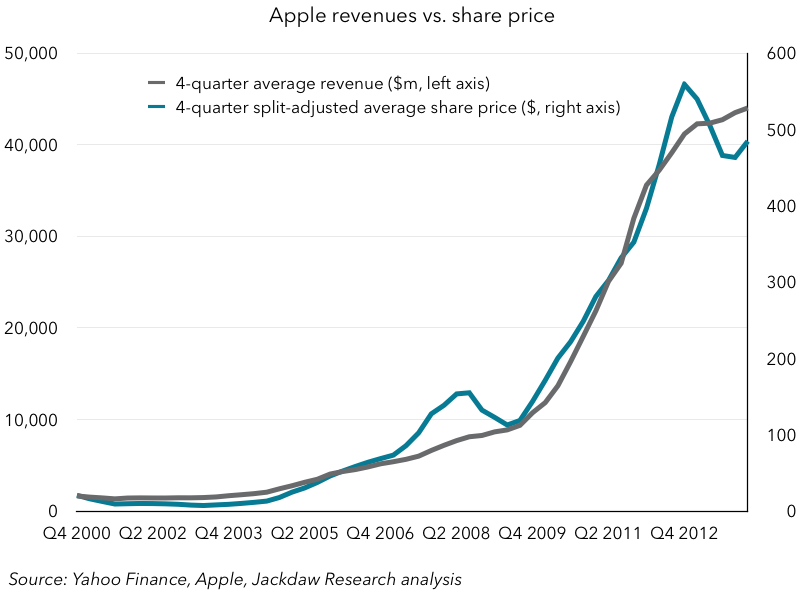

Apple has been a phenomenally successful company over the past 15 years, releasing three new product lines which revolutionized the markets they entered and drove enormous growth and profits for the company. Shareholders have benefited enormously too, as revenues and share price have risen largely in tandem over that period:

During the period from 2000-2012, Apple pleased two constituencies equally well: shareholders and customers. Producing compelling products pleased the customers who bought them in huge numbers and the growth those customers drove pleased shareholders too. Especially as Apple introduced the iPhone, growth exploded, profits increased even faster, and shareholders made out like bandits.

But over the last two years we’ve seen a de-coupling of the previously closely aligned interests of customers and shareholders. As Apple’s biggest product line, the iPhone, has reached maturity and high penetration among its target customer base, growth has slowed. With the groundwork laid by the iPhone, the iPad has rocketed to high penetration rates much more quickly, leading to enormous early growth and a much more rapid slowing of growth than the iPhone. As a result, overall growth in both revenues and profits at Apple has slowed, even though both revenues and operating profits remain significantly higher than those at the other three big consumer tech companies – Microsoft, Google and Amazon.

At the same time, consumers remain very happy with Apple’s products, buying tens of millions of iPhones and iPads and millions of Macs and iPods each year. Customer satisfaction and loyalty rates remain very high. Apple achieves this in part by taking its time with product development, releasing products in new categories only when they can deliver them well, and often withholding what others would consider key features until they can be delivered right or perhaps never. Consider the original iPhone. No 3G, Flash support, multitasking or copy/paste. All but Flash were eventually added, but only when Apple felt adding them didn’t require too much compromise. Of course, Flash famously never was. Or consider the iPad, the concept for which Apple developed before the iPhone but postponed until three years later because it felt the underlying technology wasn’t ready. Though observers have criticized Apple for making these moves, customers don’t seem to have minded and so investors have still been happy.

Apple has therefore always been, to an unusual degree, a company motivated first and foremost by creating great products rather than driving shareholder returns. But it’s also understood the former should generally also produce the latter, even though the reverse is seldom true. But as growth has slowed, and the stock price has followed, Apple is faced with a critical decision: whether to start doing things that will make sense financially in the short term even if they’re not what’s best for its customers and for Apple’s long term success. So far, Apple has dealt with this situation exclusively through financial mechanics, with stock buy-backs, dividends and now a stock split. These actions have boosted the share price even in the absence of massive growth, major new product categories or other drivers in the core business. But unless it keeps increasing the size of buybacks and dividends, there’s only so much Apple can do to appease shareholders hungry for the kind of exceptional growth the iPhone drove.

The temptation at this point will be to start to erode the overarching commitment to great products in the interests of driving short term growth. For example, to put a wearable device out into the market at a time when those on offer are all fundamentally flawed, pointing to limitations in the underlying technology. Or to introduce a cheaper iPhone for emerging markets because that’s where all the growth is. To be clear, neither of these moves – introducing a wearable or a cheaper device for emerging markets – would be a strategic mistake by itself. But the temptation in both cases would be to produce a sub-par product in these categories out of a sense of urgency driven by shareholders not customers.

I see no indication this kind of shift in thinking is imminent. Tim Cook has shown a willingness to stand up to shareholders such as Carl Icahn and the NCPPR, which suggests he’s not going to be a pushover on this front. But I think much of the response to the reports Apple might acquire Beats seem to stem from a sense Apple might be about to succumb to that temptation, by buying growth at the expense of selling an inferior product. They are just reports at this point and we don’t know whether the deal will be done, let alone whether Beats headphones will be sold as Apple products. But I think it’s that fear that has so many people worried about what a Beats deal might signify.

The reality, of course, is if Apple did release an inferior product, or worse still several of them, it would be an enormous strategic blunder. Apple products command such a premium precisely because their standards are so high, and any lowering of standards due to short term financial expediency would be terrifically damaging long term. The fact is the tension here isn’t actually so much between Apple’s customers and its shareholders as a whole – it’s between those interested in Apple’s long term prospects and those interested in short term financial performance.

Apple’s challenge over the coming months is to demonstrate what it’s doing to secure the long term performance of the company. That will start with WWDC in a couple of weeks and continue with the new product categories launched there and/or later in the year. If Apple gets it right, the interests of shareholders and consumers should be brought back into balance, resolving the tension. If it doesn’t, the tension will just continue to increase and with it, the temptation to do something Apple shouldn’t.

Apple has plenty of cash to pay off the blood suckers on wallystreet, with buy backs, etc. Apple knows; Wall Street blows.

I think you overstate the case a bit. I do believe Tim Cook has the strength to hold off Wall Street and resist caving to the temptations I describe above. However, he’s not immune to them either – look at all the moves in the last few years – share buybacks, dividends and now the stock split. He’s clearly not above catering to their needs, caving to some of their demands, but so far he’s done it exclusively through financial mechanics rather than through products. The question is, does the tension increase or decrease over the next year?

The worst article from techpinions I ever read.

Why do you say that?

Would be interested to hear why you say that. Could you explain?

My humble apologies.

When I made that comment I was skimming though your article and when I read it in depth I was wrong, once again my apologies.

I appreciate that. Thank you.

Apple buying Beats remains speculative and if it is done the reason will be more than the simplicity minded ideas running in blog dorm.

It is hard to believe Apple will depart from product and customer focus without major board and leadership changes neither of which seem likely.

It is dangerous to assume causality with correlation. I take Apple at its word that it has been working the what to do with cash much longer than the recent downturn. Although following Buffet’s strategy that when the market is idiotic and way undervalues the stock, buy the stock. As long as market keeps treating Apple as low PE 10-12 with mind boggling margins and profits and pretty good growth for a huge company, then buy the stock.

When Apple makes it’s next big move it will define a market like Google Glass or SAMSUNG wearables, etc have not. Remember Netbooks,

Blog dorm. I like it. Or was it blogdom?

This is truly a feeble article. You are merely rehashing known knowns. Ahem! Waste of time and space. Brian S Hall, where are you? Deliver us from such mediocrity!

You’re absolutely right, but you’ve just gotten the tip of the iceberg.

Any successful company begins by adding value to society, and as it grows it reaches a point where this added value is fully incorporated. The market demands perpetual growth, however, and companies are then forced to use their power – their brand, their influence, their marketing, their pricing – to begin not just to add value, but to extract value. You can envision an adoption curve similar to the ones Horace Didieu occasionally shows for product adoption: while in the steep, fat part of the adoption curve, value is being added, as more and more people benefit from their interaction with the company’s products/services. As the curve begins to level off, the growth in adoption/interaction slows, but market forces demand that growth in revenue and profit continues, and consequently greater profits must be generated from non-greater value: hence, value creation is followed by value extraction.

Apple is interesting, but not unique, in that it has a very strong value-addition focus: that is, it is focused on customer experience. When it does reach the point at which its ability to add value fully saturates society, it will be interesting, and possibly depressing, to watch, because it is hard to envision any corporate governance successfully ignoring the incessant, in-your-face demands of the market.

The companies we “hate” are generally the companies that have long-since gone beyond the major value-addition phase of their corporate lifespans and are deep in the value-extraction phase: cable companies, cellular providers, airlines, perhaps Microsoft. Some companies – Google and Facebook, for example – we see transitioning more and more to value extraction, as their main products have become ubiquitous and the need for growth is beginning to lead to questionable, from customer perspective, changes in the way they make money.

Apple is not there yet, and so far has refused to engage in reputation-damaging value-extraction practices. Constant, creeping price increases combined with slow reductions in quality, value and service; increased use of customer data for questionable purposes; new charges for previously-free services; and entry into increasingly less value-appropriate markets will be signs of this happening.

There will come a day when it will be very difficult, almost impossible, for Apple to resist a movement towards value-extraction. I hope we’re not there yet, and it will be interesting to see what happens. Hope, though, that the tension between Apple’s customers and its shareholders goes up when that day approaches, because if it doesn’t, it will be because the market has won, as it almost always does.

Written as (for now) both customer and shareholder.

Please let me know if you’re looking for a article author for your weblog. You have some really good posts and I think I would be a good asset. If you ever want to take some of the load off, I’d really like to write some articles for your blog in exchange for a link back to mine. Please send me an email if interested. Regards!

Right now it seems like Drupal is the top blogging platform out there right now. (from what I’ve read) Is that what you’re using on your blog?

If you have looked at retail sportsbooks and on-line sportsbooks, you may perhaps have observed a completeslew of odds.

I do not even understand how I ended up here, but I assumed this publish used to be great

delta 5/8 table saw nut

There is definately a lot to find out about this subject. I like all the points you made

May I have your authorization to add this content to my dataset? It’s important for me to mention that I’m collecting this data for my personal hobby as a data scientist, and citing the source is a standard practice. Here my campus page at Kampus Terbaik Thanks! ID : CMT-1J31H59PTAIA3GD0SL

clomid tablet buying generic clomid price – get cheap clomid without rx

https://amoxil.icu/# amoxicillin 500mg without prescription

http://ciprofloxacin.life/# ciprofloxacin mail online

http://amoxil.icu/# amoxicillin 500 mg

where buy generic clomid without rx: cost of cheap clomid pills – order cheap clomid without prescription

prednisone tablets india: order prednisone on line – where to get prednisone

https://nolvadex.fun/# low dose tamoxifen

nolvadex only pct: tamoxifen and grapefruit – nolvadex pct

http://zithromaxbestprice.icu/# can you buy zithromax over the counter in mexico

https://nolvadex.fun/# tamoxifen and grapefruit

tamoxifen lawsuit: tamoxifen blood clots – tamoxifen and ovarian cancer

http://lisinoprilbestprice.store/# lisinopril 10mg

where to buy lisinopril without prescription: zestril 30 mg – lisinopril 10 mg tablets price

http://nolvadex.fun/# tamoxifen vs raloxifene

http://lisinoprilbestprice.store/# lisinopril 30 mg cost

how to buy zithromax online: buy zithromax 500mg online – buy zithromax 500mg online

cytotec buy online usa: п»їcytotec pills online – buy misoprostol over the counter

https://lisinoprilbestprice.store/# lisinopril price comparison

nolvadex for sale: tamoxifen benefits – should i take tamoxifen

https://lisinoprilbestprice.store/# prinivil generic

how to buy doxycycline online: doxycycline pills – doxycycline order online

http://lisinoprilbestprice.store/# lisinopril 20 mg coupon

doxycycline vibramycin: buy doxycycline online – buy doxycycline cheap

https://lisinoprilbestprice.store/# cost of lisinopril 40mg

https://mexicopharm.com/# mexican rx online mexicopharm.com

mexican online pharmacies prescription drugs: Purple Pharmacy online ordering – п»їbest mexican online pharmacies mexicopharm.com

reputable mexican pharmacies online: Mexico pharmacy online – medicine in mexico pharmacies mexicopharm.com

http://mexicopharm.com/# mexico pharmacies prescription drugs mexicopharm.com

reputable indian pharmacies: Online India pharmacy – buy medicines online in india indiapharm.llc

mexican pharmacy: Best pharmacy in Mexico – buying prescription drugs in mexico online mexicopharm.com

https://canadapharm.life/# online canadian drugstore canadapharm.life

world pharmacy india: Medicines from India to USA online – online shopping pharmacy india indiapharm.llc

reputable mexican pharmacies online: Medicines Mexico – best online pharmacies in mexico mexicopharm.com

http://canadapharm.life/# canadian pharmacy 24 canadapharm.life

reputable mexican pharmacies online: mexican pharmacy – buying from online mexican pharmacy mexicopharm.com

https://canadapharm.life/# medication canadian pharmacy canadapharm.life

buying from online mexican pharmacy: Mexico pharmacy online – mexico pharmacies prescription drugs mexicopharm.com

reputable indian online pharmacy: Medicines from India to USA online – reputable indian online pharmacy indiapharm.llc

mexican pharmaceuticals online: Best pharmacy in Mexico – mexico pharmacies prescription drugs mexicopharm.com

https://indiapharm.llc/# india pharmacy indiapharm.llc

my canadian pharmacy: Canada pharmacy online – canadian pharmacy tampa canadapharm.life

canadian pharmacy 1 internet online drugstore: Canadian pharmacy best prices – canada drugs online reviews canadapharm.life

buying prescription drugs in mexico: Medicines Mexico – mexican border pharmacies shipping to usa mexicopharm.com

https://mexicopharm.com/# mexico pharmacies prescription drugs mexicopharm.com

https://kamagradelivery.pro/# buy Kamagra

п»їLevitra price: Buy Vardenafil 20mg – Levitra 20 mg for sale

http://levitradelivery.pro/# Cheap Levitra online

sildenafil 50 mg online india: Buy generic 100mg Sildenafil online – sildenafil pharmacy

http://levitradelivery.pro/# Levitra 10 mg buy online

buy tadalafil 5mg online: Tadalafil 20mg price in Canada – tadalafil online 10mg

http://levitradelivery.pro/# Levitra price

Buy generic Levitra online: Buy Levitra 20mg online – Cheap Levitra online

https://sildenafildelivery.pro/# 100mg sildenafil prices

Levitra online pharmacy: Buy Levitra 20mg online – Levitra generic best price

http://tadalafildelivery.pro/# tadalafil tablets 20 mg india

Levitra 10 mg buy online: Levitra best price – Levitra generic best price

http://levitradelivery.pro/# Vardenafil buy online

buy Kamagra: cheap kamagra – super kamagra

https://sildenafildelivery.pro/# sildenafil price comparison

buy sildenafil 25 mg: sildenafil without a doctor prescription Canada – cheapest sildenafil tablets

paxlovid for sale: buy paxlovid online – buy paxlovid online

http://clomid.auction/# order generic clomid pill

http://prednisone.auction/# prednisone cream over the counter

buy amoxicillin: Amoxicillin 500mg buy online – amoxacillian without a percription

https://clomid.auction/# buy clomid tablets

http://clomid.auction/# can you get generic clomid without insurance

п»їpaxlovid Buy Paxlovid privately paxlovid buy

https://prednisone.auction/# prednisone for sale online

minocycline 100mg pills online: buy ivermectin online – minocycline 100 mg tablet

http://prednisone.auction/# purchase prednisone

https://clomid.auction/# where to get generic clomid without prescription

http://paxlovid.guru/# paxlovid buy

can you buy amoxicillin over the counter in canada: buy amoxil online – buy amoxicillin 500mg uk

https://furosemide.pro/# lasix 40 mg

lisinopril 10 best price: buy lisinopril online – lisinopril 20mg tablets

buy zithromax: cheapest azithromycin – how to get zithromax

https://furosemide.pro/# lasix pills

generic propecia no prescription buy propecia cost generic propecia

buy zithromax 1000 mg online: zithromax best price – zithromax 500 mg for sale

http://azithromycin.store/# where to buy zithromax in canada

lasix for sale: furosemide 40 mg – lasix uses

https://azithromycin.store/# zithromax 500mg over the counter

buy misoprostol over the counter: Misoprostol best price in pharmacy – buy misoprostol over the counter

can you buy zithromax over the counter in australia buy zithromax z-pak online zithromax 500mg

https://finasteride.men/# order generic propecia without prescription

cost generic propecia tablets: cost of propecia without rx – order propecia without rx

how to get zithromax: zithromax best price – zithromax z-pak

http://lisinopril.fun/# generic for prinivil

cost generic propecia pills Finasteride buy online cheap propecia without insurance

Abortion pills online: Buy Abortion Pills Online – Cytotec 200mcg price

https://finasteride.men/# generic propecia online

zithromax buy: where can you buy zithromax – zithromax generic cost

http://azithromycin.store/# zithromax order online uk

zestril medication: High Blood Pressure – lisinopril 20 mg brand name

buy lasix online Over The Counter Lasix generic lasix

lisinopril online pharmacy: lisinopril medication generic – where can i get lisinopril

http://lisinopril.fun/# medication lisinopril 10 mg

buy propecia pills: Buy Finasteride 5mg – order generic propecia without dr prescription

http://lisinopril.fun/# zestril

buy furosemide online lasix dosage lasix for sale

order cytotec online: order cytotec online – buy cytotec online

how to buy zithromax online: buy zithromax over the counter – zithromax for sale usa

http://misoprostol.shop/# buy cytotec pills

farmacia online piГ№ conveniente: farmacia online miglior prezzo – farmacie online affidabili

https://sildenafilitalia.men/# viagra naturale in farmacia senza ricetta

acquistare farmaci senza ricetta kamagra oral jelly migliori farmacie online 2023

comprare farmaci online con ricetta: comprare farmaci online con ricetta – migliori farmacie online 2023

http://kamagraitalia.shop/# migliori farmacie online 2023

farmacie online affidabili: farmacia online spedizione gratuita – acquistare farmaci senza ricetta

http://sildenafilitalia.men/# viagra online spedizione gratuita

п»їfarmacia online migliore: kamagra gel – comprare farmaci online all’estero

farmacia online senza ricetta Tadalafil generico acquisto farmaci con ricetta

http://kamagraitalia.shop/# farmacie online sicure

farmacie on line spedizione gratuita: kamagra oral jelly – migliori farmacie online 2023

farmaci senza ricetta elenco: Cialis senza ricetta – farmacie on line spedizione gratuita

https://farmaciaitalia.store/# comprare farmaci online con ricetta

http://avanafilitalia.online/# acquisto farmaci con ricetta

viagra 50 mg prezzo in farmacia viagra online spedizione gratuita viagra originale recensioni

alternativa al viagra senza ricetta in farmacia: viagra consegna in 24 ore pagamento alla consegna – cerco viagra a buon prezzo

http://avanafilitalia.online/# farmacia online migliore

cialis farmacia senza ricetta: viagra prezzo farmacia – farmacia senza ricetta recensioni

http://sildenafilitalia.men/# dove acquistare viagra in modo sicuro

viagra 100 mg prezzo in farmacia: viagra consegna in 24 ore pagamento alla consegna – cerco viagra a buon prezzo

https://tadalafilitalia.pro/# farmacie online sicure

viagra naturale viagra online siti sicuri viagra consegna in 24 ore pagamento alla consegna

http://farmaciaitalia.store/# farmacia online senza ricetta

http://indiapharm.life/# india online pharmacy

indian pharmacy paypal: top 10 pharmacies in india – indian pharmacy online

https://indiapharm.life/# best india pharmacy

buying prescription drugs in mexico: reputable mexican pharmacies online – reputable mexican pharmacies online

mexican border pharmacies shipping to usa: medication from mexico pharmacy – mexican border pharmacies shipping to usa

pharmacies in mexico that ship to usa mexico drug stores pharmacies п»їbest mexican online pharmacies

http://canadapharm.shop/# best canadian online pharmacy

mexican rx online: mexican border pharmacies shipping to usa – mexican pharmacy

https://canadapharm.shop/# global pharmacy canada

canadadrugpharmacy com: ed meds online canada – canadian online pharmacy

http://canadapharm.shop/# canadian pharmacy 365

adderall canadian pharmacy: global pharmacy canada – rate canadian pharmacies

mexican pharmaceuticals online: mexico drug stores pharmacies – mexican pharmacy

http://indiapharm.life/# indian pharmacy paypal

onlinecanadianpharmacy 24: canadian pharmacy – safe canadian pharmacies

https://indiapharm.life/# world pharmacy india

https://mexicanpharm.store/# pharmacies in mexico that ship to usa

Online medicine home delivery: Online medicine order – cheapest online pharmacy india

reputable mexican pharmacies online: buying from online mexican pharmacy – buying from online mexican pharmacy

https://mexicanpharm.store/# buying from online mexican pharmacy

online shopping pharmacy india: indian pharmacy online – top 10 online pharmacy in india

https://indiapharm.life/# indian pharmacy

canadapharmacyonline legit: canada drugs – buying from canadian pharmacies

https://mexicanpharm.store/# medicine in mexico pharmacies

is canadian pharmacy legit: canadian pharmacy review – canadian compounding pharmacy

https://canadapharm.shop/# canadian pharmacies comparison

canadian pharmacy online ship to usa: canadian pharmacy price checker – legit canadian pharmacy online

https://mexicanpharm.store/# mexican online pharmacies prescription drugs

mexican mail order pharmacies: mexican mail order pharmacies – mexican border pharmacies shipping to usa

http://mexicanpharm.store/# mexican rx online

https://prednisonepharm.store/# prednisone rx coupon

prednisone for dogs: buying prednisone mexico – prednisone 20 mg tablets

https://cytotec.directory/# buy cytotec pills

https://nolvadex.pro/# tamoxifen 20 mg

prednisone 20mg capsule: prednisone 5 mg tablet price – buy prednisone online australia

http://cytotec.directory/# cytotec buy online usa

best pharmacy prednisone: cost of prednisone tablets – 200 mg prednisone daily

https://zithromaxpharm.online/# zithromax generic cost

buy cytotec online fast delivery: buy cytotec over the counter – cytotec buy online usa

They simplify global healthcare https://zithromaxpharm.online/# zithromax purchase online

https://prednisonepharm.store/# buy prednisone canada

cytotec buy online usa Cytotec 200mcg price cytotec buy online usa

cost of prednisone tablets: prednisone 10mg tablet price – online order prednisone 10mg

https://prednisonepharm.store/# how much is prednisone 10 mg

does tamoxifen cause bone loss: tamoxifen bone pain – tamoxifenworld

They offer invaluable advice on health maintenance https://zithromaxpharm.online/# zithromax 1000 mg pills

http://prednisonepharm.store/# prednisone over the counter cost

tamoxifen cyp2d6: buy nolvadex online – is nolvadex legal

https://zithromaxpharm.online/# zithromax 500 mg for sale

buy cytotec over the counter Cytotec 200mcg price purchase cytotec

http://edwithoutdoctorprescription.store/# buy prescription drugs from canada

what is the best ed pill: best ed pills online – ed medication online

https://reputablepharmacies.online/# canadian pharmacy price checker

cheap erectile dysfunction pills: best male ed pills – treatments for ed

buy prescription drugs: buy prescription drugs from canada – how to get prescription drugs without doctor

https://edpills.bid/# cheap erectile dysfunction pills online

viagra without doctor prescription amazon: buy prescription drugs from canada – best ed pills non prescription

http://edpills.bid/# ed pills for sale

ed remedies: best ed pills at gnc – natural remedies for ed

https://edpills.bid/# erectile dysfunction drug

non prescription ed pills: online prescription for ed meds – non prescription ed pills

prescription drugs without doctor approval: generic viagra without a doctor prescription – ed meds online without doctor prescription

canadian drug prices: canada prescriptions online – legit canadian pharmacy

https://edwithoutdoctorprescription.store/# buy prescription drugs without doctor

canada pharmacy world superstore pharmacy online canadian pharmaceutical companies that ship to usa

https://edpills.bid/# buy erection pills

mail order prescription drugs from canada: canadian pharmacies top best – aarp recommended canadian pharmacies

http://edpills.bid/# best otc ed pills

treatment of ed: ed drugs compared – cheap ed drugs

new ed drugs cures for ed non prescription ed drugs

http://mexicanpharmacy.win/# reputable mexican pharmacies online mexicanpharmacy.win

medication from mexico pharmacy: pharmacies in mexico that ship to usa – mexican pharmacy mexicanpharmacy.win

http://indianpharmacy.shop/# Online medicine home delivery indianpharmacy.shop

http://indianpharmacy.shop/# mail order pharmacy india indianpharmacy.shop

medicine in mexico pharmacies: mexican pharmacy – mexico pharmacy mexicanpharmacy.win

http://mexicanpharmacy.win/# mexico pharmacy mexicanpharmacy.win

п»їlegitimate online pharmacies india: indian pharmacy – indian pharmacies safe indianpharmacy.shop

mexico pharmacy mexican pharmacy online mexico drug stores pharmacies mexicanpharmacy.win

https://canadianpharmacy.pro/# pharmacy wholesalers canada canadianpharmacy.pro

https://indianpharmacy.shop/# india pharmacy indianpharmacy.shop

http://indianpharmacy.shop/# reputable indian pharmacies

cheapest online pharmacy india

medicine in mexico pharmacies: Mexico pharmacy – mexican pharmaceuticals online

http://canadianpharmacy.pro/# canadian pharmacy ltd canadianpharmacy.pro

https://canadianpharmacy.pro/# canadian pharmacy india canadianpharmacy.pro

reputable indian pharmacies

https://indianpharmacy.shop/# indianpharmacy com indianpharmacy.shop

best online pharmacy india

http://canadianpharmacy.pro/# canadian pharmacy 24 canadianpharmacy.pro

indian pharmacy

https://canadianpharmacy.pro/# global pharmacy canada canadianpharmacy.pro

pharmacy website india

http://indianpharmacy.shop/# Online medicine home delivery indianpharmacy.shop

indian pharmacy

https://mexicanpharmacy.win/# mexico pharmacies prescription drugs mexicanpharmacy.win

legit canadian pharmacy

https://canadianpharmacy.pro/# safe canadian pharmacy canadianpharmacy.pro

http://canadianpharmacy.pro/# maple leaf pharmacy in canada canadianpharmacy.pro

online shopping pharmacy india

http://mexicanpharmacy.win/# medication from mexico pharmacy mexicanpharmacy.win

indian pharmacy online

mexico drug stores pharmacies: Medicines Mexico – mexico pharmacy mexicanpharmacy.win

Meilleur Viagra sans ordonnance 24h: viagra sans ordonnance – Meilleur Viagra sans ordonnance 24h

pharmacie ouverte 24/24: acheter kamagra site fiable – Pharmacies en ligne certifiГ©es

Acheter Sildenafil 100mg sans ordonnance: viagra sans ordonnance – Viagra gГ©nГ©rique sans ordonnance en pharmacie

https://viagrasansordonnance.pro/# Viagra homme sans ordonnance belgique

pharmacie ouverte

Pharmacie en ligne sans ordonnance: Levitra acheter – Pharmacie en ligne France

Pharmacie en ligne livraison rapide: kamagra gel – pharmacie ouverte

Pharmacie en ligne livraison gratuite: cialissansordonnance.shop – п»їpharmacie en ligne

acheter medicament a l etranger sans ordonnance: cialis generique – pharmacie ouverte

Viagra femme sans ordonnance 24h: Viagra sans ordonnance 24h – Viagra homme sans prescription

https://acheterkamagra.pro/# Pharmacies en ligne certifiГ©es

Pharmacie en ligne livraison rapide

Prix du Viagra 100mg en France Viagra generique en pharmacie Le gГ©nГ©rique de Viagra

Pharmacie en ligne France: Pharmacie en ligne livraison 24h – п»їpharmacie en ligne

Pharmacie en ligne livraison gratuite: cialis sans ordonnance – Pharmacie en ligne livraison 24h

п»їpharmacie en ligne: Pharmacie en ligne pas cher – Pharmacie en ligne fiable

where buy cheap clomid without prescription: rx clomid – how to get cheap clomid prices

https://amoxicillin.bid/# amoxicillin 500 mg

generic amoxil 500 mg: amoxicillin 500 mg where to buy – amoxicillin 500 mg brand name

buy zithromax online with mastercard: zithromax 500mg price – zithromax price south africa

how to get amoxicillin over the counter: amoxicillin 200 mg tablet – cost of amoxicillin prescription

http://prednisonetablets.shop/# prednisone 50mg cost

can you buy prednisone: prednisone online paypal – prednisone cream rx

amoxicillin where to get: amoxicillin 500 – amoxicillin 500 mg price

amoxicillin 50 mg tablets: amoxicillin 500mg without prescription – amoxicillin from canada

how can i get prednisone online without a prescription: where to buy prednisone 20mg – prednisone 15 mg tablet

http://clomiphene.icu/# can i order generic clomid without rx

stromectol ivermectin buy: buy oral ivermectin – ivermectin 3mg price

ivermectin tablets: ivermectin 3mg tablet – ivermectin 6mg tablet for lice

amoxicillin script: buy amoxicillin 500mg online – amoxicillin online canada

best canadian pharmacy: Canada Pharmacy online – canada rx pharmacy world canadianpharm.store

https://mexicanpharm.shop/# mexican mail order pharmacies mexicanpharm.shop

reputable indian pharmacies: international medicine delivery from india – pharmacy website india indianpharm.store

buy prescription drugs from india: Indian pharmacy to USA – Online medicine home delivery indianpharm.store

https://mexicanpharm.shop/# mexican rx online mexicanpharm.shop

Online medicine home delivery: international medicine delivery from india – india pharmacy indianpharm.store

online pharmacy india: international medicine delivery from india – indianpharmacy com indianpharm.store

https://canadianpharm.store/# pharmacy in canada canadianpharm.store

mexico pharmacy: Online Pharmacies in Mexico – п»їbest mexican online pharmacies mexicanpharm.shop

https://mexicanpharm.shop/# mexican border pharmacies shipping to usa mexicanpharm.shop

mexican border pharmacies shipping to usa: Online Pharmacies in Mexico – mexican drugstore online mexicanpharm.shop

https://indianpharm.store/# indian pharmacy online indianpharm.store

india pharmacy mail order: order medicine from india to usa – buy medicines online in india indianpharm.store

reputable mexican pharmacies online: Certified Pharmacy from Mexico – mexican online pharmacies prescription drugs mexicanpharm.shop

legit canadian pharmacy: Canadian Pharmacy – online canadian pharmacy canadianpharm.store

world pharmacy india: Indian pharmacy to USA – top 10 pharmacies in india indianpharm.store

top 10 pharmacies in india: international medicine delivery from india – world pharmacy india indianpharm.store

canadian online pharmacy: legitimate canadian pharmacy online – legit canadian online pharmacy canadianpharm.store

reputable mexican pharmacies online: Online Mexican pharmacy – mexican rx online mexicanpharm.shop

https://canadianpharm.store/# maple leaf pharmacy in canada canadianpharm.store

legitimate canadian pharmacy online Canadian International Pharmacy canadian pharmacy cheap canadianpharm.store

online pharmacy india: Indian pharmacy to USA – indian pharmacies safe indianpharm.store

http://indianpharm.store/# cheapest online pharmacy india indianpharm.store

prescription drugs canada buy online: canadian pharmacy review – safe canadian pharmacies canadianpharm.store

mexican pharmaceuticals online: Online Mexican pharmacy – п»їbest mexican online pharmacies mexicanpharm.shop

online pharmacy india: Indian pharmacy to USA – top 10 online pharmacy in india indianpharm.store

online shopping pharmacy india: top online pharmacy india – pharmacy website india indianpharm.store

http://mexicanpharm.shop/# buying prescription drugs in mexico mexicanpharm.shop

purple pharmacy mexico price list: Certified Pharmacy from Mexico – mexican pharmaceuticals online mexicanpharm.shop

online shopping pharmacy india Indian pharmacy to USA pharmacy website india indianpharm.store

mexico drug stores pharmacies: medicine in mexico pharmacies – mexican pharmaceuticals online mexicanpharm.shop

Your commitment to quality and depth in your writing is clear.

canadian drugstore viagra: azithromycin canadian pharmacy – best online drugstore

canadian online pharmacies legitimate: discount viagra canadian pharmacy – canadian internet pharmacies

levitra from canadian pharmacy: family pharmacy online – no prescription canadian pharmacies

medication online: express pharmacy – canadian drugs online pharmacy

prescription drugs canadian: buying drugs canada – canadian pharmacy no rx

legitimate canadian mail order pharmacy: canadian pharmacy generic viagra – canada prescriptions

no perscription drugs canada: reputable mexican pharmacies online – overseas online pharmacies

I admire the way you tackled this complex issue. Very enlightening!

best mexican online pharmacies: cheapest drug prices – cheap drug prices

medicin without prescription: medications canada – legit canadian pharmacy online

canadian medications: internet pharmacy – canada pharmacy not requiring prescription

reliable online drugstore: universal canadian pharmacy – pharmacy in canada

discount pharmacy coupons: top 10 online pharmacies – top mexican pharmacies

prescriptions from canada without: online prescriptions without script – canadian pharmacies recommended

aarp canadian pharmacy: mexican pharmacies online cheap – cheapest canadian pharmacy

online pharmacy mail order: my canadian pharmacy – medications canada

http://canadadrugs.pro/# canadian drugs pharmacies online

Amazing! This blog looks exactly like my old one! It’s on a totally different subject but it has pretty much the same layout and design. Great choice of colors! https://slashpage.com/dogal-taslar

no perscription drugs canada: india online pharmacy – legal canadian prescription drugs online

reliable online pharmacies: canada drugs – prescription drugs canadian

online meds: global pharmacy plus canada – canadian drugs online pharmacy

pharmacies online: buy online prescription drugs – global pharmacy plus canada

top rated online pharmacies: mexican pharmacy online no prescription – drug store online

purple pharmacy mexico price list: mexican online pharmacies prescription drugs – purple pharmacy mexico price list

https://medicinefromindia.store/# reputable indian online pharmacy

mexican pharmacy: pharmacies in mexico that ship to usa – mexican online pharmacies prescription drugs

ed meds online without doctor prescription: medications for ed – best ed pills

top 10 online pharmacy in india: indian pharmacy online – Online medicine order

https://medicinefromindia.store/# pharmacy website india

medicine in mexico pharmacies: mexican drugstore online – medication from mexico pharmacy

ed pills online: cheap erectile dysfunction pill – best drug for ed

http://canadianinternationalpharmacy.pro/# canadapharmacyonline

best ed pill: treatments for ed – natural ed remedies

https://medicinefromindia.store/# reputable indian online pharmacy

cure ed: ed treatment pills – what are ed drugs

pills for erection pills for erection online ed medications

non prescription ed drugs prescription without a doctor’s prescription legal to buy prescription drugs from canada

canada drugstore pharmacy rx canadian pharmacy 1 internet online drugstore canadadrugpharmacy com

cheapest online pharmacy india: buy medicines online in india – top 10 online pharmacy in india

http://edwithoutdoctorprescription.pro/# viagra without a doctor prescription

buy prescription drugs: buy prescription drugs online – prescription drugs without doctor approval

http://medicinefromindia.store/# indian pharmacy

2023’te yollara çıkması beklenen Türkiye’nin otomobili Togg’un CEO’su Gürcan Karakaş, lansmanı yapılacak ilk ürünün otomobil olmayacağını bildirdi. Karakaş,… Cherry Gold Casino No Deposit Bonus Code ‘INSIDERS’ is an exciting introductory offer giving new players a complementary $15 to try their luck with online gambling. With Cherry Gold Casino No Deposit Bonus Codes, you can enjoy one of the best online casino experiences in the US, with so many games and offers to choose from as both a new and existing customer. Join Cherry Gold Casino and you are going to be rewarded with an impressive Welcome bonus. Visit Cherry Gold Casino A quadruple your money bonus is awarded to you once a deposit of $25 or more is made. Enter the bonus code: APHRODITE at the cashier to super-charge your bankroll today! Bonus Welcome Bonus Type Deposit Match Match 300% Minimum Deposit $25 Minimum Bonus $75 Wagering Requirements (WR) …

https://edgarrqok185185.blogkoo.com/highest-payout-slots-online-39674624

Run and operated by Caesars Entertainment, the casino is owned by the Eastern Band of Cherokee Indians. They also own the Cherokee Valley River Casino in Murphy. (More on that later). Sound familiar? It should. It’s the kind of job you’ve been dreaming of with a starting wage of $15.00 for non tipped positions. Hiring bonuses up to $3,000 for select jobs. Gabriel “Fluffy” Iglesias is one of America's most successful stand-up comedians performing at sold-out concerts around the world. He is also one of the most-watched comedians on YouTube with almost a Give us your email address to receive updates on what’s going on, plus you’ll receive exclusive offers! Each guestroom is kept vacant for a minimum of 24 hours between bookings. For an entirely different change of pace, consider an excursion into nearby Murphy, NC to visit the Harrah’s Cherokee Valley River Casino & Hotel. This Harrah’s location is a part of the Caesars Rewards loyalty program that includes over 50 locations worldwide!

https://medicinefromindia.store/# best online pharmacy india

best online pharmacy india

canada pharmacy reviews: canada drugs online review – best mail order pharmacy canada

http://edwithoutdoctorprescription.pro/# non prescription ed pills

http://certifiedpharmacymexico.pro/# buying prescription drugs in mexico

reputable mexican pharmacies online mexico pharmacy mexican pharmacy

https://mexicanph.shop/# buying prescription drugs in mexico

mexico pharmacies prescription drugs

mexican drugstore online mexico pharmacy medicine in mexico pharmacies

http://mexicanph.com/# mexican pharmaceuticals online

medication from mexico pharmacy

pharmacies in mexico that ship to usa medicine in mexico pharmacies reputable mexican pharmacies online

buying from online mexican pharmacy mexican drugstore online buying prescription drugs in mexico

pharmacies in mexico that ship to usa mexican pharmacy purple pharmacy mexico price list

mexican pharmacy п»їbest mexican online pharmacies buying prescription drugs in mexico

http://mexicanph.shop/# mexico drug stores pharmacies

mexican rx online

mexican pharmaceuticals online mexican border pharmacies shipping to usa pharmacies in mexico that ship to usa

mexico pharmacy best online pharmacies in mexico best mexican online pharmacies

best online pharmacies in mexico buying from online mexican pharmacy medication from mexico pharmacy

mexican drugstore online mexican online pharmacies prescription drugs mexican pharmaceuticals online

mexican pharmaceuticals online mexican mail order pharmacies mexican rx online

https://mexicanph.com/# buying prescription drugs in mexico

mexico drug stores pharmacies

п»їbest mexican online pharmacies mexican online pharmacies prescription drugs mexico pharmacies prescription drugs

mexico pharmacies prescription drugs mexican online pharmacies prescription drugs mexican border pharmacies shipping to usa

mexico drug stores pharmacies reputable mexican pharmacies online mexican rx online

п»їbest mexican online pharmacies purple pharmacy mexico price list mexico drug stores pharmacies

https://mexicanph.shop/# mexican mail order pharmacies

medicine in mexico pharmacies

mexican mail order pharmacies best mexican online pharmacies mexican pharmacy

mexican drugstore online medicine in mexico pharmacies reputable mexican pharmacies online

mexico pharmacies prescription drugs mexican drugstore online medicine in mexico pharmacies

mexican pharmaceuticals online mexican border pharmacies shipping to usa medication from mexico pharmacy

mexican pharmacy mexican border pharmacies shipping to usa buying prescription drugs in mexico online

mexico drug stores pharmacies mexico pharmacy medication from mexico pharmacy

mexican mail order pharmacies mexico pharmacies prescription drugs pharmacies in mexico that ship to usa

medicine in mexico pharmacies mexico pharmacy medication from mexico pharmacy

mexico drug stores pharmacies mexico pharmacy reputable mexican pharmacies online

mexico pharmacies prescription drugs mexican mail order pharmacies mexican drugstore online

buying prescription drugs in mexico buying from online mexican pharmacy mexican pharmacy

https://mexicanph.com/# mexico drug stores pharmacies

pharmacies in mexico that ship to usa

mexican online pharmacies prescription drugs mexico drug stores pharmacies buying from online mexican pharmacy

mexican drugstore online buying from online mexican pharmacy mexican rx online

mexico pharmacy mexican online pharmacies prescription drugs best mexican online pharmacies

best online pharmacies in mexico pharmacies in mexico that ship to usa mexican border pharmacies shipping to usa

purple pharmacy mexico price list mexican rx online buying prescription drugs in mexico online

mexican pharmacy best online pharmacies in mexico mexico pharmacy

pharmacies in mexico that ship to usa mexican online pharmacies prescription drugs best online pharmacies in mexico

mexico pharmacies prescription drugs reputable mexican pharmacies online mexican pharmaceuticals online

п»їbest mexican online pharmacies medicine in mexico pharmacies mexican online pharmacies prescription drugs

medication from mexico pharmacy buying prescription drugs in mexico mexican online pharmacies prescription drugs

mexico pharmacies prescription drugs mexican border pharmacies shipping to usa medicine in mexico pharmacies

mexico pharmacy best mexican online pharmacies best mexican online pharmacies

https://mexicanph.shop/# reputable mexican pharmacies online

reputable mexican pharmacies online

mexico pharmacies prescription drugs buying prescription drugs in mexico online best mexican online pharmacies

pharmacies in mexico that ship to usa mexican drugstore online buying prescription drugs in mexico online

buying prescription drugs in mexico mexico drug stores pharmacies purple pharmacy mexico price list

best mexican online pharmacies mexico drug stores pharmacies mexican drugstore online

mexico pharmacy mexican drugstore online buying prescription drugs in mexico online

mexican rx online mexican rx online reputable mexican pharmacies online

buying from online mexican pharmacy mexican border pharmacies shipping to usa mexico pharmacy

mexico drug stores pharmacies best online pharmacies in mexico mexican pharmacy

https://mexicanph.com/# buying prescription drugs in mexico online

purple pharmacy mexico price list

best online pharmacies in mexico mexican drugstore online mexican border pharmacies shipping to usa

purple pharmacy mexico price list mexico pharmacies prescription drugs mexican online pharmacies prescription drugs

mexican pharmaceuticals online pharmacies in mexico that ship to usa mexican pharmaceuticals online

buying prescription drugs in mexico online mexican mail order pharmacies mexican mail order pharmacies

mexican drugstore online mexico drug stores pharmacies medication from mexico pharmacy

mexican pharmaceuticals online buying prescription drugs in mexico online mexican drugstore online

reputable mexican pharmacies online medication from mexico pharmacy buying prescription drugs in mexico

mexican drugstore online buying from online mexican pharmacy п»їbest mexican online pharmacies

reputable mexican pharmacies online mexico drug stores pharmacies mexico pharmacies prescription drugs

buying from online mexican pharmacy mexico drug stores pharmacies mexican mail order pharmacies

pharmacies in mexico that ship to usa buying from online mexican pharmacy buying from online mexican pharmacy

https://mexicanph.shop/# mexican border pharmacies shipping to usa

mexico drug stores pharmacies

buying prescription drugs in mexico mexican online pharmacies prescription drugs mexican drugstore online

purple pharmacy mexico price list medicine in mexico pharmacies buying prescription drugs in mexico

buying prescription drugs in mexico online medication from mexico pharmacy mexican pharmaceuticals online

mexico pharmacies prescription drugs buying from online mexican pharmacy buying prescription drugs in mexico

https://lisinopril.top/# lisinopril 10 mg tablet cost

lisinopril 2018 lisinopril 20 mg tab price price for 5 mg lisinopril

prednisone 7.5 mg: how can i order prednisone – prednisone 10mg tabs

http://amoxil.cheap/# amoxicillin 875 125 mg tab

http://lisinopril.top/# lisinopril 30

generic lasix: Buy Lasix No Prescription – lasix tablet

amoxicillin medicine amoxicillin script amoxicillin 500 mg capsule

https://buyprednisone.store/# how to purchase prednisone online

http://stromectol.fun/# stromectol price usa

buy ivermectin nz: ivermectin 18mg – ivermectin for sale

cheap lisinopril no prescription lisinopril 30 mg price prinivil 20mg tabs

http://furosemide.guru/# furosemide 100 mg

http://lisinopril.top/# lisinopril 3972

lisinopril 5mg tabs: zestril 40 mg tablet – lisinopril 2.5 pill

amoxicillin 500 mg without a prescription: buy amoxicillin 500mg usa – amoxicillin medicine over the counter

http://stromectol.fun/# ivermectin 0.08 oral solution

ampicillin amoxicillin where can i buy amoxicillin over the counter amoxicillin where to get

https://stromectol.fun/# stromectol 3 mg tablet price

http://stromectol.fun/# generic name for ivermectin

lisinopril 5 mg: medication lisinopril 5 mg – lisinopril 5mg

http://furosemide.guru/# lasix 40 mg

https://furosemide.guru/# lasix pills

lasix 100 mg: Over The Counter Lasix – lasix

http://stromectol.fun/# stromectol medication

generic lisinopril 10 mg: lisinopril 30mg coupon – zestoretic canada

http://furosemide.guru/# lasix 100 mg tablet

http://stromectol.fun/# ivermectin 4 mg

https://furosemide.guru/# lasix 100 mg tablet

ivermectin 24 mg: ivermectin 0.08 oral solution – ivermectin 50

buy furosemide online: Buy Furosemide – lasix for sale

zestril 5 mg price price of lisinopril buy lisinopril online no prescription india

http://stromectol.fun/# cost of ivermectin cream

https://stromectol.fun/# stromectol uk buy

lasix tablet lasix furosemide 40 mg lasix 20 mg

lasix generic name: Buy Furosemide – lasix furosemide 40 mg

http://furosemide.guru/# furosemide 40mg

amoxicillin 500 mg cost: amoxicillin medicine – antibiotic amoxicillin

https://lisinopril.top/# lisinopril price

http://furosemide.guru/# lasix for sale

ivermectin 3 mg ivermectin over the counter uk ivermectin 0.2mg

https://buyprednisone.store/# cheapest prednisone no prescription

cost of ivermectin: ivermectin gel – ivermectin tablets order

https://amoxil.cheap/# amoxicillin without a prescription

lisinopril 30 mg price: generic lisinopril 3973 – lisinopril 40 mg purchase

lasix furosemide 40 mg furosemide 100 mg lasix side effects

http://buyprednisone.store/# prednisone best prices

lisinopril 2.5 mg medicine: lisinopril 20 25 mg – price of lisinopril in india

https://buyprednisone.store/# prednisone buy cheap

https://furosemide.guru/# furosemida

http://amoxil.cheap/# amoxicillin 800 mg price

lisinopril 2.5 lisinopril 20 mg tablet cost lisinopril 20 mg generic

ivermectin over the counter uk: ivermectin 5 mg price – stromectol tablets for humans

https://buyprednisone.store/# 10 mg prednisone

ivermectin 8000: stromectol for sale – ivermectin 4 tablets price

http://furosemide.guru/# lasix furosemide

zestril 5 mg tablet 50mg lisinopril 30mg lisinopril

stromectol in canada: stromectol uk – ivermectin 12

https://lisinopril.top/# ordering lisinopril without a prescription

lasix tablet: Buy Lasix – lasix uses

http://lisinopril.top/# lisinopril 20mg india

average price of prednisone prednisone uk prednisone 2.5 mg

lisinopril price 10 mg: how to order lisinopril online – lisinopril 3972

http://stromectol.fun/# ivermectin 5

https://buyprednisone.store/# prednisone 1 mg daily

generic lisinopril 5 mg: zestoretic generic – lisinopril tablets india

https://stromectol.fun/# stromectol tablet 3 mg

https://amoxil.cheap/# where to buy amoxicillin pharmacy

buy prednisone with paypal canada: purchase prednisone 10mg – where to buy prednisone 20mg no prescription

https://stromectol.fun/# ivermectin 3mg tablets

amoxicillin where to get: amoxicillin cost australia – amoxicillin 500 coupon

amoxicillin without a doctors prescription amoxicillin order online can i buy amoxicillin over the counter

https://furosemide.guru/# lasix side effects

https://indianph.com/# india pharmacy

https://indianph.xyz/# buy medicines online in india

best online pharmacy india

http://indianph.com/# world pharmacy india

top 10 online pharmacy in india

http://indianph.xyz/# top 10 pharmacies in india

buy medicines online in india

indian pharmacies safe cheapest online pharmacy india п»їlegitimate online pharmacies india

https://indianph.com/# reputable indian online pharmacy

indian pharmacy paypal

https://indianph.xyz/# top 10 online pharmacy in india

indianpharmacy com

http://indianph.xyz/# top 10 pharmacies in india

pharmacy website india pharmacy website india best online pharmacy india

https://indianph.com/# online pharmacy india

top 10 online pharmacy in india

buy prescription drugs from india cheapest online pharmacy india top 10 pharmacies in india

https://indianph.com/# top 10 online pharmacy in india

online shopping pharmacy india

https://indianph.xyz/# top online pharmacy india

top 10 online pharmacy in india

buy doxycycline without prescription uk buy doxycycline for dogs buy doxycycline cheap

https://cytotec24.shop/# buy cytotec in usa

https://nolvadex.guru/# cost of tamoxifen

where can i get diflucan online: diflucan over the counter pill – can i buy diflucan in mexico

http://doxycycline.auction/# how to buy doxycycline online

nolvadex for pct tamoxifen chemo does tamoxifen cause weight loss

https://nolvadex.guru/# aromatase inhibitor tamoxifen

http://cipro.guru/# ciprofloxacin order online

п»їcytotec pills online: cytotec abortion pill – Cytotec 200mcg price

diflucan buy in usa diflucan medicine diflucan tablets buy online no script

http://cipro.guru/# buy cipro

https://cytotec24.shop/# buy misoprostol over the counter

http://cipro.guru/# buy ciprofloxacin over the counter

ciprofloxacin generic ciprofloxacin order online cipro for sale

http://doxycycline.auction/# buy doxycycline without prescription

https://cytotec24.shop/# cytotec online

diflucan fluconazole: diflucan medication prescription – diflucan buy without prescription

diflucan tablets australia buy diflucan prescription med buy diflucan canada

http://diflucan.pro/# diflucan men

https://cytotec24.shop/# buy cytotec online fast delivery

https://diflucan.pro/# diflucan pill for sale

cytotec online cytotec buy online usa buy misoprostol over the counter

https://cytotec24.shop/# Cytotec 200mcg price

http://diflucan.pro/# diflucan australia

tamoxifen chemo tamoxifen for gynecomastia reviews tamoxifen alternatives

https://doxycycline.auction/# doxycycline 100mg online

http://diflucan.pro/# diflucan generic price

where can you get diflucan diflucan otc canada diflucan 400mg without prescription

https://cytotec24.com/# order cytotec online

tamoxifen side effects forum tamoxifen breast cancer prevention what happens when you stop taking tamoxifen

http://angelawhite.pro/# Angela White

https://evaelfie.pro/# eva elfie izle

https://abelladanger.online/# Abella Danger

https://angelawhite.pro/# Angela White filmleri

http://evaelfie.pro/# eva elfie izle

https://sweetiefox.online/# Sweetie Fox izle

https://angelawhite.pro/# ?????? ????

https://lanarhoades.fun/# lana rhoades modeli

http://evaelfie.pro/# eva elfie

http://evaelfie.pro/# eva elfie izle

http://abelladanger.online/# abella danger filmleri

https://abelladanger.online/# abella danger video

http://angelawhite.pro/# Angela Beyaz modeli

https://abelladanger.online/# abella danger video

http://sweetiefox.online/# sweety fox

https://sweetiefox.online/# Sweetie Fox filmleri

http://evaelfie.pro/# eva elfie izle

https://lanarhoades.fun/# lana rhoades

http://evaelfie.pro/# eva elfie izle

https://angelawhite.pro/# Angela White filmleri

lana rhodes: lana rhoades – lana rhoades filmleri

http://angelawhite.pro/# Angela White filmleri

http://sweetiefox.online/# Sweetie Fox izle

http://abelladanger.online/# Abella Danger

https://evaelfie.pro/# eva elfie izle

https://abelladanger.online/# abella danger filmleri

https://sweetiefox.online/# sweety fox

http://evaelfie.pro/# eva elfie

http://lanarhoades.fun/# lana rhoades

Angela White filmleri: Abella Danger – abella danger izle

https://lanarhoades.fun/# lana rhoades izle

http://abelladanger.online/# Abella Danger

http://evaelfie.pro/# eva elfie video

eva elfie: eva elfie – eva elfie

https://sweetiefox.online/# Sweetie Fox video

http://sweetiefox.online/# sweety fox

mia malkova videos: mia malkova – mia malkova full video

fox sweetie: sweetie fox new – ph sweetie fox

https://sweetiefox.pro/# sweetie fox video

ph sweetie fox: sweetie fox new – sweetie fox cosplay

dating sim: https://miamalkova.life/# mia malkova girl

lana rhoades hot: lana rhoades – lana rhoades pics

sweetie fox video: sweetie fox full – sweetie fox cosplay

https://miamalkova.life/# mia malkova new video

lana rhoades unleashed: lana rhoades – lana rhoades videos

dafing sites: http://evaelfie.site/# eva elfie

fox sweetie: fox sweetie – sweetie fox

http://lanarhoades.pro/# lana rhoades solo

lana rhoades videos: lana rhoades hot – lana rhoades

eva elfie hd: eva elfie full videos – eva elfie

https://evaelfie.site/# eva elfie full videos

free and single: https://miamalkova.life/# mia malkova photos

eva elfie full videos: eva elfie new video – eva elfie full videos

eva elfie new video: eva elfie full videos – eva elfie new video

http://sweetiefox.pro/# sweetie fox video

sweetie fox video: sweetie fox full video – fox sweetie

free online chatting and dating: http://miamalkova.life/# mia malkova latest

http://sweetiefox.pro/# sweetie fox full video

sweetie fox full video: sweetie fox full – fox sweetie

eva elfie: eva elfie hot – eva elfie

https://sweetiefox.pro/# ph sweetie fox

good dating site: https://sweetiefox.pro/# sweetie fox cosplay

lana rhoades unleashed: lana rhoades full video – lana rhoades boyfriend

eva elfie new video: eva elfie videos – eva elfie full videos

http://miamalkova.life/# mia malkova movie

eris free downloads chatting apps: https://evaelfie.site/# eva elfie

lana rhoades pics: lana rhoades unleashed – lana rhoades videos

https://lanarhoades.pro/# lana rhoades

jogo de aposta: depósito mínimo 1 real – ganhar dinheiro jogando

https://aviatoroyunu.pro/# pin up aviator

pin up: pin-up casino login – pin-up casino

aviator game online: aviator betting game – aviator game

http://aviatoroyunu.pro/# aviator oyna

https://aviatorghana.pro/# aviator game

aviator game: aviator game – play aviator

http://aviatoroyunu.pro/# aviator oyna

aviator: aviator oyunu – aviator oyna slot

http://aviatoroyunu.pro/# aviator oyunu

aviator bahis: aviator bahis – aviator

aviator mz: aviator online – como jogar aviator

https://jogodeaposta.fun/# aviator jogo de aposta

http://aviatormalawi.online/# aviator game

aviator online: aviator online – aviator moçambique

aviator game bet: aviator game – aviator sportybet ghana

ganhar dinheiro jogando: ganhar dinheiro jogando – melhor jogo de aposta

aviator bet malawi login: aviator bet malawi – aviator game online

https://jogodeaposta.fun/# melhor jogo de aposta

como jogar aviator: jogar aviator – jogar aviator

aviator ghana: aviator betting game – aviator betting game

https://aviatormocambique.site/# jogar aviator

melhor jogo de aposta: aviator jogo de aposta – jogo de aposta online

aviator game bet: aviator bet – aviator game

can you buy zithromax over the counter in canada: zithromax purchase online – zithromax 500

http://jogodeaposta.fun/# jogos que dao dinheiro

pin-up cassino: pin-up casino login – pin up

site de apostas: ganhar dinheiro jogando – ganhar dinheiro jogando

zithromax prescription in canada: buy zithromax 500mg online – zithromax cost uk

aviator mz: como jogar aviator em mocambique – jogar aviator

indianpharmacy com: Top online pharmacy in India – reputable indian pharmacies indianpharm.store

https://mexicanpharm24.com/# medication from mexico pharmacy mexicanpharm.shop

buy canadian drugs: canadian pharmacy – precription drugs from canada canadianpharm.store

canadian pharmacy online store canadian pharmacy canada rx pharmacy canadianpharm.store

https://indianpharm24.shop/# world pharmacy india indianpharm.store

online pharmacy canada: International Pharmacy delivery – canadian online pharmacy canadianpharm.store

the canadian drugstore: Cheapest drug prices Canada – reliable canadian pharmacy canadianpharm.store

http://canadianpharmlk.shop/# escrow pharmacy canada canadianpharm.store

https://mexicanpharm24.shop/# mexican pharmaceuticals online mexicanpharm.shop

mexican mail order pharmacies Mexico pharmacy price list mexican drugstore online mexicanpharm.shop

https://mexicanpharm24.shop/# mexico pharmacy mexicanpharm.shop

my canadian pharmacy: Cheapest drug prices Canada – canada drugs reviews canadianpharm.store

mexican online pharmacies prescription drugs: buying prescription drugs in mexico – mexican pharmaceuticals online mexicanpharm.shop

https://indianpharm24.com/# indian pharmacy indianpharm.store

http://indianpharm24.com/# india pharmacy mail order indianpharm.store

buying prescription drugs in mexico online: Mexico pharmacy price list – medication from mexico pharmacy mexicanpharm.shop

https://mexicanpharm24.shop/# mexican pharmaceuticals online mexicanpharm.shop

https://canadianpharmlk.shop/# thecanadianpharmacy canadianpharm.store

http://indianpharm24.com/# india online pharmacy indianpharm.store

indian pharmacies safe: Generic Medicine India to USA – best india pharmacy indianpharm.store

https://indianpharm24.shop/# buy medicines online in india indianpharm.store

https://mexicanpharm24.com/# buying prescription drugs in mexico online mexicanpharm.shop

http://mexicanpharm24.com/# buying from online mexican pharmacy mexicanpharm.shop

http://canadianpharmlk.com/# reliable canadian pharmacy canadianpharm.store

legitimate canadian mail order pharmacy: International Pharmacy delivery – best online canadian pharmacy canadianpharm.store

legitimate canadian pharmacy online Pharmacies in Canada that ship to the US safe online pharmacies in canada canadianpharm.store

https://indianpharm24.com/# indian pharmacy paypal indianpharm.store

prednisone pill 20 mg: buy prednisone without a prescription best price – prednisone 30 mg

ordering prednisone: prednisone dosage – 200 mg prednisone daily

prednisone 20mg capsule: prednisone alcohol – prednisone 5443

get generic clomid without rx: clomiphene vs clomid – how to buy clomid no prescription

amoxicillin 500mg cost: how long is amoxicillin good for – amoxicillin from canada

prednisone tablets india: does prednisone cause weight gain – prednisone 7.5 mg

prednisone 5 mg tablet rx: prednisone drug class – prednisone 500 mg tablet

azithromycin amoxicillin: buy amoxicillin online no prescription – amoxicillin 200 mg tablet

order prednisone on line can i buy prednisone online without a prescription price for 15 prednisone

https://clomidst.pro/# can you get clomid without prescription

where to get clomid no prescription: clomid women – buy generic clomid without rx

where buy generic clomid prices: can you drink on clomid – clomid without prescription

can i buy cheap clomid no prescription: clomid women – can you buy generic clomid without a prescription

http://clomidst.pro/# can i buy cheap clomid

prednisone buy canada: prednisone 20mg buy online – prednisone 20 mg in india

can i buy cheap clomid for sale: buying generic clomid prices – can i order generic clomid no prescription

amoxicillin 500 mg cost: how to get amoxicillin over the counter – amoxicillin over counter

http://clomidst.pro/# can i get generic clomid without insurance

where can i buy cheap clomid pill cost of generic clomid no prescription buy cheap clomid prices

cost cheap clomid without dr prescription: clomid sale – clomid generic

amoxicillin 500mg capsule cost: amoxicillin for pneumonia – amoxicillin 500 mg price

http://amoxilst.pro/# where to buy amoxicillin pharmacy

order clomid prices: clomid ovulation calculator – cost clomid without rx

can i buy cheap clomid online: clomid ovulation calculator – can i purchase clomid without insurance

http://clomidst.pro/# where to get clomid without rx

where buy clomid no prescription: clomid 50 mg – can i get clomid pills

http://edpills.guru/# cheapest ed treatment

canadian pharmacy online no prescription: online no prescription pharmacy – online meds no prescription

discount ed meds: cheapest erectile dysfunction pills – how to get ed meds online

order ed pills affordable ed medication cheap ed medicine

no prescription required pharmacy: canada online pharmacy – rx pharmacy no prescription

http://edpills.guru/# online ed medication

best canadian pharmacy no prescription: mexican pharmacy online – online pharmacy no prescription

https://pharmnoprescription.pro/# can you buy prescription drugs in canada

ed medications online: ed drugs online – get ed meds online

http://pharmnoprescription.pro/# online pharmacy without prescription

reputable online pharmacy no prescription: mexican online pharmacy – us pharmacy no prescription

buy ed meds online: buy erectile dysfunction pills online – online ed medications

best online pharmacy no prescription: pharmacy online – cheapest pharmacy for prescription drugs

ed treatments online erectile dysfunction online prescription best online ed pills

pharmacy no prescription required: canadian online pharmacy – no prescription required pharmacy

https://onlinepharmacy.cheap/# canadian pharmacy no prescription needed

low cost ed pills: cheapest online ed treatment – ed treatment online

buy medications without prescriptions: canada pharmacy no prescription – overseas online pharmacy-no prescription

canadian pharmacy without prescription: canadian pharmacy online – cheapest pharmacy for prescriptions without insurance

https://edpills.guru/# low cost ed meds online

how to get ed meds online: pills for erectile dysfunction online – ed medications online

http://edpills.guru/# low cost ed meds online

online ed medication: cheapest ed pills – online prescription for ed

online pharmacy discount code canadian online pharmacy canadian online pharmacy no prescription

online shopping pharmacy india: indian pharmacies safe – top 10 pharmacies in india

http://indianpharm.shop/# india pharmacy

prescription from canada: canada pharmacies online prescriptions – buying drugs online no prescription

https://mexicanpharm.online/# mexican online pharmacies prescription drugs

canada pharmacies online prescriptions: no prescription online pharmacies – buy prescription online

http://indianpharm.shop/# online pharmacy india

http://indianpharm.shop/# world pharmacy india

mexican border pharmacies shipping to usa: mexican pharmaceuticals online – mexican pharmaceuticals online

india pharmacy: pharmacy website india – legitimate online pharmacies india

mail order pharmacy india: pharmacy website india – top 10 online pharmacy in india

mexican pharmaceuticals online: mexican mail order pharmacies – pharmacies in mexico that ship to usa

pharmacy website india: indian pharmacy online – best india pharmacy

https://pharmacynoprescription.pro/# canadian prescription drugstore review

canadian pharmacy no scripts: cross border pharmacy canada – canadian pharmacy ltd

medicine in mexico pharmacies pharmacies in mexico that ship to usa pharmacies in mexico that ship to usa

indian pharmacies safe: п»їlegitimate online pharmacies india – best online pharmacy india

http://canadianpharm.guru/# pharmacies in canada that ship to the us

http://pharmacynoprescription.pro/# indian pharmacy no prescription

indian pharmacies safe: Online medicine order – legitimate online pharmacies india

indian pharmacies safe: india online pharmacy – reputable indian pharmacies

legitimate online pharmacies india: indianpharmacy com – india pharmacy mail order

medication from mexico pharmacy: mexico pharmacy – buying prescription drugs in mexico

mexican online pharmacies prescription drugs: reputable mexican pharmacies online – best mexican online pharmacies

canadian pharmacy scam: buy canadian drugs – legitimate canadian pharmacies

https://indianpharm.shop/# cheapest online pharmacy india

best non prescription online pharmacy: online medication without prescription – online drugstore no prescription

best online pharmacies in mexico: pharmacies in mexico that ship to usa – mexican rx online

medicine in mexico pharmacies buying prescription drugs in mexico online medicine in mexico pharmacies

mexican pharmacy: buying from online mexican pharmacy – mexico pharmacies prescription drugs

http://canadianpharm.guru/# best canadian online pharmacy

no prescription drugs: overseas online pharmacy-no prescription – canada drugs no prescription

purple pharmacy mexico price list: purple pharmacy mexico price list – mexican pharmaceuticals online

pharmacy website india: mail order pharmacy india – online pharmacy india

http://indianpharm.shop/# Online medicine home delivery

buy pills without prescription: buy prescription drugs without a prescription – no prescription drugs

medication online without prescription: online canadian pharmacy no prescription – online pharmacies without prescription

https://indianpharm.shop/# Online medicine home delivery

india pharmacy mail order india pharmacy indian pharmacy paypal

indian pharmacy: legitimate online pharmacies india – indian pharmacy online

https://mexicanpharm.online/# mexican mail order pharmacies

buy drugs online without prescription: meds no prescription – best online prescription

buy prescription drugs from india: reputable indian pharmacies – best india pharmacy

canadian pharmacy service: canadian pharmacy 1 internet online drugstore – canadian discount pharmacy

buy prescription drugs from india: world pharmacy india – buy prescription drugs from india

adderall canadian pharmacy: canadian pharmacy 365 – canadian pharmacy ratings

india pharmacy: top online pharmacy india – Online medicine home delivery

pharmacy website india: india online pharmacy – reputable indian pharmacies

canadian discount pharmacy: online canadian drugstore – reputable canadian pharmacy

top 10 pharmacies in india online pharmacy india п»їlegitimate online pharmacies india

http://pharmacynoprescription.pro/# online meds no prescription

buying prescription drugs in mexico: mexican pharmacy – mexican border pharmacies shipping to usa

canadian pharmacy checker: best canadian pharmacy online – canadian pharmacy no rx needed

buy pills without prescription: no prescription online pharmacies – mexico prescription drugs online

http://indianpharm.shop/# top online pharmacy india

online pharmacy india: indian pharmacy paypal – indian pharmacy online

best online pharmacies in mexico: mexican rx online – mexico pharmacies prescription drugs

https://canadianpharm.guru/# legitimate canadian pharmacy online

mexico pharmacy: best mexican online pharmacies – mexico drug stores pharmacies

buying prescription drugs in mexico: buying from online mexican pharmacy – mexican pharmaceuticals online

canadian pharmacy no prescription needed canada prescriptions by mail no prescription pharmacy online

http://indianpharm.shop/# best online pharmacy india

canada online prescription: online drugs no prescription – buy prescription online

sweet bonanza demo: sweet bonanza – sweet bonanza yasal site

https://aviatoroyna.bid/# aviator

http://slotsiteleri.guru/# yasal slot siteleri

http://sweetbonanza.bid/# sweet bonanza 90 tl

http://pinupgiris.fun/# pin up 7/24 giris

slot bahis siteleri: bonus veren casino slot siteleri – en iyi slot siteleri

sweet bonanza hilesi: sweet bonanza demo – guncel sweet bonanza

http://gatesofolympus.auction/# gates of olympus demo

http://gatesofolympus.auction/# gates of olympus taktik

http://aviatoroyna.bid/# aviator

https://pinupgiris.fun/# pin up aviator

aviator oyunu: aviator – aviator hilesi

http://sweetbonanza.bid/# sweet bonanza kazanma saatleri

aviator nas?l oynan?r: ucak oyunu bahis aviator – aviator giris

aviator pin up: pin up guncel giris – pin up aviator

http://sweetbonanza.bid/# sweet bonanza 100 tl

http://pinupgiris.fun/# pin-up casino giris

http://pinupgiris.fun/# pin up

https://gatesofolympus.auction/# gates of olympus 1000 demo

pin up: pin-up giris – pin-up bonanza

http://aviatoroyna.bid/# aviator uçak oyunu

pin-up casino indir: aviator pin up – pin-up casino

https://pinupgiris.fun/# pin-up bonanza

https://aviatoroyna.bid/# aviator oyna 20 tl

https://gatesofolympus.auction/# gates of olympus demo oyna

https://pinupgiris.fun/# pin up 7/24 giris

slot casino siteleri: yasal slot siteleri – en guvenilir slot siteleri

https://pinupgiris.fun/# pin up casino indir

pragmatic play gates of olympus: pragmatic play gates of olympus – gates of olympus hilesi

https://aviatoroyna.bid/# aviator oyna 20 tl

indian pharmacy Healthcare and medicines from India indianpharmacy com

reputable indian pharmacies: indian pharmacy – best india pharmacy

reliable canadian pharmacy: Prescription Drugs from Canada – canadian pharmacy drugs online

mexican online pharmacies prescription drugs mexican pharmacy mexican mail order pharmacies

https://mexicanpharmacy.shop/# mexican rx online

best online pharmacies in mexico: cheapest mexico drugs – medicine in mexico pharmacies

mexican mail order pharmacies mexican rx online mexican pharmaceuticals online

reputable indian pharmacies: indian pharmacy – buy prescription drugs from india

buying from online mexican pharmacy mexican pharmacy buying prescription drugs in mexico

online shopping pharmacy india: indian pharmacies safe – Online medicine order

indian pharmacies safe: indian pharmacy – indianpharmacy com

pharmacies in mexico that ship to usa: Mexican Pharmacy Online – mexican mail order pharmacies

buying from online mexican pharmacy mexican pharmacy pharmacies in mexico that ship to usa

canada drugs online reviews: canadian pharmacy 24 – canadian pharmacy online reviews

http://canadianpharmacy24.store/# legitimate canadian pharmacy online

online pharmacy india: indian pharmacy – indian pharmacy online

mexico drug stores pharmacies: Online Pharmacies in Mexico – mexican border pharmacies shipping to usa

mexico pharmacies prescription drugs: Mexican Pharmacy Online – mexican border pharmacies shipping to usa

canadian pharmacy meds review: pills now even cheaper – the canadian pharmacy

reputable indian pharmacies indian pharmacy indianpharmacy com

indianpharmacy com: Healthcare and medicines from India – Online medicine order

mexico pharmacy: mexico pharmacy – mexican drugstore online

the canadian drugstore Licensed Canadian Pharmacy canadian pharmacy prices

best india pharmacy: indian pharmacy delivery – buy medicines online in india

top online pharmacy india: top 10 pharmacies in india – buy prescription drugs from india

pharmacy canadian superstore: Licensed Canadian Pharmacy – canadapharmacyonline

https://indianpharmacy.icu/# india pharmacy

canadian pharmacy price checker Licensed Canadian Pharmacy canadian pharmacy ed medications

escrow pharmacy canada: Certified Canadian Pharmacy – canadian drug stores

buy prescription drugs from india indian pharmacy delivery mail order pharmacy india

buying prescription drugs in mexico online: cheapest mexico drugs – mexican drugstore online

northern pharmacy canada Licensed Canadian Pharmacy canadian online drugs

canada drugstore pharmacy rx: Large Selection of Medications – canadian pharmacy

http://prednisoneall.shop/# purchase prednisone no prescription

prednisone 40 mg can i purchase prednisone without a prescription online prednisone 5mg

http://clomidall.shop/# how to get cheap clomid price

http://prednisoneall.shop/# average cost of generic prednisone

generic zithromax medicine: can you buy zithromax over the counter in mexico – zithromax 500 mg

https://clomidall.com/# can i buy clomid prices

zithromax 250: can you buy zithromax over the counter in australia – buy generic zithromax no prescription

generic zithromax over the counter where can you buy zithromax zithromax price south africa

https://prednisoneall.com/# buy cheap prednisone

can i order cheap clomid tablets where can i get cheap clomid without a prescription can you get cheap clomid

http://prednisoneall.com/# prednisone 20 mg generic

http://amoxilall.com/# amoxicillin medicine

can i purchase clomid now clomid without a prescription can i get clomid pill

http://clomidall.shop/# how to buy generic clomid

http://prednisoneall.shop/# buy prednisone online fast shipping

where to get clomid now: where buy cheap clomid without insurance – how to get clomid without insurance

amoxicillin online without prescription amoxicillin cost australia amoxicillin order online no prescription

https://amoxilall.shop/# how to get amoxicillin