Fascinating things happened in 2014 with regards to the smart phone market. Two striking ones from my predictions article happened in Q4 2014 rather than in 2015 as I predicted. I hedged my bet saying they could happen in Q4 2014 and, sure enough, they did.

Smart phone vendors sold more in the December quarter than the PC industry has ever sold in an entire calendar year. Apple also passed Samsung as the number one smart phone vendor in sales in the quarter as well. Both, in my opinion, were inflection points on the entire mobile industry and have striking implications going forward. Before diving into the takeaways, I want to walk through a number of data points.

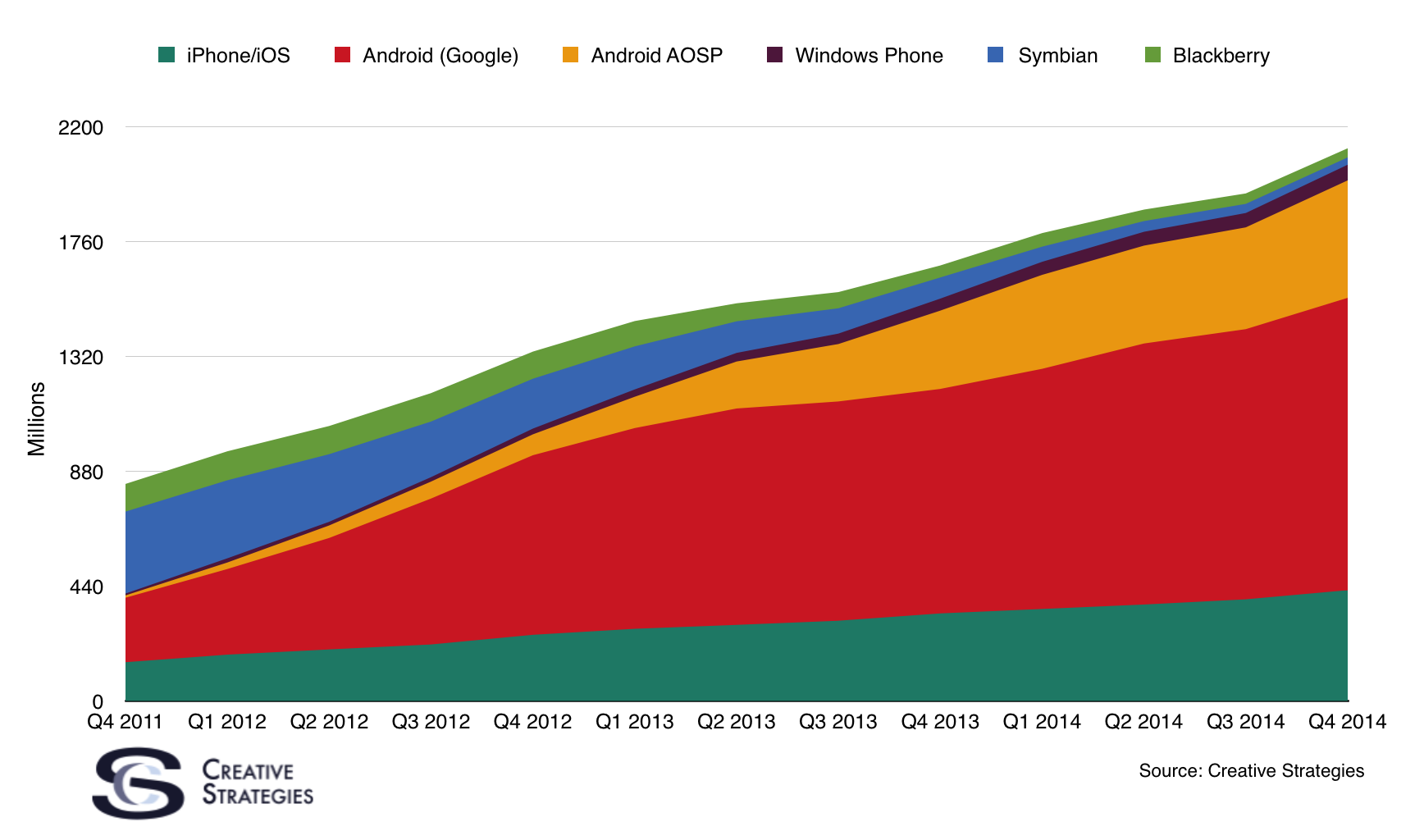

Installed Bases

On of the things I work hard to track is the installed base of smart phone platforms. Here is my chart breaking down the installed base of each current platform.

As we have been tracking this over time, you can see how Symbian essentially got eaten by Android. AOSP has been on a steady rise, thanks to China, and has an installed base slightly more than the iPhone’s. Blackberry continues to lose customers but may likely hold steady and normalize at some point.

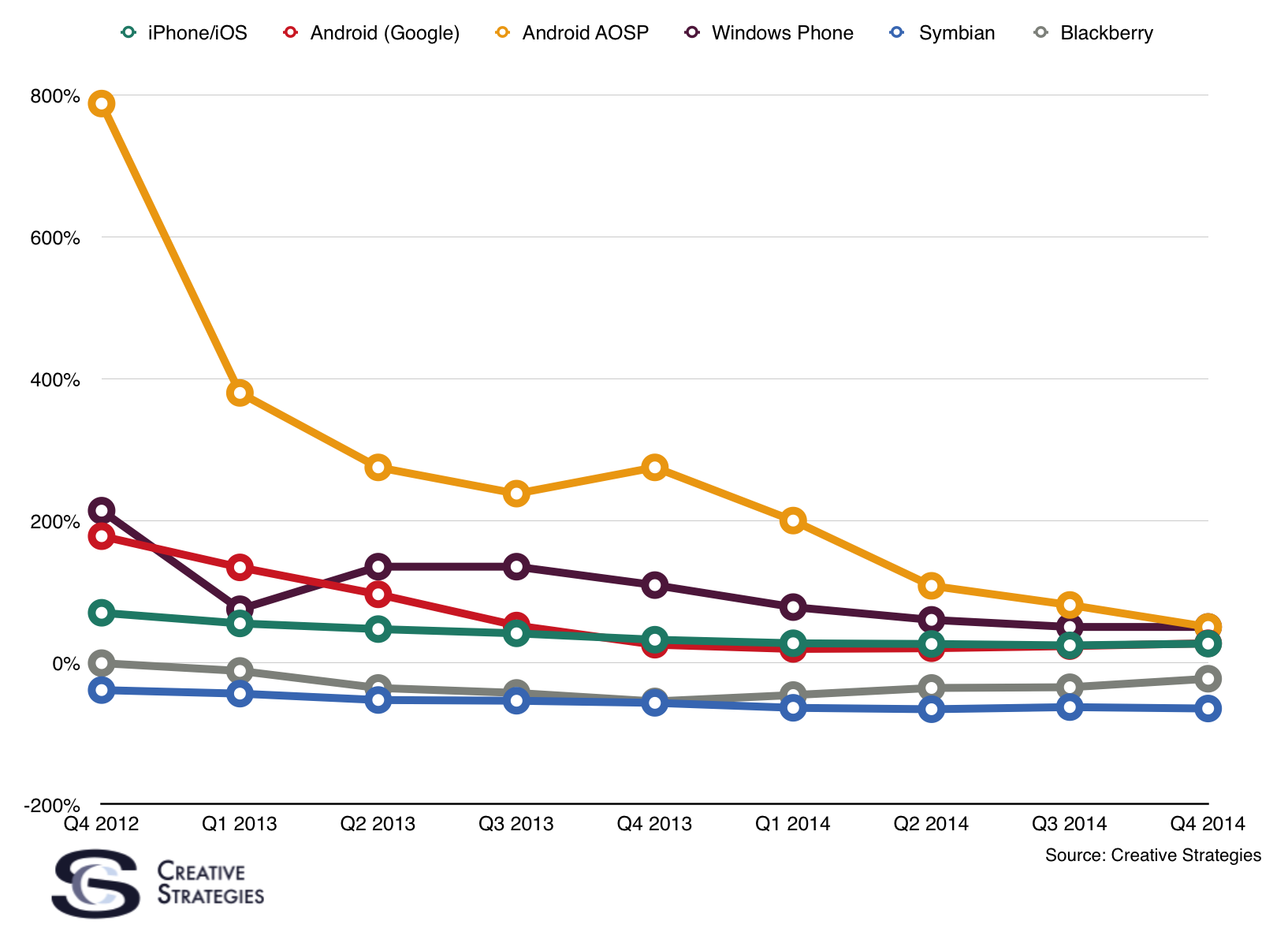

Another interesting way to look at this is to show YoY growth.

As you can see from a platform like AOSP, when you start from very small numbers and grow fast, you achieve huge YoY growth. But as your share size increases, the growth begins to normalize. I visualize this data this way to see what patterns may emerge. While Android and Apple are holding steady, we are still watching AOSP normalize. Given AOSP’s total addressable market is really only China for the time being, it is likely to hit a stopping point at some time as China becomes saturated. This growth chart will highlight that when it does. Windows Phone has modest gains annually, enough to keep their line in the positive but, in terms of size, we are talking very small numbers. I measure this YoY using a year ago quarter to track growth.

The last way I like to slice my installed base data is as a platform’s percentage of the installed base by quarter.

The point is we are seeing a normalization pattern among the major platforms. Android continues to add modestly, as does AOSP, as does Apple. What makes Apple’s installed base interesting, however, is the continued growth from hand-me-down devices and the secondary market. By my installed base estimates, about 66% of all iPhones sold to date are still in active use. This can only be achieved by making products that last long enough to get handed down to family members or sold again in the secondary markets of China and India. All of which is a contributing factor to Apple steadily growing their active user base.

Quarterly

Quarterly snapshots give us equally useful views of the market. For this we need both a global picture and a regional picture. First the global view.

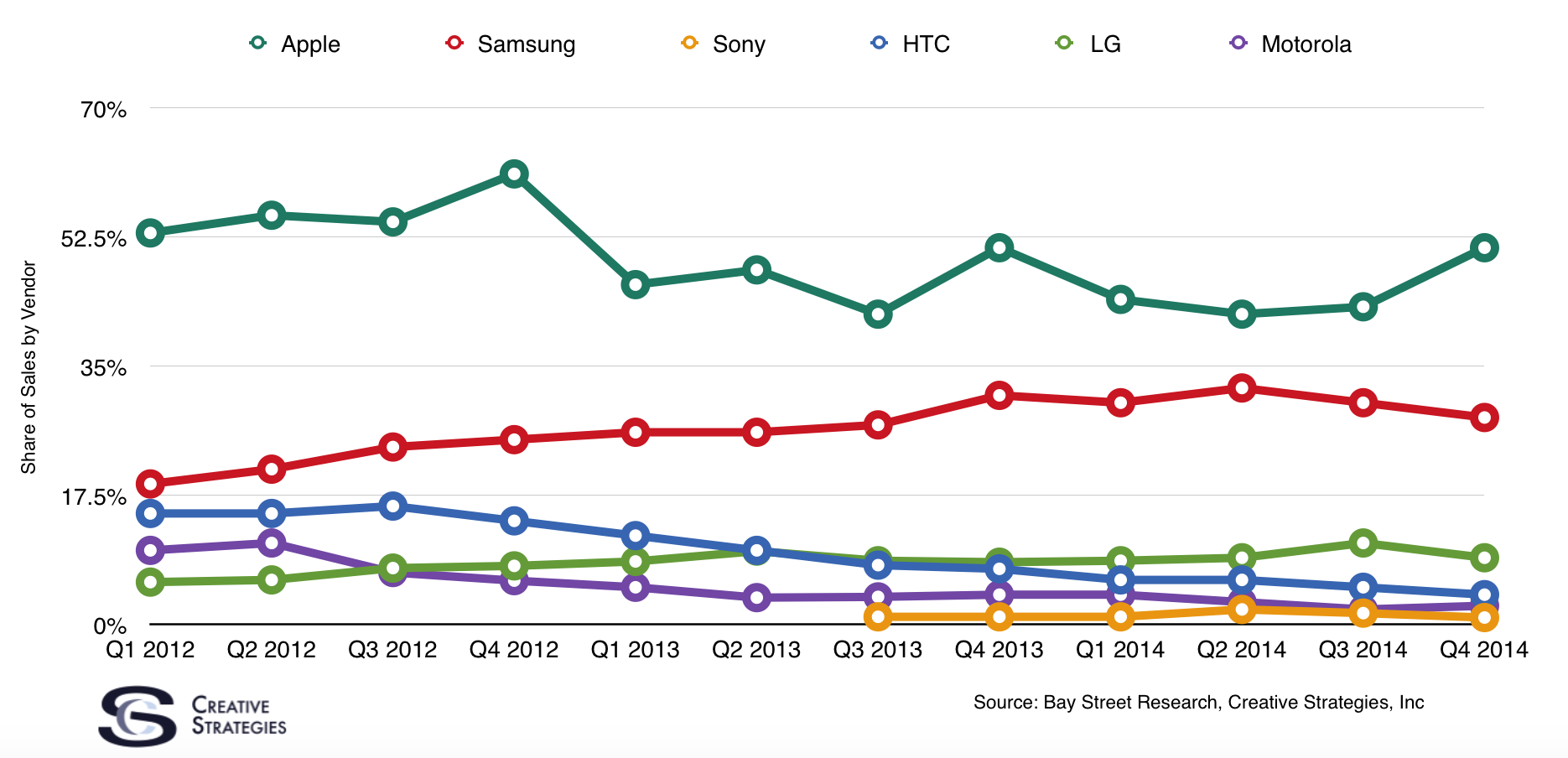

As everyone knows by now, Apple sold more smart phones than anyone else in the quarter. While I don’t chart feature phones, it is interesting to note that Apple became the second largest phone manufacturer as well. Samsung was number one — selling ~95m phones, both smart and feature phones. Apple was #2 overall with 74.5m. Microsoft/Nokia came in at number three at 50m. It is a historic moment as the market rapidly transitions from feature to smart phones. While it is fun to appreciate Apple beating Samsung in Q4, we know it will be short lived as Samsung will be back in the top spot in Q1 2015 and likely sell in the 65-68m range. Apple will likely be in the 57-58m range but could possibly hit 60, largely driven by the Chinese New Year. I’ll update my Q1 2015 estimates closer to March.

Key Regions

I’d like to provide a snapshot of a few key regions broken down by smart phone vendor and by quarter. Let’s start with the US.

The US has always been Apple’s largest market and this quarter they followed a similar pattern — gaining over 50% of quarterly sell through into the US market thanks to the holidays. Apple’s share of the postpaid market was well over 60% and their share of premium smart phone sales was over 70%.

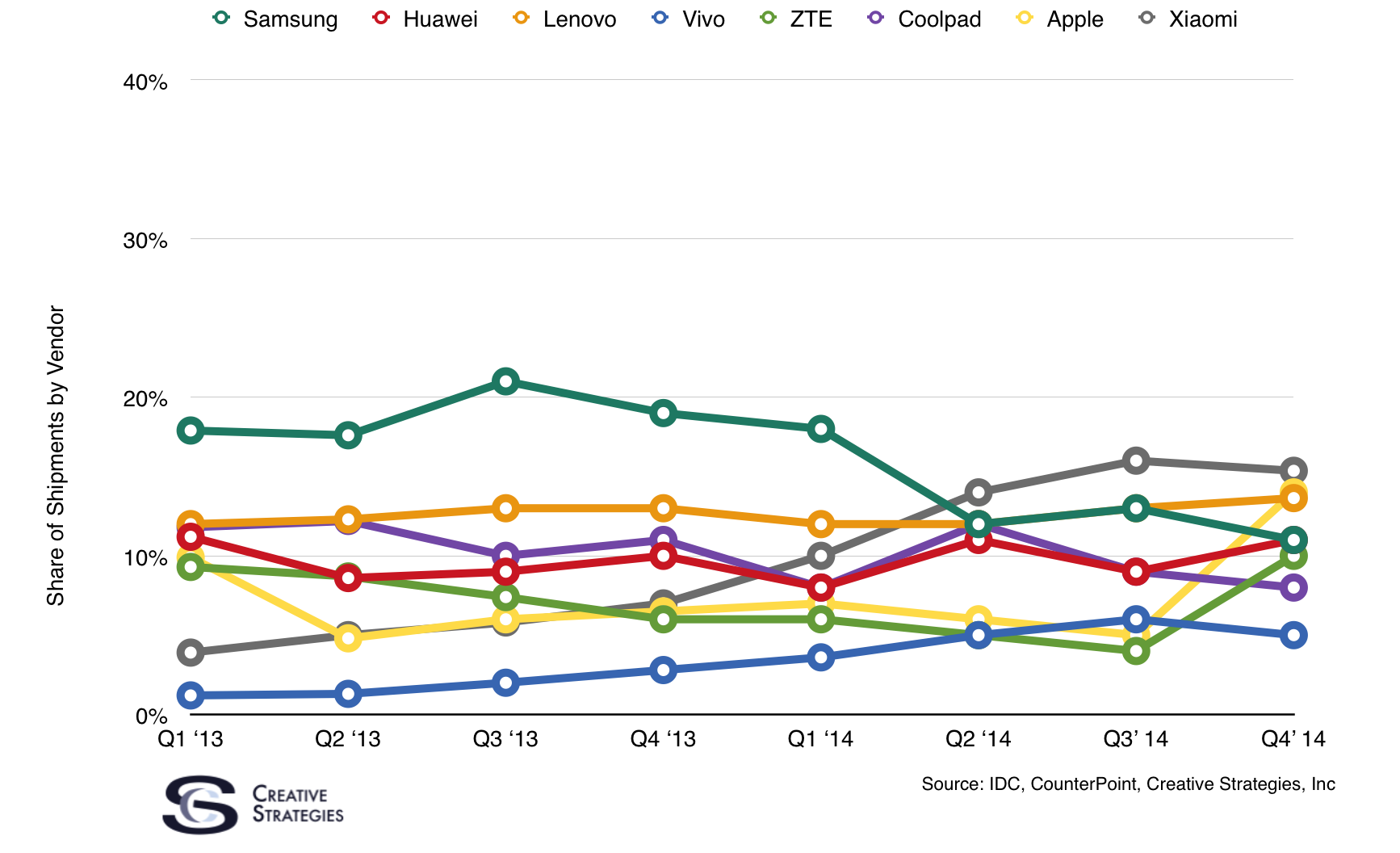

In China, the number one vendor crown was very close between Apple and Xiaomi. So close we will again see analyst firms disagree on this. However, they all will agree it is close. I am able to see some live network data from Baidu/Umeng, which is a challenge because I see how many iPhones, roughly, are active but not all are sold just in China. Some are purchased or imported from elsewhere but still end up on the network. I’ve created a model to help balance this by using what I believe the percentage being imported vs. bought locally is using a range of data points. Based on this model, I have Apple as the #2 smartphone vendor in China but very close to Xiaomi. Here is my chart.

With Chinese New Year coming, this quarter will be fascinating to watch. I’m fairly confident Apple will sell more smart phones in China this quarter than in US for the first time. They may also be the number one smart phone vendor in the region and, this time, it may not be close.

Samsung continues to have significant troubles in China despite being a top 10 brand in the region. Xiaomi also posted their first QoQ decline largely due to the larger iPhones. A key storyline I am watching in China is Motorola. Lenovo moves decent volume in China, but they are perceived as a lower end brand even though some of their hardware is quite nice. Motorola fits nicely into a higher price point, more in line with some of the Oppo and Xiaomi mid-range offerings. All our research continues to show significant interest in foreign brands. Chinese brands are having trouble moving upstream in the market and selling smart phones at higher priced tiers. This creates an opportunity for foreign brands. The key point is that, while ZTE, Huawei, and Xiaomi have their eyes set on international expansion, brands like Apple and Motorola are looking to gain share in the region.

Lastly, India. Other than strong continuous growth, India’s picture has not changed very much. Samsung is still the number one vendor, and Micromax is catching up. Apple is slowly but surely climbing but it is very slow.

Where do We Go From Here

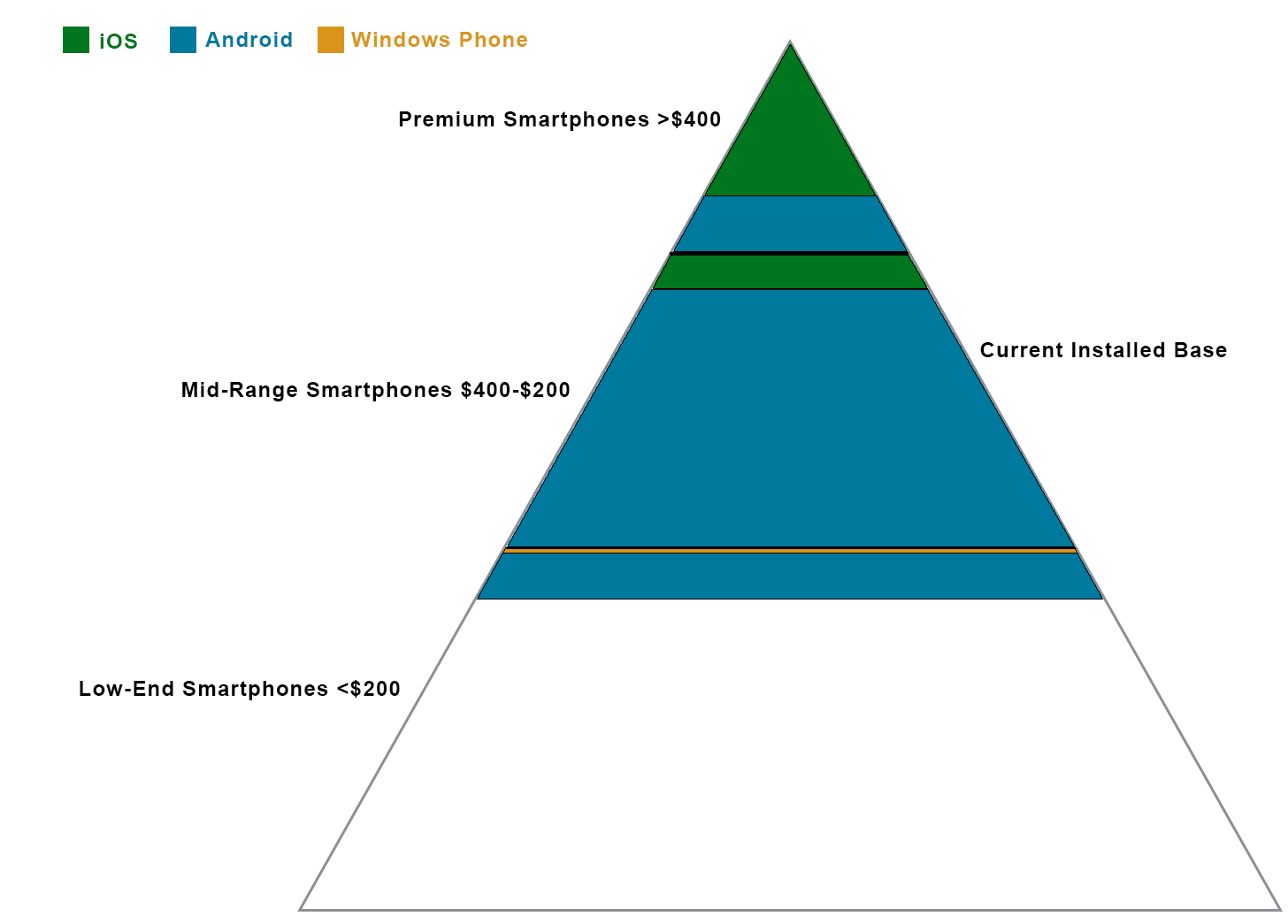

As we look at where we are today, we have to also make some points about where we are going. As I pointed out in my column yesterday, it is clear Apple is getting a near lock on the most profitable segment of the market. As Samsung’s strategy becomes clear, we will cover it for subscribers but the trend lines are not favorable for them to recover much, if at all, in premium. With all the future smart phone growth coming from lower end devices, the next phase of mobile is going to look nothing like the first. These markets will separate and it is unclear what the picture looks like for the next two billion smart phone users. To illustrate this, I’ve created this chart.

This chart is a picture of the current 2 billion smart phone owners. What I’ve done is illustrate the smart phone platform share of the current price tiers. However, at the bottom I have left it intentionally open to highlight that the battle for the next two billion smart phone users is anyone’s game. Certainly Android could grow to fill that gap or maybe it will be an Android fork or alternate platform like Cyanogen. Perhaps Windows Phone is positioned well for the next few billion. Or perhaps something out of left field like FireFox OS. What’s clear is if there is an opportunity for a third OS the opportunity exists in the gap pictured in my chart.

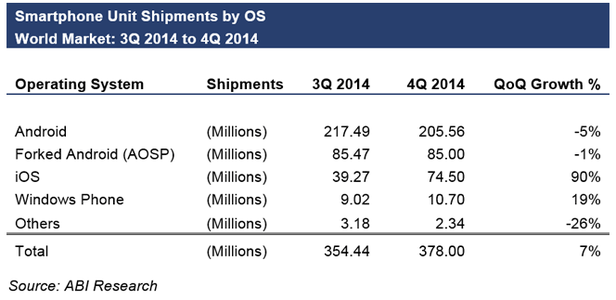

The majority of smart phone’s sold and in use at the end of 2014 were in the mid-range and high end price points. Increasingly toward the end of 2014, we saw an acceleration in phones costing less that $200. Which brings this nugget from ABI Research into light.

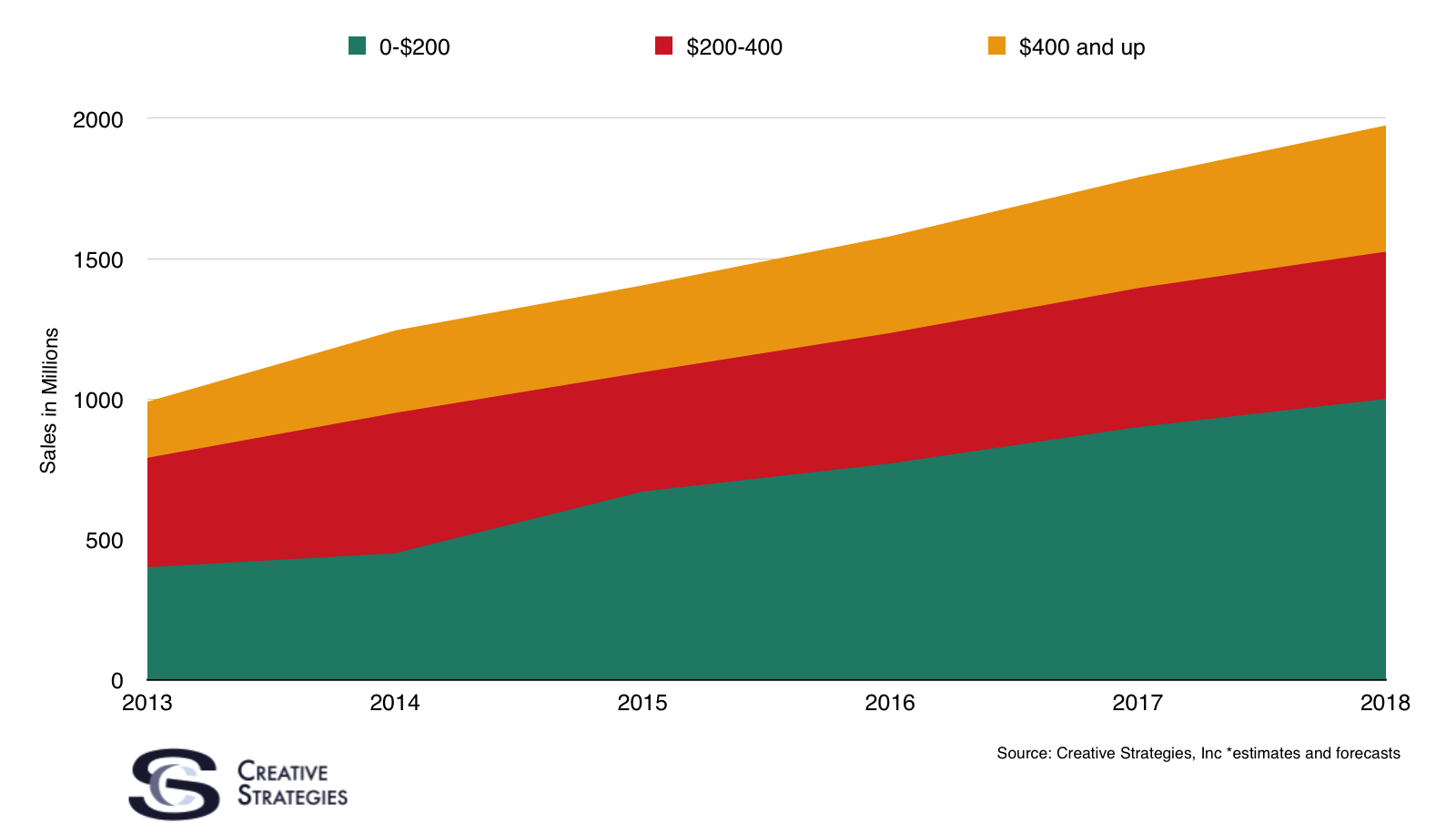

Why did Android smart phones decline? My answer is because the market for smart phones above $200 is drying up. The next phase, as we get out of tier 1,2, and 3 China and into the rural villages, will demand smart phones much cheaper than $200. Similarly in India, getting past the nearly 200m smart phone owners in the region and into the next phase of growth will happen with much lower cost devices. We are in a slight pause, as we look to re-accelerate growth as very good, low cost devices enter the market. Sometime in 2015, we will likely cross the 400m mark for smart phone shipments in a quarter. And this will be the new normal as we near 2b smartphones sold in a single year. To see how we believe that plays out, I’ll leave you with my chart on smart phone price tier forecasts. We will soon be living in a mobile first world.

Thanks!

While I work thru the report, mind explaining “platform’s percentage of the installed base by quarter”? Are unit sales part of that data? For instance, how can Android be 50%?

That is simply what percent the platform’s share is of installed base but tracked by quarter, so the lines stay steady since there are modest net adds to the platform. It would spike one way or the other if there were more than modest net adds to the platform. Take Symbian for example. Their line shows a continual decline in user base. Also note, that is plotted by year ago quarter not sequentially.

It’s hard to interpret from the last chart, but it looks like you’re projecting ~500 million premium phones in 2018. Any estimates of Apple’s share of that segment? I think you tweeted recently that your numbers show Apple had 65% of the premium segment. I don’t know if that was just for the monster quarter or over the past year.

I am yet to see Apple’s share of premium drop below 60%, it got close at Samsung’s peak but never broke it. So I think its safe to assume that is a baseline. And it could likely be higher. However, note that I use above $400 as premium, because I’m assuming there will be some very good premium-isn offerings hovering around that $400 price point. That is why I think the market for premium goes up. I also have a belief that many consumers who purchased phones in the 200-400 range in this first phase of mobile will look to move up as well into more premium tiers as they mature. But good enough “affordable” premium in the Android space will likely hover around $400 so I’m including that into the overall mix to hit that number. If you asked me to break out my tiers by volume of $500 and above I’d have different market size forecasts.

Great post Thank you. I look forward to the continuation.