It looked like Apple and the banks on one side and retailers on the other were headed for a war over phone payments. But now, Samsung seems ready to make it a three-sided fight. An article by Jason Del Ray on Re/code reports Samsung is negotiating with Massachusetts-based LoopPay over adding a third method for mobile payment to its product line.

Assuming Samsung jumps in, and the company is so far not commenting, it adds new complexity to the fight (Insiders). Apple Pay has the advantage of being the most sophisticated emerging standard with broad support of banks and credit card companies who are already advertising its availability. But it requires hardware accessible only in the iPhone 6/Plus, and Apple has shown no indication of any plan to make it available for use on non-Apple phones. CurrentC, the product of Merchant Customer Exchange (MCX), a consortium of big retailers, will work on a variety of iPhone and Android phones. While Apple Pay (and the related Google Wallet) uses Near Field Communication (NFC) to send encrypted data from the phone to the retailer, CurrentC uses a QR matrix on the screen of the phone to be read and interpreted by the retailer.

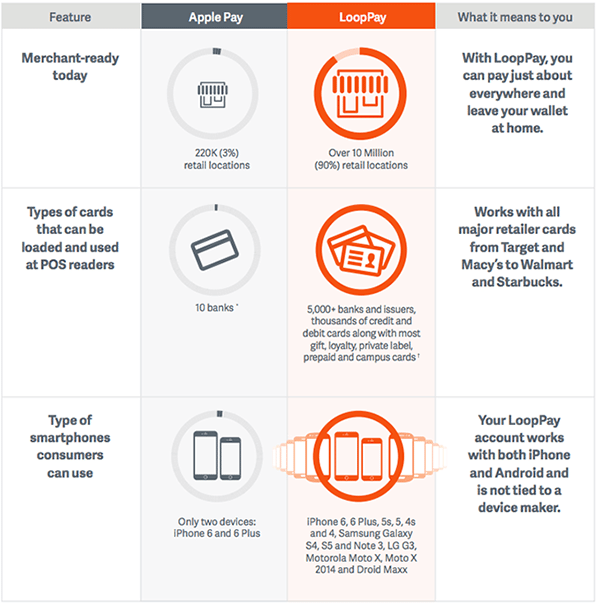

LoopPay (video demonstration) generates a data signal through a technology it calls a Magnetic Secure Transmission. The data can be read by existing retail devices that believe a card was just swiped. There are two big drawbacks. One is it requires the use of one of several devices that include a LoopPay CardCase, which serves as an iPhone case, and a LoopPay Case, a free-standing device that can be used with no phone attached. Both of these devices has a built-in system that can be set up for retail use by swiping a card once. Presumably, an adoption by Samsung would result in the LoopPay function being built into phones. The second disadvantage is it is designed to need standard swipe-able credit cards at time of purchase. Apple Pay and CurrentC may disagree on just about everything else, but they agree on the desirability of eliminating traditional credit cards as quickly as possible.

LoopPay is trying hard to argue its choices represent the strongest option. In a public note, LoopPay CEO Will Graylin argues the company’s approach, described as David v. Goliath, is superior to Apple Pay, Google Wallet, and the largely abandoned Software (CurrentC is not discussed). He claims LoopPay provides equal security to Apple Pay and LoopPay allows consumers to stop worrying about credit cards. “One less thing to carry is one less thing to worry about or lose,” Graylin writes. “They want to use the cards they already have, at their favorite merchants, on the devices they own. Their wallet account is personal. It should belong to them, and not be tied to any one device or just a few select banks.”

It looks like Samsung would face a serious hurdle with LoopPay in challenging both Apple Pay and CurrentC. Apple and its supporters are moving aggressively to take advantage of the solo control of credit card transactions. The other night, I saw back to back TV ads from CitiBank and BankAmerica supporting Apple Pay. MCX supporters Target and Walmart are likely to advertise CurrentC when it becomes available on phones next year.

It looks like Samsung would face a serious hurdle with LoopPay in challenging both Apple Pay and CurrentC. Apple and its supporters are moving aggressively to take advantage of the solo control of credit card transactions. The other night, I saw back to back TV ads from CitiBank and BankAmerica supporting Apple Pay. MCX supporters Target and Walmart are likely to advertise CurrentC when it becomes available on phones next year.

Unlike the Apple-bank alliance and CurrentC, Samsung’s use of LoopPay, assuming they could get phones supporting it into the markets quickly, is going to find it tough to fight with one force already working hard and another that will enter the market soon with a big pitch. But Samsung has been active in trying to add consumer services beyond making phones and its complex relationship with Google may account for its lack of interest in promoting Google Wallet. They would be getting into the fight very late, but Samsung could make the battle more interesting.