version in which you are enclosed in virtual worlds; whereas Microsoft’s glasses or goggles allowed you to see through the lenses and superimpose virtual images and objects onto any scene and called it Augmented Reality or AR.

Since then another termor third technology has come into the tech lexicon called Mixed-Reality that tries to bridge the gap between VR and AR and tie the VR and AR worlds together.

Most people got a glimpse of AR, with its virtual objects displayed on a smartphone, when Niantic introduced their Pokemon Go game to the world. This game allowed people to place virtual objects on any object or scene they are viewing as part of the game and made AR a household name.

Since then Apple has created a robust AR platform through its AR kit, and hundreds of AR apps are already available on iPhones and iPads. Google has also jumped into the AR game with ARCore, their AR developer tools for Android that lets Android developers create AR apps for the Android smartphone platform. But in both of their cases, these AR apps are all delivered to a smartphone or tablet. The big question in Silicon Valley these days is whether AR will ever gain a broad audience if it is only used on a smartphone, or will select AR or mixed reality glasses be a more natural way for people to view and interact with AR and mixed reality applications in the future?

At the recent Wall Street Journal Conference, John Hanke, chief executive of Niantic Inc. discussed the success of their Pokemon Go AR app and made a crucial prediction.

“He said he thought it would take “probably in the order of five years” before the technology is mainstream. Augmented reality technology debuted on the smartphone, Mr. Hanke said, “because you build it for the platform that exists.” AR will reach “full fruition when we get to the glasses,” Mr. Hanke said. With glasses, the potential for AR “is immense because it can be woven into your daily life.”

Over my 35 years in Silicon Valley I have learned that when pioneers of a technology weigh in on a subject, they are involved with, it is best to listen to what they say. Mr. Hanke is a pioneer in AR, and since millions of people have played Pokemon Go, he has the kind of knowledge and experience to predict where AR is headed. As he states in the WSJ article, he created Pokemon Go for the platform that was already there, in this case, the smartphone. But he does not believe AR or mixed reality will reach its real potential without some AR or mixed reality glasses or goggles.

On the other hand, Apple’s Tim Cook is over the moon with AR for the iPhone. In multiple interviews, he has stated his excitement for AR and believes AR is a game changer for the iPhone and has committed to working closely with developers to create the most innovative AR apps possible using AR Kit for IOS.

Google seems to be equally excited about AR on Android smartphones although they have not been as vocal as Tim Cook has been about AR on the iPhone. The good news is that AR on a smartphone or tablet will become an essential step in getting people very familiar with the concept of AR and mixed reality and I believe it will play a prominent role in making AR glasses or goggles more acceptable once they do hit the market.

If Apple or Google had tried to push AR or mixed reality into the mainstream via glasses today, they would be a flop. Just look at the disaster Google had with their Google Glasses project a few years back, and you can see why glasses even today would be a hard sell. Getting people used to AR apps on smartphones and tablets will start the ball rolling. Once the technology is ready to create AR glasses that would work and be stylish and easily integrated into our daily lifestyles in 4 or 5 years as Mr. Hanke predicts, then glasses become the preferred way to work with and interact with AR or mixed reality apps in the future.

For their part, Apple, Google, Microsoft and many others are doing much R &D around AR, and mixed reality glasses that would be acceptable to mainstream users and all have filed multiple patents on various glasses designs already. But as Mr. Hanke of Niantic says, it could be at least another five years before the technology is here to make the kind of glasses that will bring AR to the masses in a more personal and interactive way.

I am excited about AR on smartphones but agree wholeheartedly with Mr. Hanke of Niantic that it will take some AR glasses or goggles to fulfill the promise of AR and mixed reality for the mass market. In the meantime, we should get some stunning AR apps for use on smartphones and tablets, but keep in mind that these are essential stepping stones that will eventually need AR glasses for AR and mixed reality to ever reach its full potential.

Ever since the proliferation of different individual computing devices has occurred, people have been faced with a frustrating dilemma. How do you get your devices to work better together?

Yes, it’s great that we all now have a range of impressively powerful and capable devices that let us do almost anything, anywhere. The fact that we have computers in our pockets that are now more capable than room-sized supercomputers of a few decades ago is clearly a wonderful thing. And today’s super-slim, lightweight notebooks are a godsend for those who suffered through generations of “luggables.”

Ironically, though, the more capable the individual devices become, the more frustrating are the challenges that come with not having them work together more effectively. In the past, all the serious work only happened on PCs, so that was the only logical choice for many tasks. Similarly, large capacity storage was also only available on PCs, meaning they were the only place you needed to go to look for whatever files you desired.

Now, of course, high-capacity storage exists on everything from smartphones, to tablets, to PCs, to fingernail-sized storage cards, and the unlimited capacity of cloud-based storage services means it’s getting harder and harder to find the files, images or other data that we need. Plus, the amazing compute resources and connectivity options available on everything from the smallest wearables on up means it’s possible to do complex tasks across a huge range of computing devices.

The net result is a confusing mix of devices, platforms, services, and communications options that makes it increasingly difficult to maintain an organized digital life.

Several companies have made efforts to overcome these challenges, but most are intentionally limited to their own operating systems or other environments. Apple, for example, has had the ability to receive certain types of notifications that originate on iPhones onto Mac screens since the introduction of Continuity features in Mac OS X Yosemite edition, back in 2014.

Even having simple connections between multiple devices doesn’t always help, though. In fact, sometimes it gets downright annoying. Yes, I appreciate that a phone call to my iPhone will also appear on the screen of a Mac that I may be simultaneously using, but more often than not, I’m still going to answer on the phone. Plus, I don’t really appreciate every iOS device in sight starting to ring. Now, responding to a text or instant message is certainly easier with the full-sized keyboard of the connected Mac than tapping on an iPhone screen, but the fact that I (and the majority of other iPhone owners) are usually using a Windows PC along with an iPhone means this trick doesn’t do much good.

Microsoft is also attempting to address these multi-device issues. In the new Windows 10 Creators’ Edition update, the company has introduced a feature called Continue on PC that lets you move your browsing sessions from your smartphone to your PC. The setup process is a bit lengthy and it does require you to install an app on either your iOS or Android-based phone, but it’s a step in the right direction. A number of third-party vendors are also working on similar solutions, but the seamlessness of the experience and their overall effectiveness are still unknown.

With the increasing number of smart connected devices in our homes, the longer-term vision for these multi-device scenarios needs to expand as well. Samsung presented an intriguing vision of this concept at their recent developer’s conference in San Francisco, describing the ability to move certain tasks, such as automatically transferring over your exact location in reading a Facebook timeline from a Galaxy smartphone to a Samsung Smart TV. The devil is in the details for these kinds of applications, however, and while the concept sounds great, the execution of the idea remains to be seen. Plus, there is the concern that, like Apple, Samsung will limit these multi-device scenarios to its own branded products—something that would dramatically reduce its potential impact.

The process of moving from an individual device-focused world to one where all of our devices—regardless of brand or platform—can function together seamlessly is bound to be a long one. Overcoming the challenges necessary to make these multi-platform jumps isn’t easy and brand-centric thinking doesn’t help. Plus, doing these types of turnovers effectively is going to require a lot more intelligence about how, where, and for what applications we use our various devices. Most people do things a bit differently, so automatically customizing for individual habits is going to be essential for long-term success.

Despite these challenges, however, there’s no question that we need to evolve our view and usage of multiple device scenarios into easy-to-use, easy-to-traverse everyday experiences.

This past week saw the opening of Apple’s newest flagship retail store, this one on Chicago’s Michigan Avenue. The new store is enormous and strikingly designed, and is part of the company’s new model for roughly one-fifth of its nearly 500 stores. It also reflects the shift Apple is trying to make in how people perceive its stores, from which it’s now dropped the “Store” moniker and which it would like customers to think of as “town squares” or gathering places as much as retail experiences. Today, though, I’d like to take a step back from Apple’s reinvention of its stores and look instead at the growth of its store footprint over the last few years, and what it tells us about the role of retail and Apple’s regional focus.

Approaching 500

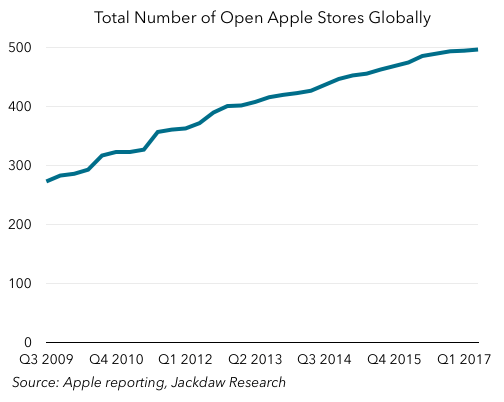

Any day now, Apple should open its 500th store, a milestone it’s been approaching for some time now. The chart below shows how that number has grown over the past eight years, from 273 stores in September 2009 to 499 at the end of September 2017:

As you can see, the growth rate has sped up and slowed at various points during that period, and in the last year in particular seems to have slowed overall, as the company focused instead on what the new experience should look like and revamped a number of existing stores.

Regional Distribution Favors the US and Europe

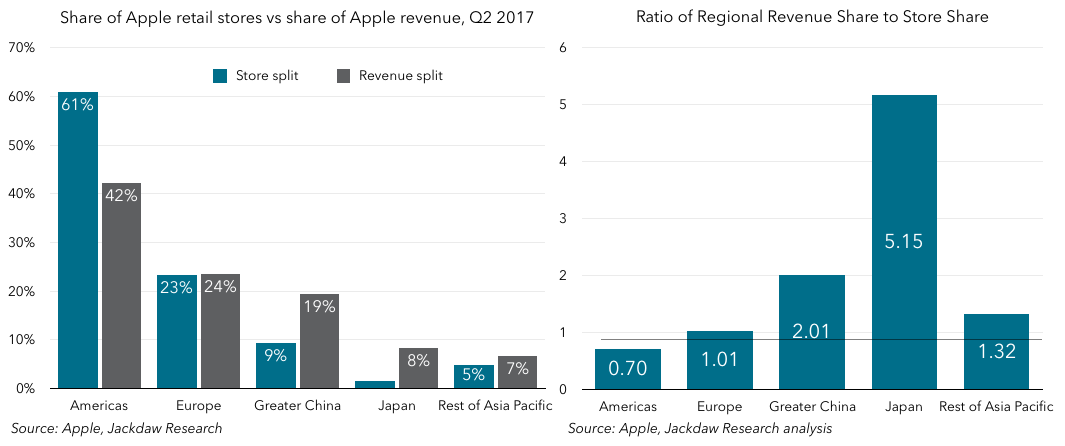

Those stores, though, are far from evenly distributed across the globe, with the US still very over-represented and other regions under-represented. The pair of charts below shows the mismatch between the contribution of each region to Apple’s revenues and the mix of stores in those markets. The first chart shows the percentage share of revenues and stores, while the second shows the ratio between the two:

As you can see, the Americas as a region has a share of retail stores which vastly outweighs its share of revenues – 61% of stores, but only 42% of revenues. At the opposite end of the scale is Japan, whose 8 stores (2% of the total) belie its 8% contribution to revenues. Europe is very close to parity between the two measures, while Greater China still has a 2x mismatch between its revenue share and its share of stores, and store presence in the rest of Asia-Pacific outside of Greater China also lags its revenue share.

Growth Over the Last Three Years Favors China, the US, and AP

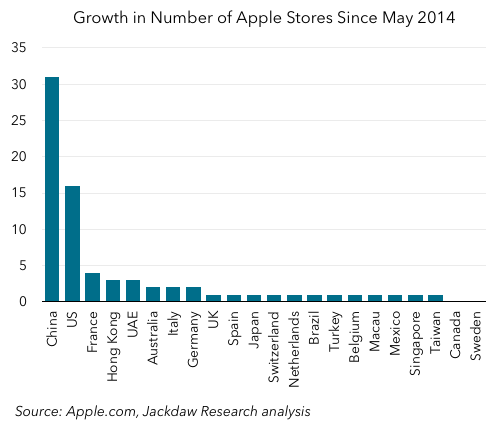

It’s interesting, then, to look at where Apple has opened new stores over the last few years, with the country breakdown shown in the chart below:

As you can see, a single country stands out starkly here: China. It has seen 31 new stores since May 2014, or over 40% of all the 75 new stores opened during that period. Together with the US, where 16 new stores were opened during that time, it accounts for 63% of total stores opened. Many countries saw either a single net new store or none at all during that period, including Canada. Of the other countries where more than one new store was opened, three are in Europe (France, Italy, and Germany) and two are in AP (Hong Kong and Australia), with one in the Middle East, also reported as part of Apple’s Europe region.

Many New Countries in the Last Few Years

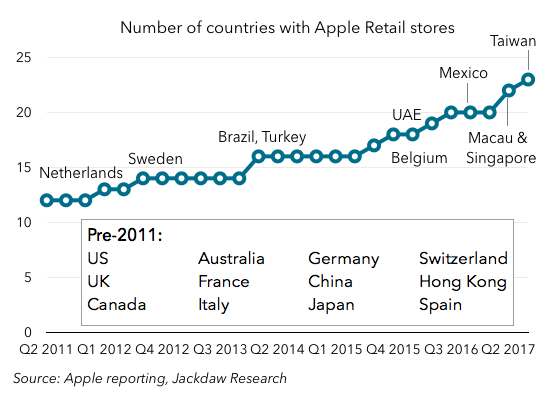

Apple currently has retail stores in 23 countries, with ten of those added since 2011. Of those, three have been in Asia Pac, and all but three have been in regions where Apple has had little penetration previously, including Latin America and the Middle East.

So the story of expansion over the last few years has three parts:

Continuing to expand in markets where Apple’s retail presence has been strong, notably the US and to a lesser extent Europe

Expanding massively in China, a region that’s suddenly become very important to Apple, and which now has more Apple Stores than any country after the US, passing the UK in the past year

Continuing to add a presence in new countries, by way of testing the water – Apple has ten countries with three or fewer stores, and five with just a single store.

Overall, that expansion has slowed a little over the past year as Apple has launched its new strategy and store concepts, but I would guess that as the company returns to growth and the strategy is implemented in a core set of stores, we’ll see it speed up that expansion and continue to focus on those three main sets of markets in much the same way.

fI want to get my two cents in on the iPhone X’s Face ID feature so I can jump up and down for the rest of eternity shouting: “I told you so, I told you so!”

UNSEEMLY ANGST

The angst being spewed over the Face ID feature is as stupid as stupid gets. Why? Not so much because it’s stupid — which it is — but because no matter how many times pundits and observers make this same mistake, they proudly make it all over again every time Apple introduces a new, revolutionary feature to one of their products.

It is not a good idea to have a strong opinion on an new tech experience that you have not experienced. ~ Benedict Evans, @BenedictEvans 10/18/2017

Rather than growing ever more humble with each repeated failure, pundits simply double-down, growing ever more strident with each iteration of the same oft-told argument.

There have been a seemingly infinite number of stupid article’s written about Face ID, but for the sake of simplicity — and my sanity — I’ll focus mostly on one article written by Ewan Spence for Forbes entitled: New iPhone X Surprises Reveal Apple’s Flawed Vision. (All quotes are from Spence unless otherwise indicated.) Now I don’t always agree with Spence, but I respect his opinion. So it’s all the more unsettling that he — like so many others — has decided to pre-judge Face ID, and for all the wrong reasons.

DESIGN

(H)as Apple placed too much focus on design and not enough on the consumer?

No.

Oh! I’m sorry. Was that a rhetorical question? Then, by all means, let’s proceed.

PREJUDGING IS GOOD FOR ME, BUT NOT FOR THEE

Until independent testing in the real world can be performed, the benefits of Face ID over Touch ID remain to be seen.

Well, that’s kinda true. But Spence’s statement would sound far more convincing if he didn’t then spend the bulk of his article telling us that he was going to prejudge Face ID as a failure right now BEFORE independent testing in the real world could be performed. Here’s an example of how that works:

Environmental factors are going to come into play with lighting, clothing, eyewear and more all impacting on the efficiency.

You don’t know that.

YOU.

DON’T.

KNOW.

THAT.

So stop saying it. Can’t you wait? Can’t you just wait until independent testing occurs before you make that kind of judgment?

Yeah, good times, good times. And today what are pundits saying about losing AirPods?

(Crickets)

BEING UNFAIR

To be fair, being unfair is what we humans do. Criticizing technology before we’ve seen or touched it — as stupid as that seems — is the norm, not the exception. The less we know about a product, the more certain we are that we can judge its value. But just because we regularly and routinely do this, that doesn’t make it right. Especially for tech writers, who really should know better.

It’s a two-step process:

STEP 1: I don’t understand (whatever).

STEP 2: I must learn more about (whatever).

Ha, ha, ha! Just kidding! No, no. No one does that! Here’s how it actually works:

STEP 1: I don’t understand (whatever).

STEP 2: I’m not stupid.

STEP 3: (Whatever) must be stupid.

Behavioral psychologists call that cognitive dissonance. Aesop called it sour grapes. I call it clickbait.

SECURITY

Spence goes completely off the rails by maintaining that Touch ID is already doing everything Face ID is promising to do, so why bother doing it? He makes this same ridiculous argument not once, but three separate times.

What problem does (Face ID) solve that wasn’t already solved by Touch ID?

Security, Dude. Security.

Does Face ID offer a better solution to Touch ID?

Yes.

While Face ID solves the problem of the recognizing a user, don’t forget this problem was already solved with Touch ID.

No, it wasn’t.

For a tech writer to say the above is simply dumbfounding. Apple stated that Face ID was 20 times more secure than Touch ID. (A ratio of 1 error in 50,000 for Touch ID versus 1 error 1,000,000 for Face ID).

That’s TWENTY TIMES more secure.

And Spence thinks more and better security isn’t solving a problem? Has Spence even met technology? Of COURSE, better security is solving a problem. Saying otherwise isn’t disingenuous — it’s demented.

INSIPID IMAGINARY PROBLEMS

Remember when people were upset because they couldn’t open their phones while wearing gloves? Now they’re upset because they can’t unlock their phones while wearing ski masks.

But that’s nothing. I’m old enough to remember when people were warning us that bad guys would be able to activate Touch ID by cutting off our thumbs! Oh no!

Now, this is just speculation but — follow me here — I’m guessing that if bad guys simultaneously had access to both our phones and our thumbs, they could just place our thumb on the home button without having to cut it off first. Or they could just politely ask us to reveal our 4 or 6 digit pin numbers by threatening to cut off our thumbs. I’m thinking either of those options might be more realistic, right?

But that was then, and this is now. We’re not going to go down that blind alley again with Face ID, are we? The heck we’re not.

IN YOUR FACE

Today’s new “They’re going to cut off your thumb” is “Your girlfriend is going to unlock your phone while you’re asleep.” (Or, more likely, when you’re passed out.) Will that work? No. You have to have your eyes open to unlock the phone using Face ID. More importantly — and I don’t mean to go all “Dear Abbey” on you — if your significant other is going to try to unlock your phone while you’re sleeping, you’re in the wrong relationship.

(Note: Spence didn’t make this argument. But others have.)

CREEPY

Facial recognition is just plain creepy, and Apple is going to have an uphill battle convincing consumers that they want to store a complex 3D map of their faces in their phones. ~ Gizmodo

Well, that’s all perfectly true if by “going to have an uphill battle convincing consumers” Gizmodo means “going to make a boatload of money selling virtually every iPhone X Apple makes”.

SELLING YOUR DATA

Here’s another argument that Spence didn’t make, but since it comes up all the time, it’s best to address it.

Apple itself could use the data to benefit other sectors of its business, sell it to third parties for surveillance purposes, or receive law enforcement requests to access it facial recognition system — eventual uses that may not be contemplated by Apple customers. ~ Al Franken

Your biometric data never leaves your device. Instead, it’s stored in an encrypted form in your phone’s Secure Enclave, where it can’t be accessed by your operating system or any of the apps running on your phone. And what’s stored in the Secure Enclave isn’t actually your fingerprint or your facial features. Touch ID and Face ID use your image and dot pattern to create a mathematical model of your face and that mathematical model can’t be reverse-engineered. The fact is, that all of this was known before Senator Franken wrote his letter and Apple said as much:

In its response letter, Apple first points the Senator to existing public info — noting it has published a Face ID security white paper and a Knowledge Base article to “explain how we protect our customers’ privacy and keep their data secure”. It adds that this “detailed information” provides answers “all of the questions you raise”. ~ Techcrunch

So all the questions were answered before they were asked. But let’s not let a little thing like facts stand in the way of speculation, grandstanding and fearmongering.

IN YOUR POCKET

Certainly the lack of Touch ID means unlocking a phone in your pocket, subtly under a table, or while being jostled in a busy commenting environment is now going to be a lot harder.

That’s it? That’s the best you’ve got? Face ID sucks because I can’t unlock my phone in my pocket?

Yeah, sure, because the last time I unlocked my phone in my pocket was…NEVER.

I could be wrong (I’m not) but most of mankind (womankind too) generally, you know, actually look at their phones when they’re using them. If your argument is that you can’t unlock your phone while it’s in your pocket, that should be a not-so-subtle clue that you’re bringing nothing to the table.

RE-EDUCATED

The user base will have to be re-educated and something that is ubiquitous in the smartphone community – fingerprint recognition – has been removed from the iPhone X.

Hmm. What a difficult problem this must be. Let’s see, let’s see. How could Apple possibly perform the difficult task of re-educating their users on how to use Face ID?

Oh, I know! They could ask them to, you know, look at their phones! Like the way they already do, like 20,000 times a day?

Wowza. Spence is seriously arguing that making people look at their phones requires re-education? C’mon, Dude. This smacks of desperation.

FUTURE POSSIBILITIES

The Touch ID sensor on the iPhone’s home button was great at what it did, but I think it had limited application elsewhere. It’s possible, for example, that it could have been used for biometrics, but I think that will be the province of the Apple Watch and maybe even the AirPods — two devices that are constantly in touch with one’s body.

The cameras and sensors in Face ID open up far more possibilities. Apple tends to introduce features that work when introduced and then those features become even more valuable when combined with features that are introduced later. This is the benefit of producing the whole widget. Apple can plan long term.

Right now, I can’t envision how Face ID will be used other than for security and AR. But that just reveals my lack of imagination and foresight. I may not be able to see exactly how the cameras and the sensors in Face ID will be used in the future, but I don’t have to be Nostradamus to see that they have the potential to do all sorts of new and interesting things. Apple isn’t just introducing a new feature that duplicates an old feature. With Face ID, they’re introducing the future.

APPLE IS DOOMED

While Apple focuses on design that benefits itself, Android’s adoption is increasing while the overpriced and over gimmicked iPhone X is going to be late and have a detrimental effect on Apple’s overall performance.

Say what now? Let’s just take a gander at some recent tech headlines.

CNBC Poll: 64% of U.S. households have at least one Apple product

There isn’t a tech company in the world that doesn’t want to be “challenged” by competitors the way Apple is.

DEJA VU ALL OVER AGAIN

You know what’s going to actually happen? The same thing that always happens. Apple is going to remove the audio jack, be criticized and then be copied. Oh wait, that’s already happened. What I mean is, Apple is going to introduce Face ID, and everyone and their brother is going to first criticize it and then scramble to emulate it. It’s as predictable as the rising and the setting of the sun.

A STUDY IN STUPIDITY

When I look at the iPhone X I see a design that works for Apple’s benefit first, with the end-user in second. I see technical solutions that translate to buzz-words that challenge logic. I see new hardware that addresses an old problem but offers fewer benefits with its newer decision. I see design choices that are in place to emphasize Apple’s branding while weakening the consumer experience.

Well, that’s the kind of stuff you’re going to see when you have your head placed firmly up your derrière.

“The highest form of ignorance is when you reject something you don’t know anything about.” ~ Wayne W. Dyer

THE FUTURE

There’s an old saying that history repeats itself, but that’s not quite accurate. Rather, the lessons of history repeat themselves until they’ve been learned. I think we’re going to see this behavior again the next time Apple introduces something new. Some lessons, it seems, are never learned.

This week’s Tech.pinions podcast features Carolina Milanesi and Bob O’Donnell discussing the recent Samsung Developer Conference and Bixby 2.0, the Alphabet investment in Lyft and its implications for the ride-hailing market, and formal release of Microsoft’s Windows 10 Creators Update, Windows Mixed Reality headsets and the Surface Book 2.

If you happen to use a podcast aggregator or want to add it to iTunes manually the feed to our podcast is: techpinions.com/feed/podcast

Windows 10 Fall Creators Update includes a number of new features, including a replacement for OneDrive Placeholders, support for Windows Mixed Reality, the ability to have a better workflow between Windows 10 PCs and iPhones and Android phones and an improved Photos app experience. For enterprise users, the added security features with Windows Defender are probably the most compelling updates. Mixed Reality support is probably the feature that will be the focus on the holiday advertising.

I have been using Windows 10 Fall Creator since it has been available to Insiders back in April and I have to say I have been enjoying most of all the UI improvements across the board. It really now feels like a much modern operating system although the things that never change make you realize that it is Windows after all – mostly the file structure and the language.

If I had to pick my top 3 features I would say improved inking, My People, and Photo Remix. Especially on Surface devices, inking is a game changer for things like document reviews. My People brings the people that matter to you to the front of your workflow in an intelligent way so that preference of communication channel is accounted for. While Photo Remix is not something I use every day, for me, it is the best example of how Windows 10 wants to move from productivity to creation.

While there are not many people using Edge on iPhone and Android to really benefit from a wider set of functionalities just the acknowledgment that there must be a focus between phone and PC is a huge deal. This is how people build their workflow today and Apple has been first in line in exploiting these changes to create a strong tie between Mac and iPhone and Mac and iPad. Yet, there are way more iPhone owners with a PC than a Mac and this should be a priority for Microsoft, especially when it comes to making Surface appealing.

I also think that Windows 10 Creator Update on Surface really shows the best of Microsoft which of course made the launch of the Surface Book 2 a perfectly timed one.

Surface Book 2

With the latest 8th Gen Intel Core processors and NVIDIA GeForce GTX 1050 and 1060 discrete graphics options, Surface Book 2 gives all the power you want or need in the design we have been accustomed to since the first Surface Book. Surface Book 2 with the 13” weighs 3.38lbs and the 15” Surface Book 2 at 4.2lbs. Surface Book 2 13” will be available for pre-order beginning November 9th in the United States and additional markets around the world, along with Surface Book 2 15” in the United States at any Microsoft Store and Microsoft.com. Delivery will begin on November 16th

This is the first true update to the Surface Book line. The original Book was updated about one year after launch but more to address some of the issues of the first generation that really deliver an update

I see the Book 2 as Microsoft delivering on the promise of serving a wide audience especially of demanding users in the top segment of the market. Giving options on form factors but also power and capabilities.

Not a device for everybody for sure, not just because of the price, but because not everybody needs that much horse-power.

The target audience I see aside from the obvious higher-end customers are users who are interested in Surface Studio but are too mobile to be able to justify their purchase. In tablet mode with the support of the Surface Dial, Surface Book 2 will deliver the same Studio experience in a more compact and mobile form factor.

With more PC vendors wanting to focus mostly in the high-end I am sure Book 2 will raise the bar on what we can see coming out from Lenovo, Dell, and HP in particular.

Samsung Creates Single IoT Platform: SmartThings Cloud

This week at its Annual Developer Conference in San Francisco, Samsung took the first step towards a company that can better connect the dots across different areas to deliver a superior experience. That step was the unification of the three pre-existing platforms SmartThings, Samsung Connect, and ARTIK under the new SmartThings Cloud platform.

While Samsung’s executives did not share many details on tools and SDKs a single “go to” platform should certainly make things easier for developers and partners.

What Samsung’s mobile lead DJ Koh outlined was a vision of consistency of experience across Samsung’s devices. Something that many have been expecting from Samsung for a while but that because of the way the company is structured had yet to happen. This is now finally changing.

SmartThings Cloud will not be limited to Samsung devices only. It is an open platform with open tools. I am sure over time we will get a better understanding of what functionalities will be limited to Samsung devices, which theoretically should have a superior experience as they can be fully controlled.

A critical part of the platform in my view is the security layer that ARTIK brings to developers and partners. This will appeal to both consumers and enterprises and could serve as a strong differentiator for Samsung. While security is rarely a selling proposition in the consumer segment, we see a much higher priority given to security when it comes to the home.

Samsung launches Bixby 2.0 and Project Ambience

Bixby was launched with the Galaxy S8 but suffered a slow rollout and high criticism for not being “smart.” Bixby 2.0 promises to be ubiquitous, personal. Bixby everywhere will be achieved in two ways. First, more Samsung devices will ship with Bixby inside – the first TV with Bixby will ship in 2018. Second, Project Ambiance will allow adding Bixby to non-Samsung devices either through a dongle or through a chip to be embedded in a product. Samsung did not disclose when either the dongle or the chip will be commercial.

The big challenge for Samsung in my view is to transition consumers’ thinking from Bixby as a user interface on one device to an interface across devices and then to a full-blown assistant.

One of Viv’s founders was on stage at the keynote talking about how all assistants today fail because they are not personal and not particularly smart. A statement that most would agree with. However, we have not had a chance thus far to actually see Viv in action and Samsung will still have to prove Bixby can deliver with the added Viv intelligence.

Ultimately, I still think Bixby’s strength will be in making our home experience less painful more frictionless. This can be a huge value add in its own right as we move from connected home to smart home. Setting the right expectations in the messaging will help consumers understand and appreciate Bixby for what it is. This seems something that even internally at Samsung has to be clarified as we heard different messages on stage.

The idea of being able to make devices that you have in the home smart by adding a dongle is quite smart in itself, especially when you talk about white goods that have a long replacement cycle. How this will work in reality beyond a speaker scenario like the one demoed on stage is unclear, however. The job of a speaker is quite easy but understanding, for instance, what adding the dongle to a fridge will help me do, is less obvious.

For other manufacturers, I think the appeal of Project Ambient will be to be the ability to add smartness at a lower cost than developing their own solution. Yet why they would add Bixby over an Alexa or Google Assistant is not clear to me. Especially given they are more likely to directly compete with Samsung than with Amazon or Google.

For now, of course, what Project Ambience shows is the power of having a semiconductor business that can deliver an end to end solution from chip to cloud platform.

In July 2014, the FCC released its Spectrum Frontiers plan, which allocated up to four large swaths of spectrum in the millimeter wave (mmWave) bands, above 20 GHz, for 5G. This spawned a bit of a land grab, with Verizon snapping up mmWave spectrum with the acquisitions of XO and Critical Path, and AT&T acquiring FiberTower’s assets. It was a windfall for these companies, sort of the tech equivalent of having held onto a house in a lousy neighborhood that suddenly gets hot. With these acquisitions, AT&T and Verizon now own close to 60% of the licensed mmWave spectrum. The FCC still retains about 1/3 of it, and plans 5G auctions at some point. Verizon and AT&T have been marching down the 5G road, testing fixed wireless access in several cities in the mmWave bands as one of the initial use cases.

But even though 5G had been heading in a mmWave, circa 2020 direction, mid-band spectrum, characterized as that below 6 GHz, is proving to be an important contender for 5G as well. T-Mobile was among the big winners in the 600 MHz auctions completed earlier this year, acquiring 31 MHz of nationwide spectrum. In August, the operator announced that it would deploy a ‘5G Ready’ network at 600 MHz, meaning that new equipment from Ericsson would be used that supports both LTE and 5G at that band. Also in August, the FCC opened an inquiry into new opportunities in the 3.7-4.2 GHz band, to be used for the “next generation of wireless services”. This effort is backed by Google and several wireless ISPs, who would want to use this spectrum for fixed wireless services. At the same time, T-Mobile and the CTIA are leading an effort to make the 3.5 GHz (CBRS) band more ‘5G friendly’ by lengthening the terms of the licenses and expanding the geographic service areas.

The upshot of this is that mid-band spectrum is emerging as a viable alternative for 5G. One can see the battle shaping up, especially if Sprint and T-Mobile merge, which is looking increasingly likely. Sprint/TMO’s main 5G play would be in their 600 MHz and 2.5 GHz spectrum, plus leveraging their holdings in other bands as well (it should be noted that TMO owns mmWave spectrum serving about 1/3 of the country, through MetroPCS). It’s not clear how active they would be in a future FCC mmWave spectrum auction.

This is setting up a pretty interesting marketing battle and debate over 5G. The mmWave bands offer a huge amount of spectrum, which would deliver orders of magnitude improvements in network speed, capacity, and latency. The tradeoff is that mmWave spectrum generally requires line-of-sight, can be affected by weather, and offers a small coverage radius. Providing service in these high spectrum bands will also require the deployment of large numbers of small cells—and we haven’t yet found the formula to be able to do this at scale, yet. There is also still quite a bit of work to be done to develop the beam-forming antennas and other technology required to deliver wireless services in the mmWave bands.

So, what does this mean for the 5G rollout? We will see services marketed as 5G, even using sub-6 GHz versions of 5G New Radio, starting in 2018. AT&T has already prepped us by launching ‘5G Evolution’ in a handful of markets. In reality, these 4.5G, or Gigabit LTE services will offer considerable improvements in download speeds and latency, which are certainly in the neighborhood of what has been envisioned for the early stages of 5G.

It’s also becoming clear that there will be different flavors of 5G. Gigabit LTE, and other services offered in the mid-bands, will look more like today’s cellular services, supporting broad coverage and mobility. Think of it as a base layer. Then, mmWave band networks will be built in denser urban areas and other targeted coverage deployments, where it makes the best economic sense and where the most subscribers can be reached. The map will look like ‘islands’ of 5G in a sea of LTE and LTE Advanced.

It will be well into the next decade before there is broad coverage of mmWave-based 5G, and there is still some question regarding the extent to which mobility can be supported in these bands or how good the coverage will be in buildings. But thinking about 5G in this way, and with this timeframe, provides a good runway for the technology to evolve. Consider that the average LTE speed is 4-5x what it was only five years ago. Apply that multiplier to 5G, as a base case, and things start getting interesting.

In the meantime, fasten your seatbelts for the upcoming marketing war between T-Mobile/Sprint and Verizon/AT&T, over 5G. With no official body really calling the shots over the definition of 5G, it will be up to the market to decide.

Samsung is holding its annual Developer Conference this week in San Francisco. At the day one keynote on Wednesday, it pushed a vision centered on “Connected Thinking” as its major theme for not only the conference but its strategy in relation to its software and services in the coming year. That was reflected in a range of moves designed to bring what have been disparate parts of Samsung together, but it’s apparent that this will be a tall order.

A Single Cloud Platform and Bixby as Connective Tissue

Samsung’s major announcements focused on three key topics:

Consolidating Samsung’s disparate Internet of Things cloud offerings

Iterating on Bixby, by improving the technology, extending it to new devices, and opening it up more

Going all-in with Google on AR through ARCore support on all of this year’s flagship phones.

The Internet of Things moves are focused mostly on using the SmartThings brand (now without Samsung as an umbrella brand) as the consumer lead, while consolidating three separate cloud IoT platforms into one, also now tagged with the SmartThings brand. ARTIK survives as a separate IoT brand, but now focused mainly on modules, while its cloud platform along with the Samsung Connect Cloud announced earlier this year will be folded into the SmartThings Cloud.

The way I see this is that the SmartThings Cloud will be the invisible connective tissue on the back end, while Bixby 2.0 eventually becomes the visible connective tissue in the front end as part of a much more coherent and connected vision for Samsung’s range of devices. Samsung executives pointed out during the keynote that it has arguably the largest number and range of devices in use of any company in the world, but the reality is that it’s always been a pretty disparate range of devices, with only fairly superficial integration between them. A big reason for that is Samsung’s operational structure, which has separate CEOs for each product-centric business unit.

The vision Samsung is pushing now is one where a variety of services on these devices will all be powered by the same cloud back-end, and Bixby will become a cloud-based voice interface which works on more and more of them over time. Bixby 2.0 will shift its personalization and training from the device to the cloud, and will therefore start to build profiles of individual users which can be exposed on a variety of devices, including shared devices like TVs and fridges. In addition to its own devices, it’s going to try to extend Bixby support to a variety of third party devices through modules and dongles as part of what it called Project Ambience, which will Bixby-enable existing home devices, both smart and dumb ones, and connect them to each other.

Significant Challenges Lie Ahead

What’s interesting here is that, even though Samsung controls the operating systems on several of its devices, because it doesn’t control by far the biggest – Android on its smartphones – it is instead building the connective layer between its various devices at the interface level. That means pushing Bixby to become far more than it’s been so far, acting not only as a way to perform tasks previously done through touch on a phone, but increasingly allowing for integration with other Samsung devices like TVs and control of smart home gear through SmartThings integrations.

In reality, though, voice can’t be the only interface and therefore can’t be the only connective layer between these various devices – in time, the integration therefore either needs to grow beyond Bixby, or Bixby itself needs to evolve to the point where it’s more than just a voice interface. In the meantime, the SmartThings brand, now decoupled from the Samsung brand to foster a sense of openness, will nonetheless become the brand for Samsung’s own connected home ecosystem too (replacing Samsung Connect), which may cause some customer confusion.

But those aren’t the only barriers to making this vision work: Samsung needs to overcome both internal and external hurdles if it’s to be successful in creating a truly connected ecosystem. The biggest internal barriers continue to be structural – hearing Samsung executives talk about this week’s announcements both on stage and one-on-one, the language is still far more that of separate companies “partnering” rather than a single team working together. The integration announced this week represents progress, but there’s a long way still go go and huge cultural barriers to overcome.

Externally, Samsung needs to convince developers and hardware partners that Bixby is ready for use as a voice platform beyond its smartphones, at a time when it’s got big shortcomings even there. Deeper integration of the Viv technology will certainly help to improve its functionality, as will opening up version two earlier to developers so that the integration can be deeper when it launches to consumers. But the leap Samsung is contemplating here is a huge one, one which other platforms have approached much more gradually and incrementally than Samsung is proposing to do. Samsung would arguably be better served by tackling either third party integration or cross-device support first and then pursuing the other second, rather than trying to do it all at once. The current approach risks over-promising and under-delivering.

The last big challenge is one of adoption – unlike earlier voice assistants, Samsung can’t simply add Bixby to existing hardware, because little of it was designed with voice interfaces in mind. What that means is that it can only grow the Bixby base to the extent that it can grow the base of devices which offer it. In categories like TVs and fridges, that means waiting until next year to even start selling them, and with long refresh cycles, it’ll take many years before penetration is meaningful. Even in smartphones, where Samsung has an installed base of hundreds of millions, it has just 10 million users of Bixby, and we don’t even know how many of those use it daily or weekly. Even if the new SmartThings and Bixby ecosystems work exactly as intended, it will be quite some time before any significant number of consumers actually get to benefit from them.

Without a doubt, in my mind, Amazon’s Alexa has been the star of the tech industry this year. Starting with CES where the banner of “works with Alexa” was first raised with support from nearly all major appliance and smart home brands. The presence of an ambient, always on, smart speaker with digital assistant has been the single greatest catalyst for the smart home I’ve seen since I’ve been studying the smart home from the beginning of the category. From a consumer perspective, the voice interface eliminated a great deal of friction from how we interact with smart home objects. Our continued research on the category keeps confirming those with Amazon Echo’s have more connected smart home products per household than those who do not and those customers rapidly increase their smart home gear after buying and integrating an Amazon Echo into their home.

As I wrote last week, the home has become the latest battleground for every company making consumer electronics, and honestly, at the moment, Amazon is the clear leader. The industry, and many consumer electronics makers seem to be ackowledging Amazon’s lead as integrating Alexa seems to be foremost on the strategy of many companies. Garmin just introduced an interesting product called the Speak which puts an Alexa assistant in your car. Sonos joins the list as well with now over 500 products having support for Alexa skills and a now more than a few dozen with Alexa directly indegrated into their products.

Amazon is doing a great job partnering here and will leverage the ecosystem of support to help them go beyond their own first party hardware to integrate Alexa everwhere. While many may not believe Amazon’s early lead here will be sustainable, I believe it will on the basis of their business model being cloud first and hardware second. Amazon’s cloud strategy means Alexa gets better overtime. So just like how your smartphone or PC/Mac gets new capabilities through software updates so do your smart products connected to Amazon’s cloud. Amazon can rapidly improve the features and intelligence of these products and simultaneously make them all work better together all through their cloud engine. This is a strong and compelling value proposition. Amazon’s early lead and industry support is going to be a challenge for Google and Apple.

For Google, the real challenge is they have lost trust and favor with many in the industry who realized very quickly they were bad partners when it came to Android. Fascinating history repeating itself from the Microsoft era as for decades computer companies only had Microsoft as a platform option, and they got fed up with them, that they desperately wanted an alternative. In walks Google with Android and hardware OEMs now had another option and they took it in mass. Now all hardware OEMS are fed up with Google and want another option for the next platform (which is voice and machine learning/AI) and in walks Amazon with a another option and the industry is taking it in mass.

This is another key reason Amazon’s lead is sustainable. The industry is clearly standardizing on their cloud for machine learning/AI smarts and Alexa as the front end interface to the machine learning/AI platform, and Google will just be relegated to search from an assistant standpoint and not managing your home or your life. While Google remains in the battle, I’m fairly convinced Amazon will win this next platform that hardware companies will use in the wave beyond smartphones. What happened to Microsoft in mobile will happen to Google in the next wave.

So what about Apple? I’ve been worried for Apple for sometime in the home because if Amazon win’s this with a vast hardware supported ecosystem and more consumers come to depend on Alexa as their assitant then Siri could be in trouble. My biggest worry for Apple is that Siri does not get the reach that will be necessary in this next wave which will have a heavy element of machine learning, which leads to AI, and voice assistants as a primary interface. This is not to say the iPhone will become irrelevant, or that much of Apple’s on device machine learning and eventually AI technology won’t be useful, but that I worry Siri will not become the primary agent consumers interact with for their life/home assistant.

The battle for the home will be one where companies have to partner well and Apple has struggled at this given the vertical nature of their business. One could make a strong argument they need to allow Siri to be integrated into third party smart home hardware in order to get the reach Siri needs. You could use CarPlay as an example, but Apple’s challenge with partners is evident with many CarPlay solutions as the experience with CarPlay is inconsistent and we constantly hear from consumers how it doesn’t always work. Apple does not control all the variables like they are used to with auto manufactures and the same problems arise when trying to accomplish reach in the smart home.

I certainly am not counting Apple out the way I am Google at this point, but I do worry that the iPhone/iOS/Siri, etc., become secondary agents and not primary ones in this next wave of computing. Apple still has a lot of work to do here particualrly around cloud and first party cloud services. There is still time but they are not making the same kind of headway Amazon is at the moment. Amazon’s lead is not too great at this point but it can get there quickly. Next years CES will be very telling about how far Amazon’s lead has become and how much farther it can get in 2018.

The move my major technology companies to start designing some custom silicon components vs. buy off the shelf components from suppliers has been a long time coming. One of the biggest challenges in the competitive field of consumer electronics is when competitors all use the same components and software platforms as their competitors. Companies competing for the consumer will live and die by their ability to be different and stand out from the pack. When you use the same software platforms and components as your competition you simply swim in the sea of sameness and have a hard time standing out. This is why Apple has developed a fully mature and foundational strategy to design all of the most critical and differentiating components that give their products an edge in the market. So it comes as no surprise that Google has developed a custom SoC for the image processing part of their new Pixel 2 smartphones.

While Apple has acquired the rare capabilities to design not just their image processor but also their CPU, GPU, and a host of other critical silicon components I don’t expect Google to go so far. I also expect other smartphone OEMs to follow suit and develop any number of custom parts from a dedicated machine learning/AI chip, image sensor, FPGA, or any number of custom ASICs that suit their needs and help them create a differentiated experience. Thinking about who may jump into the waters of designing silicon I can think of Amazon and Microsoft as potentials.

This trend was foreseeable because ARM has wanted to enable it for some time. Many of these companies designing silicon are not truly doing anything incredibly exclusive but they are tweaking generic ARM IP and customizing it for their needs. ARM will let anyone acquire a standard license and use their IP like Lego blocks to start putting together a unique solution for their needs. This is exactly what most companies are doing and what will enable many more to do so as well. But this shift underlines an important shift in how we think about what underlying components make consumer hardware stand out and become differentiated.

From Chips to Solutions

Back around 2012, I had written client notes to all the major hardware brands where I outlined the need for a component strategy to move from a few key chip decisions to a broader chip solution as a whole. The industry at the time was using the term heterogeneous computing which, simply put, meant building a computing solution that required some pieces of silicon, not just one system-on-a-chip that held all the most important parts. The idea behind heterogeneous computing was the unbundling of the SoC and moving certain functions of the SoC to dedicated chips. As Moore’s Law enabled silicon to get smaller and smaller yet remain powerful, chip companies like Intel and Qualcomm found themselves having to make trade-offs to what they designed onto the SoC and what was to be left off. This opened the opportunity for heterogeneous solutions that we see now commonplace. The big difference between now and a few years ago, is companies are now looking to design the co-processors or other compute engines no longer on the SoC themselves to deliver a specific experience they have in mind.

This move means that the value is not so much in the SoC any longer but in the total sum of all the components working together to deliver a specific differentiated experience. So Google can put together a device that has the core SoC which has the CPU, GPU, modem, IO, etc., and then design or buy the co-processors they want to deliver something unique. It is in the decisions that go beyond the SoC which is now the things that will differentiate competitors.

There was a time during my career as an analyst where I focused solely on the architecture of a single chip design when I did my analysis of a design. Over the last few years, the focus has shifted from the chip itself to the entire solution (all the chips and sensors) used in a computer. Moving from the single chip design to the design of how all the chips work together in a heterogeneous computing environment is where the exciting, and challenging, work is being done for hardware manufacturers.

One could argue that this trend will require even better software engineering than at any point in computer history. While many companies will try to make specific components, the true payoff for innovation will come from those who best can make all the pieces work best together as a complete whole. Only a few tech companies do this well, and others are trying to learn. Those who do it well will fend off types of disruption easier than those who don’t.

Many years ago, it would have been impossible to predict that the future of consumer hardware brands depends on their ability to design silicon, but that is now the undeniable reality.

Last week, actress Rose McGowan’s Twitter account was suspended for 12 hours after she wrote a series of tweets accusing Hollywood’s producer Harvey Weinstein of raping her. When she said she was being silenced, Twitter responded that her account was suspended as one of her tweets included a private phone number, which violates the code of conduct. This explanation did not convince many, however. At a minimum, it raised questions about the timing of it all. CEO Jack Dorsey took to Twitter to admit that his platform “needs to do a better job at showing that we are not selectively applying the rules.”

It is not the first time that Twitter is under fire not so much for lack of clarity on what makes up a violation of the code of conduct but for lack of consistency on how those violations are dealt with when reported. Over the past year, as harassment increased, Twitter deployed a series of measures, like the ability to mute a conversation or a user, that seemed to be aimed at hiding the issue rather than addressing it. Just because I no longer see the abuse and harassment, it does not mean it has gone away. More importantly, those users who are harassing and abusing others feel that their behavior is condoned.

Fresh off the press there is a Twitter internal email obtained by Wired that outlines new rules Dorsey is readying to release but I will wait for an official communication before commenting.

Social Media Engagement

Social Media drivers differ from people to people and from network to network. I was a reluctant Twitter user. I started using the platform for work in 2009 but did not do so consistently until 2013 when I changed job. Twitter quickly became a useful tool to keep on top of the news. My initial passive networking experience turned into an engaged one as I came to appreciate being able to share my thoughts on the tech world and actively engage with fellow tech watchers. As my engagement grew, I set some rules for how I wanted to use the platform:

– Never say anything I could not stand behind in case it was published as a quote in the press

– Keep it clean-ish

– No Religion

– No Politics

Pretty simple stuff, right? Eight years on, I am proud to say that except for the last rule I have been quite diligent in following them. I am sure that, given the current state of affairs in all the countries I lived in over the years, being silent rather than breaking my own politics rule would have been the real crime!

In a recent report published by GWI, I discovered that I was not alone in my reliance on Twitter for news. Twitter users are first engaged in reading news stories (57%) followed by liking a tweet (40%) and watching a video (34%) Direct actions such as tweeting a photo or a comment about my daily life only make up 23% and 22% of activities, respectively.

Overall engagement on Twitter has been declining since 2013 (-5%), a problem that the company has been trying to address without much success. That said, engagement on Facebook over the same period has been declining even more rapidly (-16%) as consumers seem to lean more towards more videos and pictures focused platforms such as YouTube and Instagram, up 2% and 14% respectively.

It would be too easy to blame the lower engagement to harassment alone, but I am sure nobody would argue with the fact that harassment is making Twitter less appealing as a platform. Quite a few celebrities have found Twitter too ugly, and either left like Kanye West, Lindsay Lohan, Emma Stone, and Louis C.K. or took breaks and returned, like Leslie Jones, Justin Bieber, and Sam Smith. For now, the return of investment the platform is providing me is still positive. The question is, for how long?

Disasters, Emergencies, and Hashtags See the Best of Twitter

Over the past few months, we have had our share of disasters and emergencies to deal with both in the US and internationally. It is at those difficult times that I tend to see the best of Twitter. From breaking news that allows people to keep up to date with a fast-evolving situation to people coming together to help by sharing stories or ways to donate.

But even in those good moments, trolls accounts creep into the conversation to dismiss, offend or sabotage the effort.

On the back of the Rose McGowan’s incident, two hashtags emerged bringing attention to harassment on the platform and sexual harassment across the board. On Friday the 13, a #WomenBoycottTwitter started calling on women to walk away from the social media platform for a day. Many users, including celebrities, joined in. Not everybody though agreed that silence was the best tactic to make a point in this particular situation. I for one decided not to be silent and went on Twitter to condemn abuse and do what I do every day: talk tech. I thought that at a time when many women are being brave in speaking up against abuse, remaining silent was not something I was comfortable with. Also, when it comes to Twitter it only matters who is on it not who is not. In other words, you do not notice who does not Tweet. Some also were uncomfortable with the fact that the uproar against abuse was somehow limited to white women when minorities and the LGBT community have been victims of abuse on the platform for a long time.

The original intent was clear and deserves the utmost respect, but the execution was possibly not the best. So by Sunday night, Alyssa Milano encouraged people to reply “me, too” to her tweet about being a victim of sexual harassment or assault as a way to show how pervasive the problem is. A new meme was born: #MeToo. Voices were heard from women, men, straight and gay across countries like the US, UK, Italy and even more conservative France. The conversation was not limited to Twitter; it took over Facebook as well engaging more than 4.7 million people.

Burst Your Bubble…Read Some comments

Twitter succeeded in giving a voice to so many people making it clear that sexual harassment is not just a Hollywood or Tech industry issue and impacts individuals across the world. But even in that strong testimony, the ugliness of Twitter came through. Just take a look at some of the replies posted to comments of more famous women like Italian actress Asia Argento, and you quickly have a feel for how ugly people can be when they can hide behind a Twitter handle.

Very often we live in our cocoon of lists of people we follow because we respect them, share their views or are interested in what they do or say. Without knowing it, we are sheltering ourselves from all those individuals who more likely than not do not share our views, our believes, our values. And I am not talking here about which smartphone ecosystem you prefer but big stuff like politics, religion, sexual orientation.

Sometimes that bubble bursts as we get trolled or right out attacked for our views. Others, we are lucky, and we just never see the ugly side of Twitter. That does not mean it does not exist. Like we have seen since Sunday just because you do not have a story to share under the #MeToo meme it does not mean millions of people in the world don’t have one to share.

At the end of the interview, I asked Naitoh-San what technology he has his eye on that he sees on the horizon that could impact future designs of the ThinkPad? He said that he believed that someday the technology would be available that would allow them to create a foldable laptop that perhaps could even fit in your pocket.

When he made this comment, I have to admit that my first reaction to this idea is that if this technology could ever become available, it would probably be at least another ten years into the future.

However, the idea of a foldable laptop or even a foldable smartphone intrigued me, and so I got on the phone last week with key suppliers I know in Asia and asked them about this idea and what their thoughts were on this concept. To my surprise, they told me that they are working on foldable OLED screens now and that they could have them ready for the market as early as early 2019.

This idea is not new and has been pretty much a vision for mobile manufacturers for some time. Indeed, Samsung has hinted that they could have a foldable smartphone on the market by late 2018. But when I heard these comments or rumors on this concept of foldable products I pretty much saw this as something much farther out in the future and not actually on the horizon.

It appears from talking to a couple of suppliers that indeed both smartphone and laptop computer makers are now seriously focused on finding ways to design new types of products that could take advantage of a foldable OLED screen. They even have a term of endearment to describe this kind of screen and call it FOLED.

Most smartphone and laptop vendors are feverishly trying to come up with multiple product ideas or concepts that could take advantage of this new component. Now I admit that I am still a bit skeptical that they can create a foldable OLED screen in this rumored time frame, but I no longer think that this is a pipe dream or that it is ten years out in the future.

At the laptop level I think Naitoh-San’s idea that a laptop could be designed to fit in your pocket could be highly futuristic, but I could imagine a laptop that today has a 13 inch screen being folded in half, which would make it much smaller to cart around and even be lighter and thinner in the not too distant future. And the idea of a foldable smartphone with as much as a 7” screen being folded and still fitting in a pocket now seems more feasible shortly.

What is most intriguing to me about the idea of a FOLED screen is that it gives laptop vendors and smartphone makers a utterly new component that they can let their imaginations run wild with and start a new round of innovation around mobile computing designs.

While a 7-8inch smartphone in its current format sounds ridiculous today, if it can be folded in half and fit comfortably in a pocket or purse and then unfolded so that it could turn into more of a tablet, it could move the smartphone into the realm of a serious productivity tool.

And if new laptops with FOLED screens could become smaller to carry around and made, even more, portable, especially in a 2-in-1 detachable format, it could change the way people work with their laptops in the future so that they become more versatile yet still deliver the kind of power needed for high-level productivity tasks.

Now I admit that while I do study design concepts for mobile as part of my research, I am pretty lousy at actually forecasting innovative designs. But I can imagine that if you give Jony Ive at Apple or the design gurus at most smartphone and PC makers a new palette of components to work with such as a folding OLED screen, they could turn out some pretty amazing new mobile products shortly.

Given the possible evolution, FOLED screens could deliver to mobile designers; I suspect that the current notion that tech companies are no longer innovating may fall by the wayside fast. And knowing that this type of component is just around the corner makes me even more excited about our mobile future and how these new products could impact our more mobile lifestyle.

It’s a story that would have been hard to believe a few years back.

And yet, there it was. eBook sales in the US declined 17% last year, and printed book sales were up 4.5%. What happened to the previous forecasts for electronic publishing and the inevitable decline of print? Wasn’t that widely accepted as a foregone conclusion when Amazon’s first Kindle was released about 10 years back?

Of course, there are plenty of other similar examples. Remember when iPad sales were accelerating like a rocket, and PC sales were declining? Clearly, the death of the PC was short at hand.

And yet, as the world stands five years later, iPad sales have been in continuous decline for years, and PC sales, while they did suffer some decline, have now stabilized, particularly in notebooks, which were seen as the most vulnerable category.

Then there’s the concept of virtually all computing moving to the cloud. That’s still happening, right?

Not exactly. In fact, the biggest industry buzz lately is about moving some of the cloud-based workloads out of the cloud and back down to “the edge,” where end devices and other types of computing elements live.

I could go on, but the point is clear. Many of the clearly inevitable, foregone conclusions of the past about where the tech industry should be today are either completely or mostly wrong.

Beyond the historical interest, this issue is critical to understand when we look at many of the “inevitable” trends that are currently being predicted for our future.

A world populated by nothing but completely electric, autonomous cars anyone? Sure, we’ll see an enormous impact from these vehicles, but their exact form and the timeline for their appearance are almost certainly going to be radically different than what many in the industry are touting.

The irreproachable, long-term value of social media? Don’t even get me started. Yes, the rise of social media platforms like Facebook, Twitter, SnapChat, LinkedIn and others have had a profound impact on our society, but there are already signs of cracks in that foundation, with more likely to come.

To be clear, I’m not naïvely suggesting that many of the key trends that are driving the tech industry forward today—from autonomy to AI, AR, IoT, and more—won’t come to pass. Nor am I suggesting that the influence of these trends won’t be widespread, because they surely will be.

I am saying, however, that the tech industry as a whole seems to fall prey to “guaranteed outcomes” on a surprisingly regular basis. While there’s nothing wrong with speculating on where things could head and making forceful claims for those predictions—after all, that’s essentially what I and other industry analysts do for a living—there is something fundamentally flawed with the presumption that all those speculations will come true.

When worthwhile conversations about potential scenarios that may not match the “inevitable direction” are shut down with group think (sometimes from those with a vested interest at heart)—there’s clearly a problem.

The truth is, predicting the future is extraordinarily difficult and, arguably even, impossible to really do. The people who have successfully done so in the past were likely more lucky than smart. That doesn’t mean, however, that the exercise isn’t worthwhile. It clearly is, particularly indeveloping forward-looking strategies and plans. Driving a conversation down only one path when there may be many different paths available, however, is not a useful effort, as it potentially cuts off what could be even better solutions or strategies.

Tech futurist Alan Kay famously and accurately said that “the best way to predict the future is to invent it.” We live and work in an incredibly exciting and fast-moving industry where that prediction comes true every single day. But it takes a lot of hard work and focus to innovate, and there are always choices made along the way. In fact, many times, it isn’t the “tech” part of an innovation that’s in question, but, rather, the impact it may have on the people who use it and/or society as a whole. Understanding those types of implications is significantly harder to do, and the challenge is only growing as more technology is integrated into our daily lives.

So, the next time you hear discussions about the “inevitable” paths the tech industry is headed down, remember that they’re hardly guaranteed.

We’re about to kick of earnings season for Q3 2017, and so I’m doing my usual quarterly preview. My focus here isn’t so much predicting what we’ll see as suggesting the things to look for when these companies report. As usual, I’ll tackle the main companies I track in alphabetical order.

Alphabet

Alphabet’s last set of earnings was pretty impressive, with strong performance pretty much across the board and no obvious areas of weakness. Key trends continued, with ad revenue from Google’s own sites continuing to grow much faster than ad revenue from third party sites, though growth in the latter has accelerated recently. In some ways, the most interesting revenue line to look at is the “Other” bucket within the Google segment, because that’s where a lot of Google’s new focus areas sit, including its first party hardware push and enterprise cloud services. Both have been major focus areas for Google in the past year, but Q3 should have pretty low hardware revenue given it will have been the lull before new hardware was launched earlier this month, so if there’s strong growth here, that’ll be a good sign cloud services are finally starting to grow commensurate with the investment Google is now making in this area. As I noted last week, one other thing to look out for is traffic acquisition costs in the Google sites business, and how these are tracking relative to revenue.

Amazon

Amazon demonstrated conclusively last quarter that it’s in the midst of another period of higher investment and therefore lower margins – its revenues grew strongly, but its profits were way down. Investments in AWS capacity, fulfillment infrastructure and employees, and even heavier hiring in higher-paid headquarters roles like software engineers and sales people for AWS and advertising all drove up costs and drove margins down to levels we haven’t seen in a couple of years. It’s likely we’ll see some of those same trends this quarter for the same reasons, with Amazon likely hiring significantly ahead of the holiday season. One of the biggest things to watch for this quarter is how Amazon will report the financials of the Whole Foods business – my guess it that it will simply be an additional reporting line along the lines of AWS, but we’ll have to wait and see. It has historically been more profitable than Amazon’s core business, so it should provide something of a boost to overall margins, again like AWS.

Apple

To my mind, by far the most interesting thing to look at in Apple’s earnings will again be its guidance. Its overall revenues and profits for this past quarter should be fairly predictable and in line with the outlook it provided a quarter ago, but there’s a small possibility it will be at the low end of its guidance if iPhone 8 sales in the first few days on sale were less than expected. However, the December quarter is entirely unpredictable at this point, with the iPhone X going on pre-sale right before the earnings call and on retail sale right after. Apple will certainly know what kind of supply it’s likely to have in the remainder of the quarter for that device, and that in turn will to a large extent determine how Apple’s overall December quarter goes. Weak supply could depress overall iPhone sales as many would-be buyers wait out the supply constraints, while strong supply would give Apple a massive quarter off the back of both strong sales and much higher ASPs (I wrote about all this in detail in an earlier piece). Early indications of Watch Series 3 sales and an ongoing reduction in the rate of revenue decline from China are also worth watching for.

Facebook

Coverage of Facebook in the news recently has been dominated by things that have nothing to do with its financials, at least from a direct perspective, and I’d expect its earnings call to feature a few questions about Russian influence and whether the measures Facebook is taking to mitigate that will have any longer-term impact on its ad business. But ad load saturation and its predicted effect on ad revenue growth is the thing many investors will be watching for, and I’d also expect lots of questions about Facebook’s big video push and the effect that will have on margins as the company invests heavily in content and projects lower margins due to revenue sharing. We got some hints about that on last quarter’s call but I’d expect more detail this quarter as Facebook moves this project along. It’ll also be interesting to see how many new hires it had in Q3, given that it promised faster hiring in the second half of the year.

Microsoft

Microsoft continues its transition from a product-driven to a services-driven company, but the headline on all of its earnings releases for the last two years has been all about the cloud. Microsoft’s growth rate in cloud services ticked up significantly last quarter, and one of my big questions then was whether that was a blip or a sign of a change in trajectory – my guess is the former. Meanwhile, the phone business is finally far enough in the rearview mirror that it should no longer be a drag on the business, while Surface revenue growth following recent product launches should turn positive again this quarter after some declines driven by shifting release cycles. The PC business overall, which of course is a major driver of Windows revenue, continues to be somewhat unpredictable animal from quarter to quarter, and foreign currency has been an ongoing drag on Microsoft’s results overall too.

Netflix

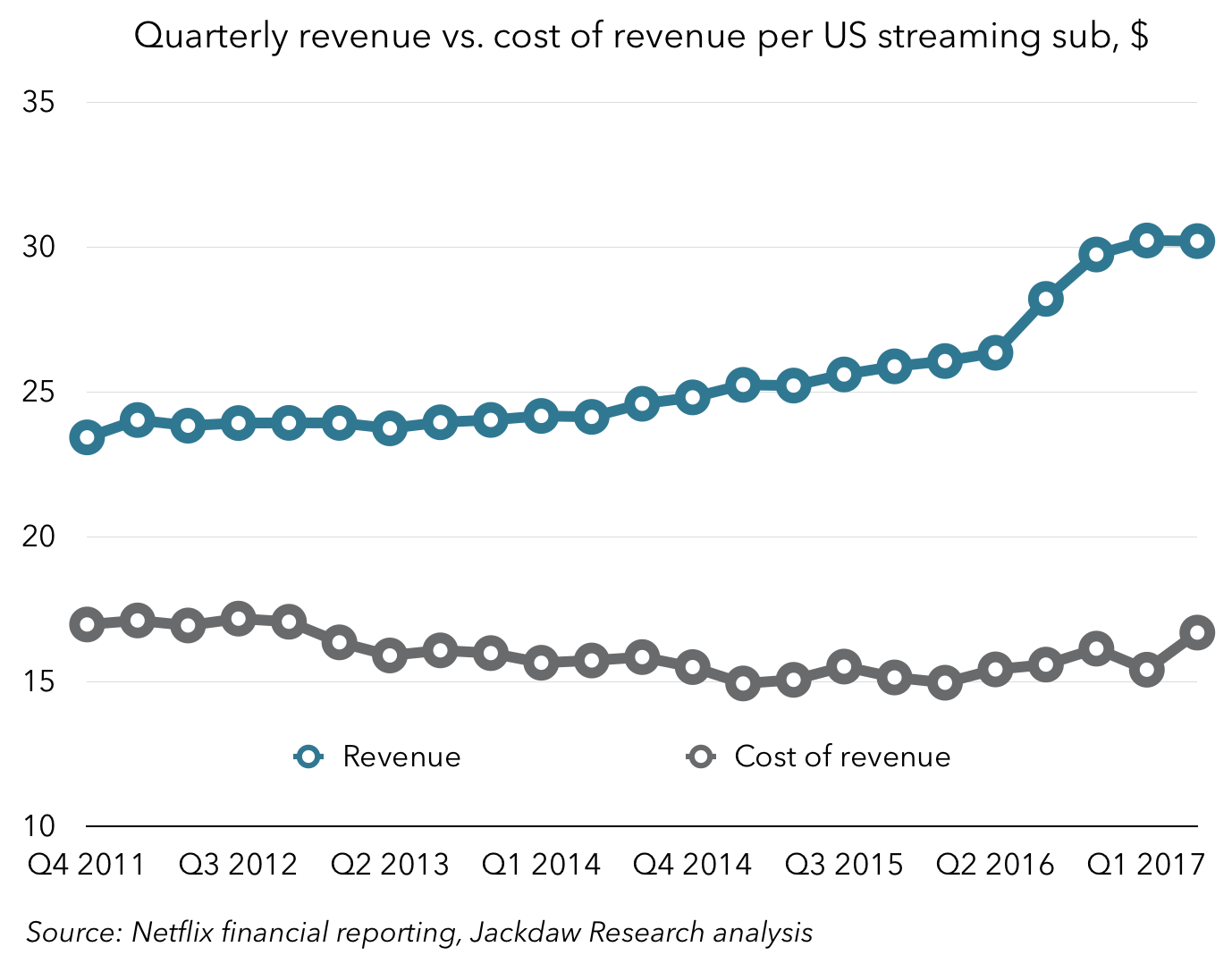

Netflix will kick off earnings season on Monday afternoon, and its guidance was for just under 4.5 million new subscribers, the vast majority overseas. Netflix’s guidance, though, has been somewhat poor lately, missing on both the high and low side, and it’s always possible that it could see significantly fewer or more net adds. My guess is that it might overshoot its guidance slightly in both geographies, but there’s no reason to expect a significant departure. The bigger question is what its guidance for Q4 looks like, given that it’s just announced price increases which will come into effect in the quarter. I wrote about those price increases here last week, and overall I’d expect them to take a hit to net adds in the US (the only region where the price increases are happening) in the quarter, but still to generate positive net adds there given that it’s usually a healthy quarter for growth. However, the impact this time around will likely come all in the fourth quarter, unlike Netflix’s last increase, so it’s possible that we’ll see a bigger and more concentrated impact this time around. I’d also expect management to be asked about the mix of customers between Netflix’s three service tiers – SD, HD, and 4K – given that the price increases affect these three bands differently.

Samsung