Both IDC and Display Search released updated numbers for the tablet segment. There are some interesting key take aways from both sets of numbers.

IDC confirms Apple’s dominant position with regards to iPad share and points to slumping Android shipments for tablets which is no surprise. The Display Search data is a bit more comprehensive which includes forecasts as well as OS share in the press release.

There is one thing that sticks out to me and it is related to Windows 8. In the IDC press release they make it clear that Windows 8’s impact is too early to tell. Whereas Display Search takes a stab at forecasting share for Windows 8 and RT but gives the advantage to Windows RT over Windows 8. This is interesting because it implies that from Display Search’s standpoint they do not have much confidence in Windows 8 on X86 but have some confidence in Windows RT to gain some traction in the tablet market.

If you look at the updated numbers from all the major forecasting firms, it is becoming clear that most, if not all, acknowledge that the tablet market could be larger than the notebook and desktop market. Regardless of your belief on that point the bottom line is that tablets and smartphones are the only real growth segments of the computing industry. IDC still is committed to calling all tablet “media tablets” which I think is wrong. There is no doubt at this point in time that tablets are computing platforms not just media consumption platforms.

In Display Search’s numbers, I think they are being overly generous to Android given the trouble it has said so far in tablets. I personally tend to believe that Windows 8 or Windows RT has more of a chance in the tablet market to succeed.

I still remain convinced that Apple will remain the undisputed leader in tablets due to the iPad becoming the standard in terms of tablet computers. In this release, my friend Richard Shim rightly points out that as the tablet market matures there will be opportunities for segmentation within the sector as vendors carve out differentiation.

As with all forecasts we have to take them with a grain of salt to a degree. Things can change quick and a couple of factors, like subsidization, could drive tablet shipments much faster than is currently being forecasted.

The bottom line is, vendors who are not establishing a tablet strategy may very well be left out of one of the hottest segments of computing we have seen in some time.

Let’s take a quick trip in our time machine to survey the smartphone market in the spring of 2007, five years ago. The iPhone had been announced but not yet shipped, and many were skeptical about its success. Android was still mostly a gleam in Andy Rubin’s eye. The hot smartphones of the day included the consumer-oriented BlackBerry Curve and the Windows Mobile-based Samsung BlackJack. The general expectation of forecasters was that Symbian’s dominant market share would shrink, but stay strong, Windows Phone would at least hold its own, while BlackBerry surged and Palm shriveled.

Fast forward to the present. Smartphone unit sales have nearly quadrupled, but the market has become jumbled in ways that few expected. Apple sells nearly one in five of all smartphones, but is the standard against all else is judged. Symbian is disappearing and BlackBerry is hanging on for dear life, especially in developed markets. Android has gone from nothing to a nearly 40% share, while Microsoft, having replaced Windows Mobile with the snazzier Windows Phone continues to bleed market share.

Smartphone Market Share

Operating system

2007

2011

Symbian

63.5

19.2

BlackBerry

9.6

13.4

Microsoft Windows Mobile/ Windows Phone

12.0

10.8

Apple iOS

2.7

18.9

Linux

9.6

—

PalmOS

1.4

—

Android

—

38.5

Other

1.1

3.4

Data: Gartner

Given this background, talking about what the smartphone market might look like in 2017 seems like a fool’s errand, but I’m going to take my chances. To some extent, smartphones are beginning to look like a mature market, at least in North America, Europe, and Japan. One characteristic of mature markets is consolidation of producers. And in the case of smartphones, this trend is complicated by the delicate interplay of handset makers and operating system providers.

The hot issue of the moment is the pressure toward combining hardware and software into vertically integrated producers. This thinking has been inspired by the staggering success of Apple, though it requires overlooking the struggles of vertically integrated Research In Motion and the implosion of Hewlett-Packard/webOS.

Ingtegration and consolidation. The industry seems well on its way to more integration and more consolidation. My colleague Tim Bajarin thinks that despite its demurrals, Google will make an integrated Motorola the prime producer of Android products. There’s a lot of reason to believe that if Microsoft doesn’t buy Nokia outright, it will formalize an arrangement in which Nokia becomes its official premier Windows Phone partner. I think both Nokia and Motorola will end up as the official flagships of their operating systems.

Apple should be able to fly above this storm. As demonstrated by its latest blowout quarter, there is every sign that it will be able to hold on to the high end of the business for some years to come. The iPhone has lost some market share, and this trend will continue because much of the growth over the next few years will come as low-end smartphones displace feature phones in markets and geographies that are not Apple’s métier. But Apple doesn’t much care about market share; it will dominate the much more important categories of mind share and profit share.

The company most threatened by MicroNokia and MotoGoogle is Samsung, which has just displaced Nokia as the leading phone maker by worldwide unit volume. Samsung is highly integrated on the hardware side. It makes its own processors, displays, and flash memory, among other components. But it has never been a leader in software. It has its own operating system, but Badu has gotten little traction and for its high-end phones, Samsung depends on Android and Windows Phone. Samsung is not going to be happy as a second-class manufacturer for either Microsoft or Google.

Samsung’s tough choices. Samsung’s options, however, are limited. It could buy RIM, which seems destined to fade away unless it can team up with someone. But given RIM’s struggles trying to bring a new BlackBerry operating system to market, this might not offer Samsung much of a solution. A more promising course might be for Samsung to claim an open-source operating system as its own. It’s partnering with Intel on a mobile OS called Tizen, but this seems headed for the same ash heap as Intel’s other OS efforts. (Meego, anyone?)

webOS offers a more intriguing possibility. HP owns it, but has open-sourced the code and made it freely available. It’s a sophisticated modern OS that needs work, but one that Samsung might be able to use as its own platform for phones and tablets. Another possibility would be simply to grab Android and definitively strike out with its own fork without regard to Google’s development path. Either course would require Samsung to get deeply into software development, developer relations, and everything else that goes along with being a full-service provider. This has not been a Samsung strength, but the alternatives may be far worse.

One way or another, I expect Samsung to be a significant player in the 2017 phone market. I’m much less sure about the smaller Android and Windows Phone manufacturers. HTC, with a foot in each camp, has stumbled of late and could have difficulty getting its mojo back. I would not be at all surprised to see Sony, which recently became the sole owner of what had been Sony Ericsson, exit the phone business after struggling, successively, with Symbian, Windows Mobile, and Android. LG, which has never quite gotten the hang of smartphones, could also leave the market. ZTE, Huawei, and Lenovo can trade on their strength in the Chinese market, but may make little impact elsewhere.

The market in 2017. In unit volumes, the 2017 smartphone market will be dominated by low-end phones sold in emerging markets. If Nokia can survive the stormy present, either in partnership with Microsoft or as part of it, the combination of Nokia’s strength in these markets and Windows Phone’s ability to perform well on modest hardware , could again make it a formidable player. Android may be a big force in two flavors, the official one and a Samsung variant. Many of the smaller phone makers will be out of the market. RIM will hang on in some form, perhaps as a supplier of back-end enterprise services and specialized secure phones. And Apple will be Apple.

The biggest question mark is MotoGoogle. Left as it is, it seems doomed to become a second-tier Android handset maker, some thing of little use to Google. Integrated and turned into an Android flagship, it puts Google head to head with Apple and possibly Microsoft. It would probably forsake the current Android licensing model, which is not working very well anyway, and would have to develop new talents such as supply chain manage, channel strategy, and carrier relations. Google has the money and the brains to do all this, but I’m not sure it has the desire, patience, and discipline to pull it off.

First let me clarify that due to my line of work I do not invest personal money into any public tech stock. That being said, even if I did, I would not put my own money into Facebook when they go public.

This has been an interesting week for Facebook. They acquired an extremely popular piece of software for iOS and Android called Instragram for roughly $1 billion dollars. Instagram had an extremely loyal, engaged, and opinionated customer base (judging by their harsh reaction to the acquisition). In fact, fellow Tech.pinions columnist Patrick Moorhead wrote in his Tuesday column about the conversation he had, via text message, with his daughter after the deal was announced. If you haven’t read it already I encourage you to read it as she very deliberately called Facebook stupid and for old people, which is in fact the title of his column.

Along those same lines I wrote a column for TIME in December entitled “The Beginning of the End of Facebook?” This column led to a raging debate in the comment section as some folks disagreed with me and others felt that Facebook may not be the king of social networks forever.

Facebook Becomes Routine

My premise was simple. I interviewed approximately 100 high school students in Silicon Valley, all who have been on Facebook at least two years and many had been on for four years or more. In every case with every interview the results were the same. They found themselves using Facebook less and less and were generally using it to simply get quick updates of friends and family. Since that column (and if you read the comments) I have gathered over 100 more responses all indicating the same thing. Those who have been on Facebook for a significant period of time see their time spent with the service decline.

Yet comScore tells an opposite story. The year over year increase of individuals average monthly minutes on Facebook is increasing at almost 50% each year. Now, comScore is looking at the total number of minutes not the number of minutes an specific individual averages. I am not sure if it is possible to track this but I would be 99% certain that the average number of minutes per month spent on Facebook actually declines the longer you have been on the service.

In my own experience and in many of the high schoolers I spoke with, the first year or so on Facebook was the most intense. Discovering and keeping up with new or old friends. The lure to share socially and show off all the things you are doing, eating, etc. All of it becomes very addicting, but after a while that drive goes away. This is at the heart where I think the problem with Facebook lies. It commands a high average of a persons time for a short while but then Facebook becomes more of a routine rather than a passion.

The numbers that ComScore is observing is because much of the globe is still having its first year on Facebook. There is also no doubt in my mind that even for those for whom Facebook becomes routine go through a season of more intense usage. Like when a friend or loved one goes on a trip or moves to a different location.

However, even with my theory of average time spent declining and the longer a consumer has used the service is correct, it is only one small part of why I wouldn’t put money into Facebook. Ultimately, however, I don’t believe the time spent on Facebook averages we are seeing today is sustainable in the long term.

The Economics of Pleasing Everyone

The problem I see with Facebook’s business in the long term is that it is trying to be all things to all people. Within that vein of thinking it is also trying to develop an advertising / revenue strategy that is also all things to all people. Generally speaking, when a service tries to be all things to all people, it is not actually good for anything.

In 2008 I was on a panel at the OnMedia summit in NY talking about this very thing. I highlighted a few networks of interest at the time. One was called Dogster.com which still exists today and is simply a social network for those passionate about Dogs. It links people up by region or just by type of dog in order to link up people of like minded interest in dogs or even certain types of dogs.

Similarly a few years prior I was spending quite a bit of time with the folks of LaLa.com and its founder Bill Nguyen. As you may know Apple has since acquired LaLa and used its technology to build Ping into iTunes. The premise of LaLa.com was simple in the beginning. Link people together who had similar tastes in music and let them help each other discover new music. The results were as expected as for quite a length of time LaLa.com’s average time on site per customer exceeded two hours per day. The allure in the case of LaLa.com was like minded people and the discovery of new music. Lala’s customer base continued to spend significant time on the service until LaLa changed their strategy.

This is the power of vertical social networks and where I believe the best advertising strategies will lie in the future. In the case of Dogster.com the community is an extremely interested one in all things related to dogs. If I was the head of marketing at Purina, would it make more sense for me to advertise on Facebook or Dogster? Similarly, how about social networks for car lovers / aficionado’s, mothers, fitness fanatics, artist lovers, etc. The total size of one of these vertical networks may not be nearly as big as Facebook’s but the target audience would more engaged, more targeted, and more passionate about the interest and thus more valuable to advertise to in my opinion.

We are already seeing these vertical networks creep up and I assume we will see many more in the future and this reality isat the root of my concern over Facebook’s long term sustainability as a profitable business. My concern is that these vertical social networks will become more valuable to brands and advertisers and command more of their ad spends than does Facebook.

The bottom line is that if I am a brand looking to advertise to a certain type of consumer, I am going to want to go where those consumers are in big numbers. My belief is that brands will find more success marketing with vertical social networks that are oriented around special interests rather than a network like Facebook which is trying to be all things to all people and not doing a good job of it.

Steve Jobs said of the PC as he was developing his post PC theme, “PCs are going to be like trucks; less people will need them. And this is going to make some people uneasy.” Well he was right, if not accurate. A whole lot of trucks are sold. In just the US in February 2012 612, 145 cars were sold, and 537, 251 light duty trucks were sold, plus an additional 225,621 Cross-over trucks. So more trucks sold than cars, and even if you add SUVs (97,825) to the cars, there were still more trucks sold in the US, and that’s not counting the bigger ones that chew up your streets and bring stuff to your shopping center or gas station.

No doubt about it tablets and smartphones are popular and selling well. What most folks seem to miss (or want to miss) is we do have cars and trucks, and motorcycles, and we will continue to have smartphones (motorcycles), tablets (cars?), and PCs (trucks?) Because Tablets are popular doesn’t lead to the conclusion that PCs suddenly aren’t. But if all you’ve got to sell is a tablet, well then the world looks a little different. And even if you have a truck to sell, if it’s getting hammered by the competition, but your car or motorcycle is showing a better margin and/or shipment level, well your interest and emphasis is pretty predictable isn’t it?

So Apple wants to promote the “Post PC” concept as a way of casting the PC in a no longer important, been there done that, obsolete technology. And because they are Apple, the only company capable of original thought or charisma, and the role model for all other computer, electronics, and phone companies, the term “Post PC” will be adopted, and heralded as the coming, the new era, the I’ll follow Apple into hell slogan of all the wantabees—which is everyone from Microsoft to the smallest Chinese cloner.

Actually, Apple makes life so much simpler for the rest of us. We don’t have to invest time and money in clever ideas, or marketing, we just have to wait for Apple to tell us what’s cool now and then copy it as best we can.

The PC/Tablet/Phone industry reminds me of a bunch of teenage girls, watching the cool girls in order to find out what is in and what’s out. Nobody wants to get caught with something that’s out and not cool, that’s worse than a zits breakout on prom night. And it’s a caution to the buyers of all this non-Apple, Apple defined cool stuff. If the company you’re considering buying something from is an Apple follower you should think twice about buying anything from them. It’s unlikely they are going to be a faithful supporter of that currently cool copycat thingie—you’d be better off buying the real deal from Apple.

But it’s tough not being Apple when it’s so big, so rich, and so trend setting. Right now the only company that seems to have a chance at standing up to Apple is HP. All the rest are still in the beige/black box PC world where this year’s machine looks just like last year’s machine and the year before it. Where this year’s big breakout product is an Ultrabook that looks like every other Ultrabook which in turn is trying to look like Apple’s Air. It’s pathetic.

So if the PC industry turns into the unexciting truck industry, regardless of shipment numbers, it’s its own fault for being lazy and scared – get some backbone PC makers, take a chance—do something original. You might find you actually like it.

As I was reflecting on my first experience with the new iPad and its retina display I was intrigued with a thought. There has always been something about the iPhone’s retina display and now with the iPad’s display that has me mesmerized. When I first saw the new iPad and the screen at Apple’s event I couldn’t stop looking at it. Even today I sometimes just turn it on to look at it and shake my head in disbelief.

The thought that I was intrigued by is how the visual appeal of Apple’s devices, and in this case of the screen, causes us to be so emotionally attached to them. Even this NY Times article in September of last year points out that consumers do actually love their iPhones. I believe this affect however as everything to do with the visually appealing experience with Apple products.

In a TIME column I wrote last year, I pointed out that Apple’s desire to create products that are at the intersection of liberal arts and technology drives them to create technology products that are in essence art. Apple turns technology into art we can use. Apple exhibits an unparalleled focus in the technology industry to design some of the most visually appealing hardware in all of computing. This focus of creating objects of desire is one part of many that encompass the Apple experience. That experience, the visual and emotional experience tied to Apple products creates an emotional response in consumers of Apple products that create as much passion around a brand as I have ever seen.

The Most Passionate Community

I would challenge you to find a more passionate community anywhere in computing. I have attended many industry conferences and trade shows and the Macworld’s where Steve Jobs spoke had a level of energy associated with them that I am yet to encounter anywhere else in this industry.

The experience around Apple products is what I think many who compete with Apple take for granted and simply don’t understand. I’ve said often at industry talks I have given that consumers don’t buy products they buy experiences and that is what Apple delivers.

Consumers in droves are discovering what the hard core long time Apple community has known since the beginning and are converting in droves buying iPads, iPhones, and even Macs. It all leads with the visual experience and beautiful and attractive hardware. Believe it or not, however, beautifully designed things are easier to use.

What is Beautiful is Usable

In 2000 a scientist from Israel named Noam Tractinsky, wrote a book called “What is Beautiful is Usable.” He started with a theory and built the scientific evidence to back it up. To quote his report on the subject:

two Japanese researchers, Masaaki Kurosu and Kaori Kashimura1, claimed just that. They developed two forms of automated teller machines, the ATM machines that allow us to get money and do simple banking tasks any time of the day or night. Both forms were identical in function, the number of buttons, and how they worked, but one had the buttons and screens arranged attractively, the other unattractively. Surprise! The Japanese found that the attractive ones were easier to use.

Noam himself then wanting to test this theory with the Israeli culture so he duplicated the experiment. He thought that aesthetic preferences may be culturally dependent. His observation was that the Israeli culture is more action oriented and they care less about beauty and more about function. However when he duplicated the results with an Israeli group of people the conclusion was the same. In fact in his research the sentiment was stronger with the Israeli sample size. So much so that in his research report he remarked in his paper that beauty and function “were not expected to correlate” — He was so surprised that he put that phrase “were not expected” in italics.

It appears that Apple has been on to something from the beginning. Perhaps Steve Jobs absolute resolve to make technology products beautiful carried with it inherent user experience paradigms that simply made products easier to use and that theme is continued today all throughout Apple. This in my opinion is truly what is setting Apple apart in the market place. They create objects of desire and out of that focus comes a visually and easy to use user experience paradigm that drives emotional responses in consumers of their products.

We know humans are visual beings, especially men, and interestingly enough a great deal of science exists today linking beautiful things to ease of use. There are companies who can design objects of desire and easy to use products and there are those who can’t. Apple’s advantage in this area is that they create the hardware and the software with this technology and software as art philosophy. We see this in their hardware and their software and will eventually see it more in their services.

Noam Tractinsky is right and his book title highlights a profound truth. What is beautiful is usable and this philosophical truth carries over into computing and human interaction with computing.

Right now there is only one company who I think truly understands it.

References:

– Don Norman, Why We Love (or Hate) everyday things, Feb 4th 2003

– Tractinsky, N., Adi, S.-K., & Ikar, D. (2000). What is Beautiful is Usable. Interacting with Computers, 13 (2), 127-145.

– Tractinsky, N. (1997). Aesthetics and Apparent Usability: Empirically Assessing Cultural and Methodological Issues. CHI 97 Electronic Publications: Papers

The recent 2012 WW forecast for tablets from IDC which forecasts sales of 106MM units in 2012 with Apple’s iPad numbers at a little under 60MM has been widely picked up and republished across the internet. The report also predicted that Apple could lose dominant marketshare to the Android platform by 2015. Windows tablets do not figure in the IDC forecasts as currently IDC defines them as PCs.

While I’ve a lot of respect for IDC’s ability to identify key market trends, especially in the Enterprise IT market but I’m not convinced they have their finger on the pulse of the Apple iPad market nor Apple’s iOS strategy.

It appears that IDC has consistently under-estimated the iPad market since its launch and their recent forecasts seem to follow that pattern. Just to verify my suspicions I looked back at the IDC forecasts since the launch of the iPad on April 3rd 2010 when Apple sold 300,000 iPads on the first day and 3 million in the next 80 days.

I recall at the iPad launch IDC analysts noting that the iPad would do remarkably well if they sold 5MM units by the end of 2010. IDC subsequently estimated the total number of all tablets to be sold in 2010 at 7.6MM units. But when the final numbers were reported, Apple alone had sold nearly 15MM units. IDC’s forecast for 2011 was set at 44.6 MM units (the final sales for 2011 came in at nearly 69MM units with Apple selling 40 MM units). IDC first predicted 2012 sales of 70.8 MM units – this forecast was increased to 88 MM units and now stands at the 106 MM number announced by IDC a few days ago.

Based on the historical sales growth and the launch of the new iPad it is hard to believe that Apple will sell less than 60MM units in 2012.

With 40MM sales in 2012 – at least a doubling of that number is to be expected. Unlike the original iPad, which initially launched in the US, the new iPad will be sold in 36 countries by March 23rd. The combination of the price reduction on the iPad 2, the new iPad (third generation) and the highly likely launch of the 7.85′ iPad Mini for $299 should drive Apple iPad sales to well over IDC’s forecast number and I suggest that a number well above 80MM units is achievable for 2012 with an annual run rate of over 100 MM units.

IDC is hardly the only analyst firm underestimating Apple’s potential but is one of the most conservative.

The research company also predicts that Android tablets will have a higher market share than the iPad by 2015. Many have predicted that the growth of Android tablets will follow the success of Android smartphones but the markets are very different. The predicted success of Android tablets has not happened so far. The only tablet to get any traction is Amazon’s Kindle Fire. Amazon’s Kindle Fire is a gateway to Amazon’s retail store – it’s not really a tablet strategy – it’s a commerce strategy. To boost their m-commerce platform, Amazon is likely to drive their hardware sales by aggressive pricing – to near zero (perhaps even bundling the Kindle Fire with the Amazon Prime Free Shipping Service).

However, Amazon, if they could negotiate terms with Apple (which is a tall order) could be better off having a Prime app on the iPad rather that being in the hardware business.

At the low end, Android tablets may see some traction where they will be used low cost mobile web browsers and simple readers – especially in emerging countries where low pricing is essential to drive sales. But will customers want a product that has limited functionality, a sub-optimal experience and does not come with a massive eco-system of applications designed specifically for the device?

When Apple launched the iPad many questioned its role as a “Tweener” devices between the smartphone and the PC. Apple was however able to define the category due to the quality of the product, the user interface and experience but more importantly the totality of their eco-system -hardware, software, an apps development platform and a massive distribution system via iTunes.

No other company gets close – so today, we don’t really have a tablet market – we have an iPad market. Note that Apple never refers to their product as a tablet – as they associate the tablet with Microsoft’s earlier failures.

Apple’s dominance of the tablet market has significant implications for media companies. Most have assumed that some equilibrium will eventually come into the tablet market, so a strategy of delivering content across multiple devices was a safe distribution strategy, even with the challenge of optimizing for many different devices. The publishers’ consortium Next Issue Media (made up of Condé Nast, Meredith, Hearst, News Corp and Time) decided, after negotiating difficulties, to eschew the Apple platform and support Android. A decision they are probably regretting. The success of the iPad platform lured each of the consortium members to find a way to eventually work with Apple so the value of the consortium is unclear if they remain solely focused on Android.. The question media companies now have to answer is whether the competitive platforms to Apple’s iPad can do justice to their digital publications. Can these platforms meet reader expectations or provide a significant large enough digital distribution channel to drive user and advertiser revenues ?

Apple will never compete for the low revenue, low margin low quality “budget” end of the market. Apple will always prefer a lower marketshare position so long as they maintain a high revenue and margin share of the segment. It’s possible that eventually the sheer numbers of very low cost tablets could outsell Apple’s premium products but I doubt it. Customers won’t be satisfied with an underpowered tablet any more than they were satisfied with the concept of the netbook. It’s much more likely that as smartphones increase in capabilities and significantly drop in price that they will be the mobile devices of choice in emerging markets. The functionality of even low cost smartphones will be superior in virtually every case to low cost tablets (other than display size and even then, foldable displays, 3D and projection could step in to solve that issue).

The tablet expected to take share from the PC market, overtaking it in unit sales by the 2015/16 timeframe. There will be a few specific cases where PC will remain superior to tablets in input and processing power, but that gap will narrow over the next few years and customers will flock to the convenience of the “tablet”. However the size of the tablet market , while significant, is never going to get close to the volume of the smartphone market which will be measured in billions.

We’re living in a world of digital mobility – it’s a multi-screen world – currently the dominant displays are smartphones, ultra-portable laptops, tablets and the TV but as the Corning Concept video suggests that will evolve. Apple’s goal is to take significant market share in each of the segments and bind them all other with an iOS platform that attracts the world’s best developers.

I don’t have IDC’s resources, contacts or detailed knowledge of the industry but I’ve been around the Apple marketplace for 25 years. My predictions are based on both gut and industry instincts – but are far from scientific but I’m willing to wager my 2012 estimates of iPad will be closer to the mark than the IDC forecasts. For the record I predict Apple will sell over 1MM units on March 16th. It will sell close to 10MM new iPad units within the first 30 days of launch as it rolls out t in 37 countries and in 2012 the total sales of iPads will be in excess of 90MM. My colleagues at IDC are willing to bet a nice bottle of wine that they will end up being more accurate than I am. Sounds good to me and no matter who wins I look forward to sharing it while we develop our own 2013 predictions for this exciting, emerging market.

Apple’s stock price is currently around $600, valuing the company over $500 billion. Already analysts are upping their target range to $700. If Apple continues to execute as well as it has this may too be conservative. I only wish I had the foresight to hold the Apple stock I purchased back in 1997.

Fights over intellectual property rights have become so much a part of the tech scene that it sometimes seems the industry employs as many patent and copyright lawyers as it does engineers. And if the fights over software patents and music, video, and book copyrights weren’t enough new technologies allowing anyone to become a micro-manufacturer could become the next front in this running battle.

The Makerbot Thing-o-Matic 3D printer.

3D printers costing as little as $1,000 let you turn a computer-generated design into a plastic object almost as easily as a printer turns a Word file into printed pages. 3D scanners can turn physical objects into printable designs. Much more expensive commercial machines can print in a large variety of materials, including aluminum, titanium, stainless steel, glass, and ceramics. Low-cost computer-driven milling machines and laser cutters can do jobs that printers can’t handle. And if you don’t want to do the printing yourself, companies such as Shapeways are becoming the Kinko’s of custom manufacturing; send them a file and they’ll ship you a part.

Some tech-optimists see 3D printing as a solution to many of the world’s problems. In a posting announcing that it would be distributing plans for printable objects it calls “physibles,” The Pirate Bay announced:

“The benefit to society is huge. No more shipping huge amount of products around the world. No more shipping the broken products back. No more child labour. We’ll be able to print food for hungry people. We’ll be able to share not only a recipe, but the full meal. We’ll be able to actually copy that floppy, if we needed one.”

This, of course, is cheerful nonsense. Printing food, for example, would require an edible feedstock, meaning there is no net gain for anyone.

But the technology does make it easy to make copies of a large variety of objects, from toys to replacement parts for your bicycle. But is it legal? After all, the availability of Xerox machines made it possible to copy books and software lets you copy DVDs, both activities that constitute copyright infringement.

It may come as surprise, but in general, physical objects enjoy little or no intellectual property protection. With some specific exceptions, such as sculptural works of art and buildings, physical objects cannot be copyrighted.

Of course, there are other forms of protection. Trademarks, for example. You could copy a Nike sneaker—the technology doesn’t actually exist to do that yet, but it will—but putting a swoosh on it would violate Nike’s trademark. There’s a fuzzier part of trademark called trade dress that can protect the general appearance of an item, but to win it, the product must be very well-known and immediately identifiable, like the classic Coke bottle. Finally, there’s the possibility that your copy will infringe on someone’s patent. Even an object you design from scratch could inadvertently violate a patent though most of the time, replicating part of a patented device does not infringe. (For more detail on the fine points of the law, see the wonderfully titled Public Knowledge white paper “It Will Be Awesome If They Don’t Screw It Up” by Michael Weinberg.

The danger is that industrial incumbents will fight to strangle this baby in the crib. For many industries, the selling of replacement parts is a lucrative business. Until 3D printing came along, though, it was simply too difficult and expensive for anyone to bother making competitive parts. One exception was the auto industry, where the huge market for replacement body parts made it worthwhile for third-party manufacturers to take on the huge cost of tooling to make copies. The auto industry has tried and failed to shut down this “crash parts” business for decades, though it recently has had some success using design patents.

Some companies have tried to sneak physical products under the protection of the digital Millennium Copyright Act. Lexmark, for example, included a chip in toner cartridges that contained computer code. It argued that replacement cartridges made by Static Control Components infringed its copyright by copying the code. But in an important ruling, the 6th Circuit Court of Appeals found that adding computer code for the purpose of extending copyright to something otherwise not protected was unacceptable.

There’s a good chance, though, that as 3D printing becomes easier, cheaper, and more popular, industry will try to legislate new protections. This time, however, I think the tech world and the spirited “maker” community can prevail. First, as the fight over the Stop Internet Privacy Act showed, it is much, much easier in Washington to block legislation that to pass it. The system is heavily biased in favor of inaction.

Second, this time the community is forearmed. The tech industry paid little attention when the DMCA was being debated in the late 1990s and to the extent it got involved, it deferred to big software companies such as Microsoft and Adobe, which wanted strong protections against piracy. The industry was a bit slow to rally to the anti-SOPA cause, but once it did, it proved effective.

The use of information technology to make physical object is an important new frontier. Let’s hope, in Weinberg’s words, that they don’t screw it up.

Not long after the new iPad was announced, story after story was written that this new iPad was evolutionary, not revolutionary. But I am not convinced that is a correct viewpoint. In fact, I believe that this new iPad will actually have a revolutionary impact on the market in some very interesting ways.

Some Historical Perspective

Back in 1981, I wrote the first report on what was to become desktop laser printers. At the time, laser printers were as large as mainframes and took up much of a 9’ X 12’ room. But I had seen Canon’s laser printer engine and wrote in this report that by using this type of technology in potentially desktop sized printers, I could imagine a day when we could publish documents on our desktops. Now, this was three years before postscript laser printers hit the market and before Aldus’s Pagemaker was introduced.

Not long after this desktop sized laser printer engine was shown to Steve Jobs, he made a fortuitous decision to build an Apple laser printer of his own. And after being convinced by John Warnock (co-founder of Adobe) to include Postcript as its software engine, Jobs put in place a key component of technology that would put Apple on the map. Not long after that, Paul Brainerd created a Mac product called Pagemaker and together, these two products launched the desktop publishing revolution. Although Jobs embraced both products, I am pretty sure he and even the team at Apple never really understood the magnitude of these products impact on the world of publishing at first. For Jobs, the decision to back a desktop laser printer was totally out of order given Apple’s PC centric business model and those around him argued loudly with him about doing this product.

But we now know that Steve Jobs’ stubbornness about introducing a laser printer had its roots in his desire to have a digital version of his calligraphic type fonts replicated through this printer. And from that point on, while at Apple until mid 1985 and at NeXT, the issue of high quality graphics took center stage on every product Steve Jobs touched. And when he came back to Apple, this was still top of mind. By the way, I worked on multiple desktop publishing marketing programs for Apple, MacWorld and various hardware and software vendors who were doing DTP like products then and saw up close how Apple single handedly rewrote the rules of electronic publishing, something we now take for granted and use every day when we create our own newsletters, Web pages, etc.

The New iPad

In the column I wrote not long after the new iPad was launched, I pointed out that from the inception of the iPad, Jobs wanted it to have the highest resolution screen possible but that at the time of the release of the first two generations of the iPad, the technology was not there to deliver the real iPad he wanted to give his customers.

But it was always on the roadmap and they had to do some serious engineering between their team and their partners to get us this new iPad to this incredibly high resolution. And with it, I believe Apple is ready to have another revolutionary impact on the market via one of their products.

One good example of this will be in medical applications. Although doctors and hospitals have actually been adopting and using iPads in pretty big numbers, this new iPad will become a must have tool soon. The reason is that with the older iPads, the information they were processing on it was mostly data driven. But as you know, doctors rely on a lot of things like xray’s and digital imaging to help them make key diagnostic decisions. For final analysis they will always defer to industrial strength 10K graphics workstations, but the new iPad with its high resolution screen will now be able to give them on-the-go images that can deliver much more imaging details then they had on their original iPads. This will become an important part of their ability to do immediate analysis and will now become the minimum level of tablet graphics quality they will accept in their medical practices.

Another example will be its impact on catalogs. Apple recently released the new catalog category in the iTunes store but I have talked to some catalog vendors who consider today’s tablets inferior for delivering the graphics quality they demand in their print catalogs. A good example might be Restoration Hardware. They pride themselves in delivering one of the greatest graphics quality catalogs on the market and would have never even considered doing a digital version for the older iPads. But for them and any other vendors for whom high quality images are critical to their catalog sales processes, the new iPad will be revolutionary for them. According to Joaquin Ruiz, CEO of Catalog Spree “With ultra-sharp pictures, text and video, the new iPad is perfect for all forms of publications. March 7, 2012 will be remembered as a landmark for publishers from news, to retail, to education, and to books.

The folks involved in engineering, oil and gas exploration and nuclear energy research will also see a higher resolution iPad as a welcome mobile tool that will become a key part of their on-the-go digital tool-belt. And don’t count out this high resolution iPad’s role in education. This new iPad will deliver a much closer representation of textbooks, especially ones that have a lot of images, graphics and diagrams, and to students it will become the minimum resolution they will accept in a tablet that will soon carry all of their textbooks.

When Steve Jobs introduced the iPhone, he said he would be happy if Apple could get even 1 percent of the cell phone market. An understatement if there ever was one. And even with the iPad, while Jobs used a lot of flowery language to describe it, he was cautious in declaring what type of impact it would have on the market.

At the launch of the new high-resolution iPad, Tim Cook and team–I believe–clearly understated what this new iPad’s market impact will be. All they said was that it was a newer and better version of the iPad and that they were pleased they could deliver a new tablet with a much better screen. But don’t let that fool you.

I believe we will look back relatively soon and realize that with this iPad, Apple started another revolution that has it roots in their desktop publishing heritage and instead of desktop publishing this time around, the revolution will take place in mobile publishing. The result will be to extend Jobs and teams original mantra that was, “What-You-See-is-What-You-get,” but this time it manifest itself on the new iPad. Think of the new iPad as the new representation of Steve Jobs’ laser printer’s paper. And its influence will touch every market. It will drive what I believe will be the minimum standard in tablets as tablets become the vehicles for every form of mobile publishing content, whether it be images, video, games, newspapers, magazines or books as well as the future of the web.

With the Nexus One and their recent purchase of Motorola, Google has more then signaled that they will soon be in the hardware business in a big way. And the recent rumors that they are building a 120,000 square foot consumer experience testing center on their campus suggest that they will test their own hardware along with partners products in order to create and deliver devices that are truly optimized for their Android and Chrome software.

This move is of course controversial since it means that they will be in direct competition with their customers and partners who back Android and Chrome. However, I don’t think Google has any choice but to go in this direction if they have any hope of gaining ground on Apple and try to stave off an imminent threat from Microsoft via their Windows 8 cross-device Metro strategy.

One of the facts that is becoming very clear to the industry at large is that Apple’s lead in hardware, software and services is a mammoth one. They are selling over 5 million Macs per quarter. The iPhone continues to be a hot product and while Android has gained much ground in units shipped against the iPhone, Apple is taking as much as 74% of all the profit in this space. And the iPad holds well over 80% of the tablet market share and this will be the case through this year too. And many of my research colleagues predict that even in 2015, Apple will have at least 60% of the tablet market.

But the key to Apple’s success is no secret. They are where they are because they own the hardware, software and services and combined they give Apple a significant advantage over their competitors. And while that too is no secret, what is not understood well by the outside world is that they architect their devices around their services. The best example of this is with the iPod. While the hardware itself is the profit center for Apple, it was the music service that was the critical component that made the iPod take off. From a hardware perspective, they architected it around the music service, which means they designed the iPod software, user interface and hardware dials so that they were optimized to deliver a great portable music experience.

The same goes for the iPhone and the iPad. It is the services that drive the final UI and hardware designs and since Apple controls the entire eco-system, they can be assured that they deliver to their customers a unified and easy to use experience with their products.

Now consider the plight of the middleware software vendors like Google and Microsoft. What they bring to the party is a critical component of any final product via the OS. But both companies architect from the inside out, or only at the software level and then hand this off to their vendor partners who must now design their hardware around the software and hope the design can be optimized for the OS they have been handed. And from Google and Microsoft’s standpoint, they can only influence and hope so much that their hardware vendors will get it right.

Historically speaking, Microsoft has done the best job of creating strict technical guidelines that hardware vendors can follow, but Google’s approach to Android design is pretty much a moving target. Vendors have told me of all kinds of problems they have had getting strict hardware guidelines from Google for building Android devices.

Microsoft’s model worked for PC’s. But I don’t think this model will continue to work with this new world of mobile devices. What seems to be happening now is that in both the Windows and Android camps, controlling how the hardware vendors use these operating systems is much more difficult as hardware vendors strive to try and differentiate themselves in the market place. In many cases that mean’s hardware and software UI tweaks that go beyond what these companies give them in the way of an OS which then potentially delivers various forms of fragmentation.

At some point, not controlling the entire hardware, software and services delivers diminishing returns to both of them and sooner or later they will find that the old PC model of creating an OS and giving it to vendors to propagate will not work. In fact, I am seeing that understanding starting to become clear to both Google and Microsoft as they stare up at Apple running away with all of the profits. Apple’s model works. Using the old PC model will not work in this new world of mobile devices.

This is why we are seeing so much hardware activity at Google and I expect to see similar branded hardware strategies evolve at Microsoft very soon. While they can hope that their partners can utilize their software to create great hardware and services, at some point they have to realize that putting their trust in their vendor partners to deliver their vision is a crapshoot.

Indeed, they may only have a real chance to catch Apple if they take control of the hardware, software and services and the sooner they realize this, the sooner they can control their individual destiny’s.

One of the things my firm focuses on is spotting trends within the technology industry. As a part of our constant search for trends we employ a concept we call “live the future now.” What this means, is that we as trend analysts, ourselves being early adopters, attempt to look for and implement things into our own work, play, family, life, etc, that we believe consumers may use technology for in the future. We also hunt out and study other people or groups of people, mostly early adopters, who are also using technology today the way we believe the masses will in the future.

So this column is going to be more about the future than the present.

Because I live and breathe this industry I also acquire quite a lot of technological gadgets as a part of this process. For the past six month’s I have been utilizing in different capacities no less than five and upwards of eight tablets at any given time all throughout my house. Not all my tablets are running the same core OS as some are iPads, some run Android and one runs Web OS. This helps me evaluate the strengths and weaknesses of a range of tablet operating systems and device features. Regardless of the OS I basically keep a tablet in every room of my house, except the bathroom, at all times. In basically every room where we spend significant time you will find a tablet of some shape or form. Living with a tablet in every room of my house is a fascinating experience. It is also a very convenient experience.

In the future I believe having access to these “smart connected screens” in every room will be a staple of most consumers’ homes in the developed world. What this enables is a situation where consumers don’t need to carry their tablets with them from room to room. They simply move to each room and as necessary, at their convenience, pick up the closest tablet and begin using it.

In my own experience doing this, I found that quite often I simply wanted to look something up on the Internet. What I looked for was the most convenient screen to access the Internet with. My notebook is rarely near me on the couch or bed and my smart phone suffices but the screen is a little to small for the job most times. This is where tablets come in. They are more mobile than notebooks and sport bigger screens than smart phones. And when you have one in every room you don’t have to think about bringing your tablet with you or where you left it last. Having a tablet in every room ready to be picked up and utilized was not only extremely convenient it was also extremely useful.

Now in this reality we must recognize that we may potentially shift from tablets being mainly personal computing devices to perhaps more communal computing devices–at least in the home environment.

Shift from Personal to Communal Screens

With the role of the personal cloud, I can see a situation where you just pick up the most convenient tablet/screen to your proximity, in whatever room you happen to be, log in to your personal cloud, and instantly the tablet becomes “your tablet.” It would contain all your personal settings, preferences, access to media, etc.

In this environment what is personal is your cloud not the device itself. This is a different take on the concept of personal computing. This of course does not mean that we consumers will not own personal computing devices, like smart phones for example, but that there will also be screens we use in our daily lives that are not personal but more communal. The personal cloud we subscribe to is what turns any screen into our personal computing platform for the amount of time we choose to use that screen as such.

Google’s Chrome OS is very similar in concept to what I am outlaying. Any person who has a Google account and has invested in the Chrome OS, via a ChromeBook, could log into my or any ChromeBook and begin using the device as if it was their own. When this concept makes its way to tablets I believe it will enforce this idea of a screen agnostic tablet, in every room, future that I am outlining.

Now of course for this to happen the cost of tablets will have to come down. That is why I pointed out at the start of this column that I am talking more about the future than the present. However, what if someday we can sell a $99 or less tablet that runs a very light OS, with access to cloud services, and wi-fi? Another way this reality could happen is with a hardware-as-a-service model where as a part of a subscription, perhaps to your cable provider, the devices are provided for free.

The bottom line is that over the next five years the BOM cost of tablets will come down. If these devices rely more on the cloud than native software, some of the costs will move from the device to the service. Making the hardware more affordable as it relies more on a service to become “personal.”

It is with these types of “smart connected screens” that I believe we will see the explosion of devices into consumers homes. Prior to tablets we may have assumed that the dominant computing screen in consumers lives was going to be a notebook PC. In essence we would have said that there would be a notebook in every room, owned by every consumer. I think we are rapidly learning that, that future is going to be given to tablets.

Best Buy has been running a commercial for the past few weeks where they are positioning themselves as THE place to buy a mobile phone. The commercial was very well done.

The commercial included many who invented recognizable aspects of the mobile phone experience. People like Philippe Kahn who created the camera phone. Or Ray Kurzweil touting speech and voice technologies he created. Each person goes on to say what they created in relation to the mobile phone. Then it ends with some Best Buy blue shirts saying the following:

We created a better way to buy a smart phone. Any phone, any carrier, and all of their plans, with lots of unbiased advice.

It is the last few words that I find the most interesting–with lots of unbiased advice. This insinuates that cell phone retailers should be accused of selling phones with biased advice. Perhaps not just bias advice but sales kickbacks from handset vendors as well incentivizing sales people in carrier stores to push one device over another. Not every vendor does this but it does happen. It can lead to overly zealous sales folks pushing devices on consumers they don’t actually want. I have actually witnessed this in action.

Last summer I was in a certain carriers store activating an iPad for their data network. I overheard a sales conversation between a woman in the store and a sales rep. She had mentioned several times that she was interested in the iPhone. During the process of the conversation the sales person talked her out of the iPhone to go with another device. I listened to her explain what her main uses were and they were fairly simple. Talk, text, email, web, and the device she was sold was fully capable. The only observation I made was that she did not seem overly technical. I was leaving the store at the same time as she was and I gave her my business card and asked if she wouldn’t mind emailing me in 30 days if she hadn’t exchanged the device. She emailed me a week later saying she exchanged it for the iPhone.

This is what I am referring to when I speak of the complexities and challenges of selling devices as retail. This is why I expect that over the next several, or more, years that we will see more companies duplicate Apple’s retail strategy and start opening more of their own direct to consumer outlets. Tim articulates in his column today that he expects Amazon, an online only retailer, to start employing their own retail strategy–which would truly signal this fundamental shift.

All of this just goes to demonstrate how the carrier sales channel is fundamentally broken. Best Buy is looking to solve this problem by carrying every device on every network. To some degree I almost wonder if Best Buy’s approach won’t lead to more challenges for consumers as there are faced with an overload of information and options. This is known as the consumer paradox of choice, which I have written about before.

Best Buy’s approach, believe it or not, will make handset vendors lives even more difficult. At least when sold through the carriers channel, these OEMs compete with a limited number of devices. Carriers don’t generally pick up every device an OEM makes but rather picks certain ones to fill gaps in their lineup. Competing in the sea of sameness which is the Android landscape, and will someday be the Windows phone landscape as well, will be even more difficult in an environment where the sea of sameness is multiplied. This is exactly what will happen in Best Buy as they sell every device, from every network.

And lastly is it even possible to be a sales person in retail and not have bias? We will see how this turns out as hopefully our friends at NPD will be able to track specifically what happens with sales of mobile phones and tablets at Best Buy. I, for the time being, will remain skeptical and convinced that the OEMs are better with their own retail presence. I outline that logic in this column by pointing out how similar the personal electronics market is to the automobile market. I remain convinced that the way we buy products is going to be drastically different in the not too distant future.

I recently noticed something about my tablet usage that really intrigued me. Since using the iPad, it has become a constant companion to me and along with my iPhone and Droid, I carry it with me all of the time. Although my smartphones are quite important to me, I have always had a bit of a difficult time reading their small screens and as I get older, I have to admit that the size of the screens I use in my life are becoming an important part of my user profile. And while I would often buy apps on the smart phones for use on them, I very seldom used them for any real eCommerce purchases. For that I mostly deferred to my laptop.

But over the last six months, I began noticing that my preferred screen for buying things started shifting over to the iPad. This particular fact came into even sharper focus for me recently when I read a piece in Wired that pointed out that Amazon’s tablet might actually serve as a powerful vehicle for their overall large store.

In this same article, they recounted a Wired interview with Steve Jobs in 1997 where they asked him what opportunities he saw with the Web. Here is what he said:

Wired: What other opportunities are out there? Steve Jobs: Who do you think will be the main beneficiary of the web? Who wins the most? Wired: People who have something – Jobs: To sell! Wired: To share. Jobs: To sell! Wired: You mean publishing? Jobs: It’s more than publishing. It’s commerce. People are going to stop going to a lot of stores. And they’re going to buy stuff over the Web!

As you can see, even back then, Jobs saw that there would be a major shift in user buying habits and that the Web would become a serious vehicle for eCommerce. And over the last 13 years that has happened in a big way. eBay, Craigslist, Amazon, iTunes, etc have all driven eCommerce into the mainstream and they are now just a normal part of the way most of us buy things, especially things that we cannot find at our local mall. Of course, the irony of this quote from Jobs is that while iTunes has driven his eCommerce vision, he also created stores that have become one of the most successful retail chains in the world.

Now, if you look closely at peoples shopping habits these days, much of how they search for a product through search engines and review sites like PC Mag’s product reviews, and then buy them over the Web, should give you an understand that the Web has literally become the most powerful medium for commerce next to the grocery store. Sure, people will always go to the mall, but the mall and local stores will always have a limited supply of goods. But through the Web, you can buy just about anything. Although people will still use desktops and laptops for eCommerce, if my experience with the iPad is any guide, then the tablet, with its bigger screen then a smart phone and its full access to all Web eCommerce in this highly mobile for factor, could actually drive even more eCommerce purchases in the future. Another way to look at this is that the tablet is Amazon’s Brick and Mortar and a tablet is to Amazon what a physical store is to Wal-Mart.

If you think about Amazon’s business, it started with selling books online and then quickly became a place where consumers can buy just about anything and shop competitively from one single location. It just so happens however that this location is not physical; it resides fully within your browser. Amazon’s location is virtual.

To contrast, a company like Wal-Mart is evolving into the digital age with a strategy that includes their brick and mortar stores. To some degree Barnes and Noble is doing something similar but only in the realm of books. Amazon however has no intentions of creating a physical location where you walk in to experience their service. I believe however that Amazon is very interested in giving you a virtual physical storefront and it started with the Kindle.

Any retailer will tell you how important the overall retail experience is to their success. Some companies do retail poorly and others do retail extremely well. The Kindle for Amazon started completely around discovering, purchasing and reading books. The Kindle is the retail storefront to Amazon’s digital book library.

I believe that the evolution of the Kindle will follow Amazon’s business evolution. It started with books then included everything else. Which is why this next device that will most likely be a fully featured tablet will also come with Amazon’s complete shopping experience built in. This includes not just digital storefronts like books, music and movies but physical items as well. Since Amazon is one of, if not the largest digital storefront, it benefits them to get devices on the market where they control the entire shopping experience.

This is one of the reasons Amazon re-jiggered their iOS app strategy to stay away from Apple’s transaction model and fees. I don’t believe this move was just about avoiding management fees but that Amazon wanted to control the user experience with their storefront instead of Apple.

Reflecting on that point briefly, it becomes clear that Apple’s app store commerce model works for those for whom billing and storefronts are a problem but it does not work for those companies who have spent millions of dollars perfecting their own e-commerce experience. This leads me to believe that if the entire eCommerce experience is baked into the tablet experience then Apple’s new big purchase might be an eCommerce “etailer” that offers a broad range of products that Apple can integrate into the complete user experience of the iPad.

Amazon also has an interesting strategy with their Prime service that could be strategically integrated as well within their tablet offering. Perhaps Amazon gives better deals or promotions to those who own the tablet and are Prime customers thus incentivizing more purchasing from their store directly on the tablet.

This is why I believe a tablet is actually strategic for Amazon. Of course they can and will make sure their services are available on every device imaginable. However if they bring a device to market that is a full blown tablet and also includes the most elegant and seamless experience to research, discover and purchase from, then that device becomes the retail storefront to everything Amazon sells – and more.

Our firm has been doing an extensive amount of tablet analysis over the past year. The more I study the role of the tablet in the industry and in the lives of consumers the more fascinated I become with this form factor. To clarify, we believe and classify the tablet as a PC. We simply view it as a form factor within the PC landscape.

One theme of late that has some of my mind share is around tablets going where traditional PCs can not. I am not just speaking of overall market share, although that factors into my thinking, but rather I am thinking about location. Now to be clear, I am not saying PCs (clamshell notebook PCs specifically) literally can not go to the locations I will talk about. Rather, what I want to point out is that the traditional PC/Notebook PC is the wrong form factor for a growing number of use cases and market pain points.

Prior to tablets, I believe the technology industry at large looked at nearly every consumer use case, as well as every vertical market, as an opportunity for the sale of a traditional PC/Notebook PC. What this led to was the adoption of the traditional PC into scenarios, where although sufficient, was the wrong form factor for the job. If you follow much of what I write you will notice that I am fond of Clayton Christensen’s philosophy in The Innovators Dilemma that consumers “hire” products to get jobs done. Prior to tablets the market “hired” the PC to do jobs that we are now finding tablets are better suited to do.

Last week I looked at the adoption of the iPad by a growing number of enterprises for specific mobile workforces like field force and sales force automation. In many business related scenarios we are seeing the iPad step in and take the place of notebook PCs primarily because it is better suited for the specific task at hand. Enterprises are finding that for their most mobile workers the iPad is a better tool for the job than a clamshell notebook.

Late last year I wrote in my TabTimes column about how small businesses are using iPads for things like point of sale retail and even mounting an iPad for interactive product/ media placement. I even talked about some examples where restaurant owners were going digital and integrating iPads for the uses of taking orders, showing pictures of menu items to customers, and adding other relevant information for customers to make dining decisions. In both those later use cases the job could have never been solved by a traditional clamshell PC because who wants to hang that device to the wall at retail or walk around a restaurant holding a clamshell notebook? This is at its core what I mean when I say that tablets will go where PCs can not. This is what I mean when I say that the tablet is the ultimate mobile PC.

Further to this point, I highlighted yesterday in an article how the iPad makes the perfect learning companion. I have been very vocal about how touch computing removes barriers to computing presented by mouse and keyboards and therefore are better tools for learning for all ages but kids specifically. We have been using PCs in the classroom because they were the only tools available. Now there is a better tool, the iPad, and it will find itself fitting into educational environments better than the PC ever could.

The list goes on from legal firms, to financial management firms, to hospitals and doctors, pilots and airlines, public safety, and more, who are all finding that the iPad is better suited than a clamshell PC for their specific computing needs. Consumers are waking up to this reality as well.

Although, the notebook PC is portable you don’t typically see consumers move around, walk around, or stand up and use their notebook. This is because the form factor lends itself to a desk or a lap where the screen sits at arm’s length away. Tablets are very different. Consumers are comfortable using them while standing, walking, sitting on the couch, laying in bed, in the bathroom, by the pool, at the beach, in the kitchen, etc. The tablet is not designed to be viewed at arm’s length and because of that our relationship with this form factor changes. We can use it in different ways and more importantly take it places we would not or could not take our clamshell PCs.

I would argue the tablet form factor lends itself to more mobile computing use cases than a clamshell notebook. Because when consumers use a clamshell notebook they are not truly mobile–they are stationary. Whereas one can actually use a tablet and truly be mobile. I know I am tweaking slightly the classically held definition of mobile computing. However, due to the nature of tablets impact on the market I believe the traditionally held definition of mobile computing needs to be challenged.

The PC, tablet, smart phone, and perhaps something new down the line, are all tools to get jobs done. Each one has its place and each will remain relevant in some way shape or form. However, when it comes to mobility the tablet is mobile computing in its purest form.

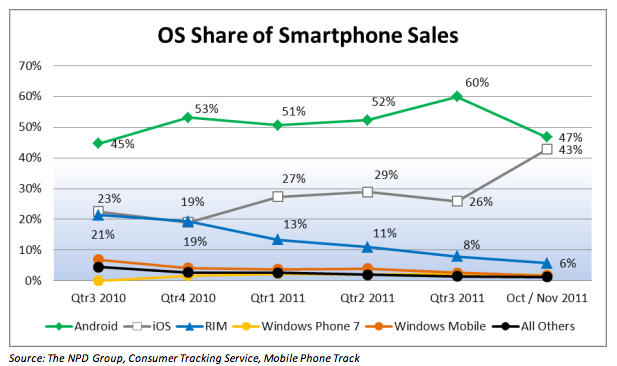

The end of 2011 brought about some interesting market developments. Both Nielsen and NPD shared data that the once so dominant Android actually declined in market share over the holiday quarter of 2011. Both Nielsen and NPD also shared that during the same quarter iOS, mostly due to the iPhone, closed the gap on overall Android market share.

Now, with all of these quarterly market share reports, we have to keep in mind that this data only reflects the current quarters data and not the annual or overall installed base. Still, it is important to note that during the holiday quarter (perhaps the most important quarter) Android market share declined and iOS jumped dramatically. This reality should concern Android partners and Google.

We sensed this trend early on and shared with our clients last fall the fact that Android could be headed for a decline in market share. In my TIME column in October of last year I outlined many of the ways that Google was mis-handling Android and unfortunately further straining their already strained relationship with their partners. If Google does not get a handle on not only the fragmentation issues but also their relationship with their partners (by being more transparent and trusting with them) then I anticipate the decline in Android market share to continue. Not solely based on more consumers choosing iOS but by Android’s partners vesting more resources and upping their commitment to Windows Phone.

I don’t expect any Android vendors to completely dump Android but I could see them shipping fewer Android devices overall as a part of their product mix in favor of Windows Phone, which inevitably would lead to fewer Android devices on shelves at any given time, which would lead to even further Android market share decline. I firmly believe that Android device volume is its strongest competitive advantage. Right now Android currently has the bigger share of OEM resources and overall device mix per OEM. However, that could all change very quickly and in 2013 Microsoft will have a compelling story around Windows Phone and Windows 8 for their partners. If Google does not adjust their strategy with Android quickly they run the risk of OEMs shifting the balance of their resources more toward Windows Phone (or something else) and away from the Android platform.

If you line up all of these underlying trends it could spell real trouble for Android. My biggest concern for Android overall is that the platform itself creates no significant hardware loyalty. That is a dangerous truth for any of Google’s hardware partners. The same can be said of Windows Phone, or any other horizontal platform for that matter. If you are going to be in the hardware game you have to differentiate and more importantly create a partner ecosystem that creates customer stickiness.

Lastly, on my point that Android’s competitive advantage is volume of devices in channel at any given time. NPD shared their data on the top devices sold over the Oct/Nov time period. If you look at the chart you see that the top three are iOS devices. Note these are three different phones. If Apple does continue to diversify their products on the market and leave legacy devices in channel at lower price points, they will themselves be creating their own iPhone army of devices that could further hurt Android’s market share over the long haul.

There used to be a time when I would go to tech industry events, trade shows, internal company meetings, etc. and I was one of the few in the room with a Mac. I took great pride in that fact, but now the Mac is gaining everywhere. It’s in schools, hospitals, labs, construction sites, restaurants, consumers’ homes, coffee shops, and now increasingly in the enterprise.

With this observation in mind it should come as no shock that Apple blew the doors off their latest earnings and recorded all time sales of Macs. My analyst colleague, Frank Gillet at Forester, shared his research which showed that 1 in 5 Global workers now use an Apple product for work.

So what is fueling this trend?

Apple Products Cost Less to Support

When I worked at Cypress Semiconductor, I moon-lighted from time to time and helped our IT department by solving Windows problems. I prided myself on the fact that I could troubleshoot Windows with the best of them. I could navigate my way in and out of all of the different and common Windows conflicts. Then a funny thing happened. I switched to the Mac and all of a sudden troubleshooting became a thing of the past. That reality is now hitting the enterprise IT departments.

A recent survey by the Enterprise Device Alliance which surveyed IT professionals in large enterprise environments that have a mix of Macs and PCs overwhelmingly found agreement with IT managers that Macs cost less than PCs to support. IT managers noted that Macs presented higher up front acquisition costs, but also noted that the long-term benefits were worth the tradeoff.

When it came to Mac adoption in the enterprise, ease of technical support and lower total cost of ownership were among the top reasons for the switch. Number one on their list–employee preference.

Bring Your Own Device To Work

If you follow this industry even a little bit you keep hearing about the “consumer-ization of IT” or the “Bring Your Own Device” trend. Yes, both trends are real and IT managers are diligently working to allow employees to use whatever devices they want at work.

We recently interviewed SAP’s CIO Oliver Bussman. He shared with us that inside SAP they have 14,000 iPads and 8,000 iPhones deployed. That is a total of 22,000 iOS devices compared to the 20,000 Blackberries deployed to his workers. SAP, like many other companies is working to cater to their employees’ device preference. And Mr Bussman shared an interesting perspective with us. He said that he now has to pay closer attention to what is going on in the consumer market because if he doesn’t, he would not be able to stay ahead of the game. His workers use and learn how to make things like the iPad work for them at home. Then they come to him and say they want to use it in the office as well. After his visit to CES, Mr. Bussman recorded a video of his thoughts on the consumer-ization of IT and it is worth watching as he has a very important perspective on the subject.

The Right Product for the Right Job

In the construction industry they say that “every job is easier with the right tools.” Perhaps for too long, due to the Windows monopoly on most businesses, IT managers have been forced to have workers use the same tool to get a multitude of jobs done. But now devices like the iPhone and iPad in particular are proving more effective in many situations like field force and sales force automation.

During our interview Oliver Bussman also shared with us that he was able to deploy 300 iPads to his global sales team in just 4 weeks. In many enterprise solutions, the iPad, and touch computing in general, is just a better tool for the job.

IT managers need to effectively empower their workforce to be productive and equipped with the tools they need to be successful. Apple products are now becoming a critical part of the enterprise tool set.

Apple’s focus has not been the corporate IT accounts. Apple has always been a consumer product company waiting for a pure consumer market to mature. Now that the consumer market for personal electronics has matured, it appears to also be an enterprise strategy. Demand for Apple products is at an all-time high with consumers and their latest earnings prove this. What no one really could have predicted was that to win in enterprise you had to also win in consumer. It seems logical, but hindsight is 20/20. That reality is now fueling growth in Apple’s favor from every corner of the technology sector. The scary thing for Apple competitors is that they are just getting started.

The answer to this is no, and yes. Let me explain.