As an analyst, one of the first things I was ever asked to do was put together a forecast. In fact, a key part of an analyst’s job is to dive deeply into a market, learn as much as you can about what the current market size is, understand where it’s going, and use all the insight you can to make predictions about where it’s headed. While there are some mathematical tricks and a certain amount of scientific rigor that can be applied to the process, it’s fundamentally more of a creative, artistic effort.

At the end of the day, you have to trust your gut and intuition about where you believe certain markets are headed, based on as many useful forms of input as you can ingest. This is really where the magic is, in my opinion, because selecting the right questions to ask about what products are being made, what components are in the pipeline, what tangential trends have started to make an impact, and how people are using the products, is what can help drive a more accurate forecast.

I use those principles whenever I develop a forecast and it led me to foresee a number of things—including a drop in tablets, a turnaround in PCs and an increase in the number of larger 5”+ smartphones—back in the February TECHnalysis Research forecast that were counter to popular thinking at the time. Since then, I’ve completed additional research, including a deep dive into BYOD usage in US businesses and, most recently, my Worldwide Consumer Device Usage study. These have made me realize I need to take those concepts even further.

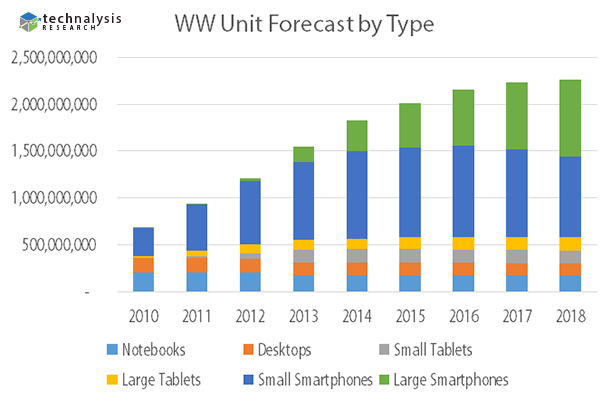

The bottom line is that I’m now expecting the PC market to perform even better than I first predicted, the tablet market to do even worse and the smartphone market to do better exclusively because of an explosion of interest in larger smartphones. In fact, my new forecast numbers show that the tablet market will never catch the PC market, but instead will linger in the sub-280 million unit range through the end of the 5-year forecast period (through 2018). The reasons for this shift are many, but essentially boil down to the fact that tablets have come to be seen more as “nice-to-have” products instead of “must-have” products. In addition, I believe the rapid rise of the 7” category will not only stop but turn into a retreat, due primarily to the expected growth in larger phones. As a result, we will see a shift back towards larger-size 8”+ tablets, with that category taking more than half of the tablet market starting in 2017.[pullquote]I’m now expecting the PC market to perform even better than I first predicted, the tablet market to do even worse and the smartphone market to do better exclusively because of an explosion of interest in larger smartphones.”[/pullquote]

Conversely, I now believe PCs will actually see year-over-year growth this year and then go through a very modest dropoff throughout the next five years, but stay above the 300 million number through 2018. The big shift in PCs is that commercial PCs will become the larger half of the PC market starting in 2016, as businesses around the world will continue to drive PC purchases.

The story for smartphones is that growing interest in larger smartphones will drive rapid turnover of existing devices, even in the US and other markets that have been slower to adopt larger smartphones to date. This, in turn, will lead to the sub-5” smartphone market peaking in 2015, but the larger smartphone category growing to nearly half of all smartphones by 2018.

The chart below shows these forecast numbers in graphical form.

©2014, TECHnalysis Research, LLC

The combined worldwide total of PCs+Tablets+Smartphones, which together I call Smart Connected Devices, will cross 2 billion units in 2015 and peak at around 2.25 billion in 2018. By that point, we will likely have other product categories that need to be considered in the mix, but I do believe the signs are becoming clearer that the decades-long run of compute-intensive devices growing at impressive rates will soon be coming to an end. In fact, from a revenue perspective, my prediction is that 2016 will be the last year of monetary growth for these categories, with modest declines starting in 2017 and continuing forward.

Given these changes, I suspect we will see a number of companies evolve their strategies over time as they adjust to this new world order. Devices will certainly continue to be critical and their sales will not simply go away, but creating software and services that ties these devices and the information they contain together in compelling, useful ways is where the real excitement is going to be.

I think you are dead on, Bob. And I suspect Apple will have the right mix and the quality in its product line to continue as it is.

I see myself eventually having a MacMini, MacBook, the 9 inch Tablet (my iPad 3 is heavy), my iPt till it dies and is replaced by an iPad mini, and the smallest iPhone. That would be five items out of the six you have listed.

There are many reasons I believe that Apple is in the driver’s seat which includes: its quality, product line, its superior functionality, integration, continuous updates to its OS past a products first few years, its practical applications (good enough office alternative), support and its status (status does sell) and security. That’s a lot of points in its favour and there may be others I have missed.

It sounds like my five desires add up to quite a bill, but it would regardless the vendor or vendors one chooses to make such a dream active. But as I have four of the five, sort of, that is only one expense in the next year and probably a couple of years before I decide to upgrade another product. It is manageable because of the mentioned Apple-persistent in build quality, durability and functionality that extends the life of the products past their prime. My iPad 3 may be heavy but how I use it does not make that a major inconvenience and would be the last of my Apple family to be updated.

Another advantage one can use to hedge against the cost of their iProducts is to sell and then upgrade second hand. Such for my iPad and possibly my MacBook comes to mind. The quality build and therefore life of Apple products is so good this becomes a very viable Apple option. The competition may be able to come close to one or a few of the Apple advantages, but integration wise, they are very disadvantaged, hobbled, really.

Namaste and care,

mhikl

Great information shared.. really enjoyed reading this post thank you author for sharing this post .. appreciated

I appreciate you sharing this blog.Really looking forward to read more. Really Great.

very satisfying in terms of information thank you very much.

I discovered your weblog site on google and examine just a few of your early posts. Proceed to keep up the excellent operate. I simply extra up your RSS feed to my MSN Information Reader. Looking for forward to reading extra from you afterward!…

Good info. Lucky me I reach on your website by accident, I bookmarked it.