The technical answer is yes. Android AOSP (Android open source project) meaning Android code that can be freely taken and used will be installed on more tablets than iPads in 2013. But the story isn’t that simple or clean cut. Data requires perspective and that is what I hope to provide around IDC’s latest press release and chart predicting that Android will be on more tablets than iOS in 2013 and beyond.

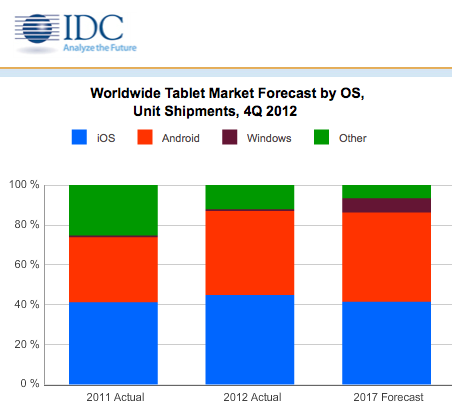

Here is the original IDC chart.

Now at first glance we look at that chart and mistakingly assume that the red part, which signifies Android, means a flavor of Android with universal value to both Google and developers. If I was a developer, I would look at that chart and think that Android tablets must be where I should focus my resources because it is clearly the OS market share leader starting in 2013 and beyond. However, if I thought that I would be wrong.

To clearly understand the Android picture we need to better understand the flavors of the OS and in particular which ones have the Google Play store and which ones do not. Because what really matters if we are interested in a clear industry picture of OS platform share is the distribution mechanisms for applications on each platform. If iOS represents a certain amount of market share then I can be confident that Apple’s app store is on that percentage of devices and install base.

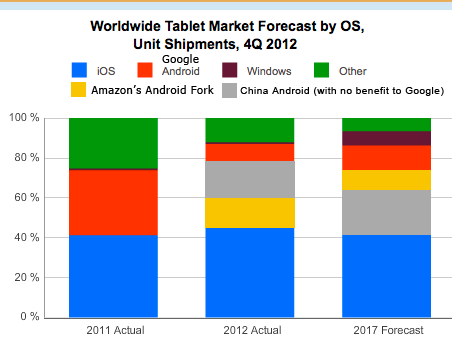

The problem when we talk about Android market share in both smartphones and tablets, is that we are not talking about market share in which a universal app store medium exists. This is because Android can be taken and forked, to the chagrin of Google, and used for the sole agenda of others thus not benefiting Google or the Play Store developers. This is the problem we have when we look at the Android growth in tablets. The greatest percentage of it is coming from Amazon with their Kindle fire, and the Chinese market. The Kindle Fire runs a forked version of Android and developers must use Amazon’s SDK and proprietary app store. 90% of Chinese Android devices sold do not come with the Goolge Play store installed but rather have ties to dozens of local app store from local service providers. Therefore to get an accurate picture of the Android market, it is more helpful to break out market share by devices which have the Play store and the ones that do not. If we did, then IDC’s, chart would look more like this.

Chart Caveat: Two things about this chart. First I’m making a point not a series of forecasts. I will let my friends at IDC and other firms do the forecasting. Second, the size of the tablet market in 2017 could likely be over 600 million.

This is a more helpful way to look at the data and understand the market share. If I am a developer and I look at this data, then I may be more inclined to say that I should focus on Amazon’s platform vs. Google’s version of Android when it comes to tablets. More importantly I would understand that iOS and Apple’s App store still offers me the greatest total addressable market. China is the wild wild west as I point out and only local devs have a shot there at figuring out their app store mess.

Since Android is not actually a platform, but an enabling technology that allows companies to create platforms, it’s helpful to look at the data in a way that shows the picture as it is. Stating generically “Android market share” does not give an accurate picture to the market which needs the data to make educated decisions.

My goal here is not to be overly negative on Android, but simply to paint a more accurate industry picture.

Android not a platform. Interesting. It does explain all the scurrying around by Amazon, Google, Microsoft, HP, LG, and Samsung to secure more integration, to build a platform. Like Apple.

yeah, thats at least how I see it. How its being forked and used as an enabler for platforms is very interesting. I inline linked to some articles in this post where I break that down further.

Actually I forgot to link to this one. This is where I break it down.

http://techpinions.com/toward-a-more-informed-discussion-on-android/13093

Same as WebKit is not a platform. Android and WebKit are both platform components that manufacturers can use when building their own platforms. Google used Apple WebKit to make Android and Chrome, but that does not mean Android and Chrome are Apple products or benefit Apple in any way. Amazon used Android to make Kindle, but that does not mean Kindle is a Google product or benefits Google in any way. And software developers cannot target all WebKit-based or all Android-based products as one platform. You can make a Web app for Safari that doesn’t run in Chrome — both WebKit-based. You can make an app for Samsung Galaxy 3 that doesn’t run on a single Motorola phone — both Android-based. There is not even a guarantee that your Samsung Android-based app runs on all Samsung Android-based phones!

The Apple equivalent of Android is not iOS — it is Darwin. Darwin is an open source component that Apple uses to build both iOS and Mac OS X platforms. Mac apps don’t run on iOS devices just because they are both Darwin-based. Amazon uses Android to build their Kindle platform. Apps that run on Kindle don’t run on Galaxy Tab just because they are both Android-based.

So unless the definition of platform is being arbitrarily changed, no Android is not a platform. Today’s platforms are iOS, Mac, iPod, PlayStation, Wii, Windows 8, Windows RT, Windows Vista/7, Windows XP, Xbox, Kindle, Nexus, Galaxy. By looking at this list, you can see right away that Microsoft has too many platforms, leading to their chicken/egg problem of very few apps for Windows 8 and Windows RT. You can see why a lot of Android-based software development is targeted only at Kindle, Nexus, or Galaxy, which combined are relatively small, maybe 10% of all Android-based devices, which is why it is had to make money with Androidbased development. You can see what is really happening. You don’t end up mystified as to why iOS has the most developer support because you can see it is by far the largest platform. Reality.

I don’t want to broaden this too far. Cus’ I have no idea what I’m talking about. Wikipedia does define operating systems as platforms, however.

My interest is in a nontech definition of a platform, as in a business platform. I’m just going to glump this info below. What intrigues me is the idea that a platform, say a political platform, can a logical articulation on which a community can gather and build.

Platform businesses have a number of attributes in common. These include:

Platforms are open. A “proprietary platform” isn’t.

Platforms can be built upon.

No one should have to ask you permission or pay you money to start building on your platform (although platforms can ultimately be both commercial and non-commercial).

Platforms attract communities of builders. To thrive, these communities should be managed and nurtured.

Building a community around your platform enables you to build your business more effectively with the enthusiastic help of customers, suppliers and partners.

Platforms scale efficiently. Self-service access and low barriers to entry are cornerstones of this.

Platforms do not discriminate between small and large builders. Some platforms enable small builders to compete on a level playing field and disrupt incumbent businesses.

A platform is a two-way contract between the platform provider and the builders that utilize the platform.

Platforms can be managed in a way that encourages positive outcomes for the platform business as well as customers and builders.

Platforms can facilitate unexpected outcomes. This is usually a good thing, if it’s managed properly.

Source: Platform Associates

If operating systems and platforms were the same, there would only be one term, the other would fade away and no longer be used.

Operating system has meant very different things over the years. By some definitions, Darwin is Apple’s operating system. By other definitions, OS X is Apple’s operating system. By other definitions, Apple has 2 operating systems: iOS and Mac OS (called OS X today, but referring to something different than what OS X referred to from 1999–2008, which was just the core part that was put under Mac OS in 1999 and put under iOS in 2007.) By some definitions, Apple’s operating system is xnu, just the kernel of Darwin.

So no, operating system does not equal platform. The fact that Wikipedia says so only strengthens my position.

Platforms is also very generic. For music and movie producers, iTunes is Apple’s platform, but for software developers, Apple’s platforms are iOS and Mac OS X. In the context of this article, we are talking about the latter kind of platform: a group of users that a software app or hardware accessory developer can target as one. An iOS app runs on all iOS devices; a Mac app runs on all Mac OS X devices; a Wii app runs on all Wii’s.

The Web is a platform for basic Web pages (not really for apps yet, unfortunately) but is not an operating system. Java is a platform but not an operating system.

All good. Just to clarify. I didn’t say all platforms were OSes, but that all OSes were platforms.

There are accepted definitions here. The heart of an operating system is the kernel. Darwin, a modified BSD Unix kernel, serves the purpose for OS X and iOS. Android’s kernel is modified Linux. But Android, like iOS or OS X or Windows, is a full operating system, with a file system, a program scheduler, I/O, and a user interface (or actually, a number of UIs, depending on version.) Compatibility of of applications among OS versions is generally determined at the API level–a program will only run on a given OS instance if it uses only the APIs supported by the OS. iOS and OS X have a fair number of APIs in common, but not nearly enough to support interoperation (not to mention the fact that iOS runs on ARM processors and OS X on Intel x86.

On the other hand, you can run many stock Android programs on a Kindle Fire provided they are written for the version of android on which Fire’s software is based.

The distribution channel fragmentation is just another dimension in the Android fragmentation story.

It should actually be the one that generates the least amount of headache during the development process, proportional with the code and design changes needed.

I can see how it complicates maintenance and support, but it’s an ordinary cost of doing business. Selling through multiple distributors never broke anyone’s back.

I agree with that in respect to Amazon but not to China. The China one is a mess. I constantly hear horror stories of devs from that market.

Also interestingly we are getting quite a bit of data now that much of those white box cheap Android tabs in china are just being used as media players (video). So one could argue they aren’t even really using the apps or computing elements that may benefit a app dev business model.

The Android-based tablets are all media players like iPod. They run phone-based operating systems, phone-sized apps, music, movies, book reader, Web browser at roughly a $200 price point. Just like an iPod. They should be compared in sales to iPods. When you do that, a picture appears that shows Apple media players are optimized primarily for music, Amazon’s primarily for books, and everyone else’s for movies. Which of course makes perfect sense. That shows the heritage of Apple and Amazon — music and books, respectively — when they started making media players. That shows how everyone else came late and had cheap enough large screens to sell primarily as large-screen movie players. In a sense, an Android-based tablet is the true “iPod video” that Apple never did. iPods continue to be music players that can also play video as a secondary feature.

iPad, on the other hand, is a PC. The one and only successful tablet PC thus far after about 20 years of trying. iPad runs the core OS from a high-end PC workstation, and its primary function is to run full-size native C/C++ apps. Full-size is 1024×768 at 1x or Retina 2x resolution — PC size. Native C/C++ apps are also found on Mac, Windows, and game consoles — PC apps. Not Java like Android-based devices, but C like PC’s. My iPad replaced one of my Macs and I run the same apps on the iPad that I used to run on that Mac. An iPad is a Mac with the mouse user interface and mouse developer interface replaced by touch user interface and touch developer interface and the security locked down an extra level for even more ease of use and reliability.

I can work all day on my iPad at my job, and often do. I have yet to see anyone work all day on a Kindle Fire. I have yet to even see a Samsung tablet being used. It is no small thing because the money that paid for my iPad came out of what used to be a 2-Mac budget but is now a 1 Mac and 1 iPad budget. So iPad did not grow my technology budget to add touch and 10 hour PC mobility, it shrank it. For others, they are replacing a Windows PC purchase with iPad, and getting a cheaper, better, easier to use, longer battery life PC. And the iPad apps are cheaper than Mac apps and much cheaper than Windows apps. On the other hand, Android-based tablets are considered expensive at $200 because they don’t replace a $400–$800 Windows PC purchase. You have to find additional budget for them. They are Windows PC accessories.

So this is just more of the same pro-generic propaganda that we have always seen. A little know fact is that Mac developers have always made the same or more money than Windows developers, Adobe has always made roughly 50:50 on each platform. That is because the users who are actively engaged in each platform is about the same. But IT analysts lump in Windows-based point-of-sale systems, bank machines, kiosks, typewriters, and even servers to present the picture that Windows has 90% of a meta PC market. That is a big part if why so many Windows developers and manufacturers went bust. They built for a phantom user base, and then sold into a market that was really only 10% that size — the engaged users who were running Windows and buying apps and hardware accessories.

So the decoding you are doing here is an age-old tradition. I’m an Apple user since the 80’s. I have seen this all before. The Mac was not counted as a PC by many IT analysts until it adopted Intel processors in 2005/2006, even though at that point, every PC they had counted for 15 years was a Mac clone. There are a lot of IT analysts with a vested interest in the generic market, which primarily makes sales by convincing naive users that Windows is the same as Mac, Kindle Fire is the same as iPad, Galaxy phones are the same as iPhone. They piggyback on the demand Apple creates while simultaneously minimizing Apple at every turn. A smart reader has to decode IT analysis and unwrap that bias.

Of course selling through multiple distribution channels has broken backs. That was the basis upon which we got 5 giant record companies and 5 giant movie companies in the 20th century. That created only 5 distribution channels out of an amalgam of hundreds of thousands of retailers. It saved many producers from going out of business. Hip little independent record companies did not sell to giant record companies because they wanted to — the multiple distribution channels broke their backs.

Apple has created a system where there is only one distribution channel, so that a 1-person app developer can function on equal distribution terms with giant companies. The distribution channel does not break any backs and force an intermediary set of giant distributors to appear to gobble everything up until the distribution channels are united.

If you develop an Android-based app, to reach all of the devices, you would have to create a business agreement with over 10,000 individual retailers. To reach all Apple devices, you make one agreement with one retailer.

As a consumer, you can see an app running on a friend’s Android-based device, rush out and buy an Android-based phone, and never be able to find that app for purchase on your new phone because it is wired into a different retailer.

Android-based phone making is a non-profit for everybody other than Samsung. Android-based app development is a non-profit for almost everybody. Unprofitable business equals broken back.

Ben, do we have any correlation between shipments and sales?

No since they don’t report that way. The best we can do is get channel sales from our friends at NPD but in the case of Amazon its not complete because of online.

Besides looking at it the way I am, the other nut that needs to be cracked is what an activation is. I’ve heard from numerous sources that when an android device is updated, that it could be counted as another activation. Thus the same device can be counted numerous times. I’m still trying to validate this but its an interesting talking point.

Apple open source code (WebKit) will be installed on way more devices than Android open source code. WebKit is on all Apple devices, Android-based devices, BlackBerry devices, most Nokia devices, all Chrome OS -based devices. as well as PC installations of Chrome and Adobe Creative Suite. Lumping all of these devices into “the WebKit platform” is just as unimportant a sales metric as “the Android platform.” Samsung is the only one making any money from Android, and they are also the manufacturer that most-closely copied Apple. Did people buy a Galaxy phone to get Android features, or did they buy it to get iPhone features?

When you break out the numbers by manufacturer, comparing Apple, Samsung, Nokia, Motorola, LG, Sony, HTC then you see the actual phone and tablet markets, and suddenly you understand why Apple has all the influence. And you have to compare sold versus sold. This is basic science.

So we are just witnessing a propaganda campaign by the generic tech industry. Regular people think Apple’s sales and market share have crashed when both of those metrics have only ever gone up. It is the combined Android market share that fell last quarter, and Android-based devices have gone even further downmarket and become even more unprofitable.

By 2017 there just might be a Samsung fork of Android too. As a stepping stone on the way to replacing Android with Tizen as Samsung’s mobile OS of choice. Either way, Sammy may not be running the generic Google release in 5 years.

And then there’s the possibility of a Motorola fork as well. And maybe that’s the reason why Rubin stepped aside. Because he wanted Android to be one-size-fits-all and the rest of Google management wanted Motorola to get the latest features first. To give them an advantage over other Android handset makers (especially Samsung with their own optimized Android fork.) To help an recoup that disastrous $12.5 billion investment in useless patents.

The guy who replaced Rubin is the Chrome chief. Google is shipping its own Chrome hardware already. Motorola may become the Chrome hardware maker, making Chrome phones and tablets.

Android apps are based on stolen Oracle/Sun intellectual property. Oracle wants them impounded and destroyed. Eventually it will happen because otherwise, all copyright law is affected negatively. Google erased “© Sun” from the Java specification (a giant document that took Sun 10 years and millions of dollars to write) and put on “© Google” and continued on their way. Ultimately, that can’t stand.

So I expect this leadership change is part of Google focusing further on Chrome OS, which runs a legal kind of app. With proprietary hardware, Chrome can easily outcompete Nexus.

John, you sing sweet music and I am madly penning the notes. And speaking of pen, that is where the Google top brass needs to be asap, IMun-HO.

addendum

and regarding further below “. . . should have done a big-screen Zune with the movies from Xbox, but since Apple didn’t do a big-screen iPod, Microsoft never thought of it.” Just about gagged on my milk and cookies.

There is an opera in the tales of Apple and MicroSoft. I could see The Magic Flute meets Punch and Judy.

This TP edition has been one of the most instructive and entertaining pieces of tech journalisms and commentary in a long time.

Ben, very helpful insight. The other factor that struck me is that the total number of tablets is increasing and thus iOS numbers which represent the major profit of the tablet market are increasing. It might be argued in light of what you have revealed in these numbers that Apples’ influence in this market may be expected to increase.

It is iPad’s influence on the PC market that is interesting. The other tablets are just media players, but iPad is a PC. From 2006–2010 the Intel Mac took almost the whole high-end of PC’s and drove Windows PC’s down to a $400 average sales price, where iPad is currently murdering it. That is why Windows 8 is a tablet PC system. That is the basis of competition now in the low-end PC market. Low-end PC’s are tablet PC’s now, and high-end PC’s are workstations.

iPad versus Windows 8 is the story of 2013. Apple supplanting Microsoft as the center of PC computing is the story of 2006–2016. So is Apple supplanting Nokia/BlackBerry as the center of phones.

A bunch of $200 media players from hundreds of manufacturers is an echo of the iPod market. Boring. Notice the leaders in media players are Apple, Amazon, and Google — iTunes, Kindle, and Play are the reason because media players need content stores. Microsoft has something similar with Live, but no media player devices, so no media player sales since they retired Zune. They should have done a big-screen Zune with the movies from Xbox, but since Apple didn’t do a big-screen iPod, Microsoft never thought of it.

Any idea what is in the green “Other” category? It seems way too big for just the Fisher Price kid tablets.

More and more Chinese tablets are coming with the Play Store nowadays. And as long as you buy a tablet with Android, Google profits in market share statistics. And even if you are using a different apps store than the Play Store, Google profits via AdMob and usage statistics/data mining. And as long as this app store (not thousands, not hundreds, there are more like 5 or 6 important ones) or website, and even blog sites, are not pirating paid apps, the developer will benefit via the ads/ad network he is using.

It’s hard to compare Apple with Google; their business models are completely different. But to dismiss Google’s take on mobiles/OSes would be foolish. Especially considering that their business model has never really failed them; just look at their stock. But time will tell.

Do they? The way Google is NOT present in China?

Has no relevance to any of the points I metioned. IMO.

Reading through the comments and article again, Samsung surfaces as a big X factor. It’s noted below that it might fork Android. Maybe it just sticks a fork in Android and moves off entirely to its own OS. Samsung owes Android nothing; it’s free, right? And Samsung wants to be Apple, not Sony and certainly not a Google lackey.

I agree on those points. I think Samsung must either fork Android or do something of their own entirely if they want to continue to attempt to have a premium business. You are not in control of your own future when you ship the same software as your competitors.

Can Samsung search and ads be far behind? It’s put out a Passbook app. We can’t all live upstream, but I bet Samsung thinks it can. Tiger by the tail?

@Ben wrote, “This is because Android can be taken and forked, to the chagrin of Google…”

An interesting thought experiment — not too different from seeing what insights you get by denying one of the axioms of Euclidian geometry — is to see what happens if you’re wrong, if Google really is quite happy to see Android become universal and totally out of its control.

In this environment, the OS would be so completely commoditized that its value was effectively zero. Any commodity engineering shop — which Ben Evans has documented very well — could bang out a tablet by making a couple of phone calls for screens, plastic moldings and generic circuit boards; as a result the hardware would cost very little, too, maybe $100 for what would have amazed anybody back just ten years ago at $2000.

Now, the value is purely for the producers of information/entertainment. (An aside: loved seeing the McLuhan quote, “Anyone who tries to make a distinction between education and entertainment doesn’t know the first thing about either.”) Those content providers need a way for people to find and pay for their work; today, with the exception of a very few paywalls that are working well, means advertising—advertising their site and running ads for products to pay for the sites.

Of course, it is advertising on which Google is nearing a complete monopoly.

No, not in China or India, and non-™ OASP Android might enable other services to get established in markets in a way that’ll make it harder for Google to compete later. But in truth, Google has probably written off any hope of doing business in the People’s Republic, as the government wants total control of information (especially political content), and near-total economic control. So not much loss there. But at least, in the US, Microsoft is denied the opportunity to profit from distributing hardware with Bing as the default search engine and Apple’s iAd continues to go nowhere.

So even an out-of-control Android world leaves Google MORE effectively in control of its monopoly, of the only way they’ve EVER made money.

I don’t know what the Rubin departure means for this Gedankenexperiment. It could be that Google assumes it’s done all it needs to demolish Microsoft as a mobile competitor (the original rationale for Android), and that it’s time to let the OHA go its own way, while Google switches to promoting Chrome as the end-all, be-all way of accessing everything through the Google portal. But that would correlate nicely with my idea, maybe accelerate it.

(PS: just saw the Quartz thoughts and it crystallized the idea that next up is for Google to submit Android as a W3C spec — that ANY party can deliver content thru Android applets without any royalties — as a way of attacking the Windows and iOS abilities to deliver great apps only through their platforms. That’d be PERFECTLY consonant with their typical disruptive innovation approach.)

Still, I’m not seeing a scenario in which Google attempts to take Android back under its exclusive control. Like so many markets where Google first scorches, and then salts the earth so nothing else can grow (be monetized except by ads), Android has done its job and Google is moving on.

What you bring up goes to the heart of the question of why Android exists in the first place. I firmly believe that Android was conceived as a disruptor play in an attempt to force a commodity hardware business. From close OEM relationships we have, I know google always encouraged their partners to get the costs down, down, down. Despite their partners asking for ways they can get better margins or make money on things other than hardware, since making money on hardware alone is a not a business many want to be in.

I am not sure Google anticipated that partners would want an upstream play rather than a downstream play. But I am convinced Google wanted a commodity business related to hardware because its was better for their services side of the business.

I fall into the camp that Google didn’t care at all to make money from Android, they simply wanted to make sure their search got on as many mobile devices as possible and for that they believed forcing a commodity market using Android as the vehicle to do so would take it down that path.

This is not happening and their partners are having trouble making money. Just like MSFT, I expect google to lose more Android partners.

exactly, and as proof we know that Google pays Apple – it’s supposed OS rival – a lot each year to remain the default search app for iOS.

Walt, is there anyway that Apple could do to ‘search and advertising’ to disrupt Google, as Google and Amazon have done in disruption of other’s business models; i.e., along the way of “free” or next to free? With the cash it has on hand, Apple could afford to do it at break-even, or even at a loss. There are other models out there that Apple might buy or bring into its fold namely Start Page, DuckDuckGo, and dare I add, Bing and Yahoo. I’d forgotten about iAd but with profit taken out of the scenario, Apple might find it possible to think outside the box. Surely it would be to both Apple’s and MicroSoft’s advantage to work on some disruptive line together. My enemy’s enemy is my friend sort of stratagem.

I’m not aware of a major success that has resulted recently from a frontal assault. Google’s Android ascendancy was based on disrupting the value stack of Microsoft’s OS not by giving it away (as it appears), but from monetizing it with ads (which, TBH, hasn’t actually worked THAT well).

Apple’s recent big hits all came after Jobs told the faithful two decades ago, to get over the fact that they lost the PC wars, and to go do something great in new markets. Only lately are they doing ANYTHING like direct competition with Microsoft, in announcing the 128GB iPad.

So no, a frontal assault on Google, pouring billions into destroying another’s business, with no hope from creating a new market, seems fruitless — mean-spirited, too, which is a distraction of what they claim to, and mostly actually do, do.

The only areas I can see Apple leveraging are in first-class hardware (where they stand clearly ahead of all but a few Android lines) and online services: better synchronizing, better usability, easier access, bypassing the generic, and ad-cluttered web. Those will be challenges enough; Apple’s efforts with maps and Siri are not exactly moving everybody to switch to them.

“So no, a frontal assault on Google, pouring billions into destroying another’s business, with no hope from creating a new market, seems fruitless — mean-spirited, too, which is a distraction of what they claim to, and mostly actually do, do.”

In my heart of hearts I agree. Apple is not a mean spirited or desperate company but it sure must rankle when Google, whom Apple invited to its board, pulled some pretty cranky low punches. “Do no evil” is truly more Apple’s style, and this is mostly understood and appreciated by its faithful followers, I suspect. An Apple wristwatch, a low priced iPhone for lower end users with fewer high-tech needs would open the doors even in NA and Europe as should across China, India and poorer markets. (I know I prefer my iPad in this regard and would jump at an iPhone less featured.) I’m sure Apple had all this in its plans and scenarios long ago having anticipated the trends of today. Apple is a mind open, mysterious yet not devious, whilst so obviously desperate are Samsung’s and Google’s frantic caldrons of toil and trouble to be in this game.

As always, your thoughts help sweep aways the cobwebs of confusion. 🙂

These companies are operated by human beings, but ones with lots of experience in staying focused.

“Don’t get mad; get even” doesn’t capture it; Scoop Nisker’s “if you don’t like the news, make some of your own” comes a bit closer.

Exactly, M French

–

Wearied novice

Occasions to the dark side

Trials of sentience

IDC gets away with not being fact checked for its prior years’ predictions, which have often been poor. they have always been “optimistic” about MS in particular (one of their “research” clients i bet). now their 2017 estimate of a Windows RT/full OS tablet share of almost 10% is laughable. RT won’t be around at all by then, and full Windows tablets will be lucky to ever get more than 1% of the market.

Everything on that chart, except the area marked “iOS” is made up numbers. Nobody actually reports sales for android.

Or put another way, this is just wishful thinking from android fans, and the professional liars at the IDC.

You may be young, but if you watch IDC for any period of time, all of their predicitions are wrong.

What they claim and predict is what they are paid to claim and predict by the people purchasing the legitimacy of their “analysis” which comes to pre-ordained conclusions.

This is my first time pay a quick visit at here and i am really happy to read everthing at one place

You have noted very interesting details! ps decent web site.

Definitely what a great blog and instructive posts I definitely will bookmark your site.All the Best!

https://indianpharmacy.shop/# online pharmacy india

Online medicine order

medication from mexico pharmacy: mexico drug stores pharmacies – п»їbest mexican online pharmacies

canada pharmacy world Pharmacies in Canada that ship to the US canadian drugs pharmacy canadianpharmacy.pro

http://mexicanpharmacy.win/# mexican rx online mexicanpharmacy.win

world pharmacy india

https://canadianpharmacy.pro/# best canadian pharmacy canadianpharmacy.pro

http://mexicanpharmacy.win/# buying prescription drugs in mexico online mexicanpharmacy.win

Online medicine order

canadian discount pharmacy Cheapest drug prices Canada best rated canadian pharmacy canadianpharmacy.pro

https://mexicanpharmacy.win/# mexico drug stores pharmacies mexicanpharmacy.win

https://indianpharmacy.shop/# indianpharmacy com indianpharmacy.shop

top online pharmacy india

mexican pharmacy buying prescription drugs in mexico online mexico pharmacy mexicanpharmacy.win

https://mexicanpharmacy.win/# best online pharmacies in mexico mexicanpharmacy.win

http://mexicanpharmacy.win/# buying from online mexican pharmacy mexicanpharmacy.win

cheapest online pharmacy india

india pharmacy Cheapest online pharmacy india online pharmacy indianpharmacy.shop

https://mexicanpharmacy.win/# mexico drug stores pharmacies mexicanpharmacy.win

http://indianpharmacy.shop/# indianpharmacy com indianpharmacy.shop

indian pharmacy paypal

https://canadianpharmacy.pro/# canada drugs reviews canadianpharmacy.pro

canadian pharmacy ltd Pharmacies in Canada that ship to the US canada pharmacy online legit canadianpharmacy.pro

http://mexicanpharmacy.win/# buying from online mexican pharmacy mexicanpharmacy.win

https://mexicanpharmacy.win/# mexican pharmacy mexicanpharmacy.win

pharmacy website india

ed meds online canada canadian king pharmacy legitimate canadian pharmacy canadianpharmacy.pro

http://canadianpharmacy.pro/# ed drugs online from canada canadianpharmacy.pro

Viagra vente libre allemagne viagra sans ordonnance Viagra sans ordonnance livraison 24h

http://cialissansordonnance.shop/# Pharmacie en ligne sans ordonnance

Pharmacie en ligne fiable: achat kamagra – Pharmacie en ligne fiable

Sildenafil teva 100 mg sans ordonnance: viagra sans ordonnance – Sildenafil teva 100 mg sans ordonnance

http://viagrasansordonnance.pro/# Viagra homme prix en pharmacie

Pharmacie en ligne livraison 24h

http://viagrasansordonnance.pro/# Sildénafil 100 mg sans ordonnance

Pharmacie en ligne livraison 24h kamagra en ligne Pharmacie en ligne pas cher

Pharmacie en ligne livraison gratuite: levitrasansordonnance.pro – pharmacie ouverte 24/24

http://acheterkamagra.pro/# Pharmacie en ligne pas cher

Pharmacie en ligne livraison gratuite acheter mГ©dicaments Г l’Г©tranger п»їpharmacie en ligne

pharmacie ouverte: Pharmacie en ligne France – Pharmacie en ligne fiable

https://viagrasansordonnance.pro/# Sildénafil 100 mg prix en pharmacie en France

https://viagrasansordonnance.pro/# Viagra homme prix en pharmacie

acheter mГ©dicaments Г l’Г©tranger

http://levitrasansordonnance.pro/# Pharmacies en ligne certifiées

Viagra femme sans ordonnance 24h viagrasansordonnance.pro SildГ©nafil 100 mg sans ordonnance

Pharmacie en ligne livraison gratuite: Levitra acheter – п»їpharmacie en ligne

http://viagrasansordonnance.pro/# Viagra vente libre pays

Pharmacie en ligne livraison gratuite achat kamagra Pharmacie en ligne livraison gratuite

https://cialissansordonnance.shop/# Pharmacie en ligne fiable

how to buy cheap clomid now get clomid tablets clomid no prescription

amoxicillin 500 tablet: can we buy amoxcillin 500mg on ebay without prescription – amoxicillin without a prescription

http://azithromycin.bid/# buy zithromax 500mg online

cost cheap clomid no prescription: can i get generic clomid no prescription – cost of clomid now

iv prednisone prednisone 20 mg prednisone buy no prescription

http://ivermectin.store/# ivermectin online

cost of stromectol medication: ivermectin uk coronavirus – order stromectol

amoxicillin azithromycin price of amoxicillin without insurance can i buy amoxicillin over the counter

https://amoxicillin.bid/# buy amoxicillin from canada

can you get clomid tablets: can you get generic clomid tablets – where to buy generic clomid without prescription

ivermectin oral ivermectin 1 topical cream ivermectin lotion cost

https://clomiphene.icu/# cost generic clomid without insurance

can i get generic clomid without dr prescription: where can i buy clomid without rx – cost cheap clomid without prescription

https://ivermectin.store/# buy ivermectin nz

http://clomiphene.icu/# how to buy cheap clomid price

how to buy clomid online where can i buy clomid without rx can i order generic clomid without rx

buy prednisone from india: mail order prednisone – 80 mg prednisone daily

https://azithromycin.bid/# generic zithromax online paypal

amoxicillin over counter: amoxicillin generic – amoxicillin 500mg for sale uk

order generic clomid without rx where buy generic clomid online cost of clomid

https://azithromycin.bid/# zithromax generic price

ivermectin price uk: buy stromectol online – purchase ivermectin

prednisone 20mg prescription cost prednisone 3 tablets daily prednisone 5 mg brand name

http://amoxicillin.bid/# amoxicillin 875 mg tablet

where can i buy amoxicillin without prec: buy amoxicillin online cheap – amoxicillin order online no prescription

http://amoxicillin.bid/# amoxicillin generic brand

canadian pharmacy online Canadian Pharmacy canadian pharmacy world canadianpharm.store

indian pharmacy: Indian pharmacy to USA – pharmacy website india indianpharm.store

http://mexicanpharm.shop/# mexican rx online mexicanpharm.shop

п»їbest mexican online pharmacies: Online Pharmacies in Mexico – mexico pharmacies prescription drugs mexicanpharm.shop

Online medicine home delivery international medicine delivery from india best online pharmacy india indianpharm.store

indian pharmacy: Indian pharmacy to USA – reputable indian pharmacies indianpharm.store

https://mexicanpharm.shop/# medicine in mexico pharmacies mexicanpharm.shop

https://canadianpharm.store/# canada discount pharmacy canadianpharm.store

pharmacy website india: Indian pharmacy to USA – best online pharmacy india indianpharm.store

reputable indian online pharmacy online shopping pharmacy india reputable indian pharmacies indianpharm.store

http://indianpharm.store/# reputable indian pharmacies indianpharm.store

safe canadian pharmacy: Canadian International Pharmacy – canadianpharmacymeds com canadianpharm.store

mexican rx online Online Mexican pharmacy mexico pharmacy mexicanpharm.shop

http://canadianpharm.store/# legitimate canadian mail order pharmacy canadianpharm.store

trusted canadian pharmacy: canadian pharmacy in canada – canadian online pharmacy canadianpharm.store

purple pharmacy mexico price list: pharmacies in mexico that ship to usa – pharmacies in mexico that ship to usa mexicanpharm.shop

http://indianpharm.store/# top 10 online pharmacy in india indianpharm.store

reputable indian online pharmacy order medicine from india to usa top 10 online pharmacy in india indianpharm.store

buy medicines online in india: order medicine from india to usa – indian pharmacy indianpharm.store

http://canadianpharm.store/# legitimate canadian online pharmacies canadianpharm.store

http://canadianpharm.store/# canadian compounding pharmacy canadianpharm.store

canadian pharmacy online ship to usa: Pharmacies in Canada that ship to the US – canadian pharmacy prices canadianpharm.store

http://mexicanpharm.shop/# reputable mexican pharmacies online mexicanpharm.shop

mexico pharmacy: Certified Pharmacy from Mexico – mexican border pharmacies shipping to usa mexicanpharm.shop

reputable indian online pharmacy Indian pharmacy to USA Online medicine order indianpharm.store

https://indianpharm.store/# best india pharmacy indianpharm.store

top 10 online pharmacy in india: order medicine from india to usa – buy prescription drugs from india indianpharm.store

mexico pharmacy: Online Pharmacies in Mexico – mexico pharmacies prescription drugs mexicanpharm.shop

https://mexicanpharm.shop/# best online pharmacies in mexico mexicanpharm.shop

http://indianpharm.store/# indian pharmacy indianpharm.store

best rated canadian pharmacy Pharmacies in Canada that ship to the US canadian pharmacy scam canadianpharm.store

mexican rx online: Certified Pharmacy from Mexico – mexico pharmacies prescription drugs mexicanpharm.shop

https://canadianpharm.store/# my canadian pharmacy canadianpharm.store

top 10 pharmacies in india: international medicine delivery from india – best india pharmacy indianpharm.store

mexican mail order pharmacies Online Mexican pharmacy pharmacies in mexico that ship to usa mexicanpharm.shop

canadian drugstore online: canadian pharmacy online store – canadian compounding pharmacy canadianpharm.store

https://canadianpharm.store/# canadian online pharmacy reviews canadianpharm.store

buy prescription drugs from india order medicine from india to usa indian pharmacy online indianpharm.store

Online medicine order: india pharmacy – indian pharmacy paypal indianpharm.store

http://canadianpharm.store/# canadian drugs pharmacy canadianpharm.store

https://mexicanpharm.shop/# pharmacies in mexico that ship to usa mexicanpharm.shop

mexican border pharmacies shipping to usa Online Pharmacies in Mexico buying prescription drugs in mexico mexicanpharm.shop

reputable online pharmacy canadian online pharmacy no prescription pharmacy drugstore online

canadian pharmacy world: internet pharmacies – universal canadian pharmacy

https://canadadrugs.pro/# canadian pharmacy generic

your discount pharmacy: rx online no prior prescription – pharmacy without dr prescriptions

price prescriptions prescriptions canada canada drugs without prescription

canadian drug store legit: reliable online pharmacies – thecanadianpharmacy com

meds without prescription: most trusted canadian pharmacy – onlinepharmaciescanada com

https://canadadrugs.pro/# canadian pharmacies prices

usa online pharmacy: prescription without a doctors prescription – online pharmacy canada

cheap prescription drugs canada pharmacies online pharmacy northeast discount pharmacy

http://canadadrugs.pro/# online prescription drugs

online pharmacies: canadian pharmaceuticals for usa sales – pharmacy without dr prescriptions

testosterone canadian pharmacy discount canadian drugs global pharmacy plus canada

prescription drug price comparison: prescriptions online – my canadian drugstore

http://canadadrugs.pro/# canadian online pharmacy reviews

canadian pharmacy advair: reputable online canadian pharmacy – mexican drug pharmacy

canadian mail order drug companies: reputable online canadian pharmacies – prescription drugs without prior prescription

http://canadadrugs.pro/# canada rx

non prescription drugs prescriptions from canada without prescription drugs without doctor approval

global pharmacy canada: top mail order pharmacies – online ed drugs no prescription

https://canadadrugs.pro/# prescription drug prices

reliable online canadian pharmacy: canada rx – online drugstore service canada

list of legitimate canadian pharmacies: rx canada – canadian pharmacy cialis cheap

http://canadadrugs.pro/# discount mail order pharmacy

canadian mail order pharmacy: androgel canadian pharmacy – online canadian pharcharmy

https://canadadrugs.pro/# best non prescription online pharmacies

canadapharmacyonline.com: legal canadian prescription drugs online – pharmacies online

online ed medication no prescription: overseas pharmacy – cheap canadian drugs

https://canadadrugs.pro/# canadian mail order drugs

online meds without presxription: canadian neighborhood pharmacy – mexican border pharmacies shipping to usa

https://canadadrugs.pro/# canadian prescriptions online

canadian pharmacy for sildenafil: online pharmacies reviews – canadian pharmacy cialis cheap

pharmacies with no prescription canadian pharmacy advair best online pharmacies without prescription

http://canadadrugs.pro/# mail order pharmacy

prescription without a doctor’s prescription: online medications – discount prescription drug

indian pharmacy paypal indian pharmacy online indianpharmacy com

http://medicinefromindia.store/# indian pharmacies safe

mexico pharmacies prescription drugs mexico pharmacy mexico drug stores pharmacies

https://medicinefromindia.store/# п»їlegitimate online pharmacies india

http://certifiedpharmacymexico.pro/# mexican drugstore online

reputable mexican pharmacies online: mexican border pharmacies shipping to usa – reputable mexican pharmacies online

indian pharmacy paypal top online pharmacy india best online pharmacy india

https://medicinefromindia.store/# india pharmacy mail order

canadian pharmacy near me canadian pharmacy 24h com canada ed drugs

https://medicinefromindia.store/# best online pharmacy india

meds online without doctor prescription buy prescription drugs without doctor buy prescription drugs online

canadian pharmacy prices: best rated canadian pharmacy – canadian pharmacy phone number

http://medicinefromindia.store/# india pharmacy mail order

Online medicine order: online shopping pharmacy india – mail order pharmacy india

http://certifiedpharmacymexico.pro/# mexican border pharmacies shipping to usa

legal to buy prescription drugs from canada cheap cialis prescription drugs canada buy online

https://canadianinternationalpharmacy.pro/# best canadian pharmacy to order from

mexico pharmacy mexico pharmacies prescription drugs mexico drug stores pharmacies

mail order pharmacy india: best india pharmacy – online pharmacy india

http://edwithoutdoctorprescription.pro/# prescription meds without the prescriptions

rate canadian pharmacies: canadian pharmacy 365 – pharmacy wholesalers canada

https://certifiedpharmacymexico.pro/# mexican online pharmacies prescription drugs

https://medicinefromindia.store/# online shopping pharmacy india

https://canadianinternationalpharmacy.pro/# trustworthy canadian pharmacy

top 10 online pharmacy in india top 10 pharmacies in india best online pharmacy india

world pharmacy india: indianpharmacy com – india pharmacy

http://medicinefromindia.store/# reputable indian pharmacies

cheapest online pharmacy india best india pharmacy online pharmacy india

http://certifiedpharmacymexico.pro/# buying from online mexican pharmacy

http://canadianinternationalpharmacy.pro/# reputable canadian pharmacy

non prescription ed drugs ed pills without doctor prescription viagra without doctor prescription

canada drugs online: canadian pharmacy – canadian pharmacy

http://certifiedpharmacymexico.pro/# mexican mail order pharmacies

https://medicinefromindia.store/# buy medicines online in india

new ed treatments erectile dysfunction medicines ed medications online

https://edwithoutdoctorprescription.pro/# prescription drugs

indianpharmacy com best online pharmacy india buy medicines online in india

http://medicinefromindia.store/# india pharmacy

https://medicinefromindia.store/# top 10 online pharmacy in india

online pharmacy india

https://certifiedpharmacymexico.pro/# buying prescription drugs in mexico online

purple pharmacy mexico price list: mexican pharmaceuticals online – buying from online mexican pharmacy

best india pharmacy indianpharmacy com india pharmacy

https://canadianinternationalpharmacy.pro/# safe online pharmacies in canada

canadian pharmacy online reviews canadian pharmacy 24 com canadian online pharmacy reviews

http://edpill.cheap/# male ed pills

erection pills viagra online treatment for ed erection pills viagra online

http://canadianinternationalpharmacy.pro/# online canadian pharmacy review

natural ed medications: herbal ed treatment – ed treatment pills

mexico pharmacies prescription drugs mexican rx online mexican pharmacy

mexico drug stores pharmacies reputable mexican pharmacies online medicine in mexico pharmacies

mexican pharmacy mexico drug stores pharmacies mexico drug stores pharmacies

medicine in mexico pharmacies buying prescription drugs in mexico mexican pharmacy

https://mexicanph.com/# buying from online mexican pharmacy

purple pharmacy mexico price list

mexico pharmacies prescription drugs mexican pharmaceuticals online mexico drug stores pharmacies

purple pharmacy mexico price list purple pharmacy mexico price list mexico pharmacy

mexican pharmaceuticals online mexican rx online pharmacies in mexico that ship to usa

https://mexicanph.com/# mexican drugstore online

purple pharmacy mexico price list

buying from online mexican pharmacy mexico pharmacy mexican rx online

mexican border pharmacies shipping to usa medication from mexico pharmacy medication from mexico pharmacy

purple pharmacy mexico price list mexico drug stores pharmacies buying prescription drugs in mexico

mexico pharmacy medicine in mexico pharmacies reputable mexican pharmacies online

http://mexicanph.com/# purple pharmacy mexico price list

mexican rx online

best online pharmacies in mexico mexican border pharmacies shipping to usa mexico drug stores pharmacies

buying prescription drugs in mexico online mexican mail order pharmacies purple pharmacy mexico price list

mexico drug stores pharmacies mexico pharmacies prescription drugs mexican drugstore online

best online pharmacies in mexico mexican online pharmacies prescription drugs mexico pharmacy

https://mexicanph.com/# medicine in mexico pharmacies

medication from mexico pharmacy

mexican mail order pharmacies buying prescription drugs in mexico online mexican online pharmacies prescription drugs

mexican mail order pharmacies mexican pharmaceuticals online reputable mexican pharmacies online

https://mexicanph.com/# mexico drug stores pharmacies

medicine in mexico pharmacies

purple pharmacy mexico price list best mexican online pharmacies mexican drugstore online

best online pharmacies in mexico buying prescription drugs in mexico п»їbest mexican online pharmacies

mexican border pharmacies shipping to usa medication from mexico pharmacy mexican drugstore online

mexican pharmacy medicine in mexico pharmacies mexican rx online

https://mexicanph.shop/# mexico pharmacies prescription drugs

best online pharmacies in mexico

best online pharmacies in mexico mexican drugstore online buying prescription drugs in mexico

mexican pharmacy best mexican online pharmacies mexico pharmacy

п»їbest mexican online pharmacies п»їbest mexican online pharmacies mexico pharmacy

mexico pharmacies prescription drugs medication from mexico pharmacy best mexican online pharmacies

mexican rx online mexican rx online pharmacies in mexico that ship to usa

mexico drug stores pharmacies purple pharmacy mexico price list buying prescription drugs in mexico

mexican rx online pharmacies in mexico that ship to usa medicine in mexico pharmacies

mexican pharmacy pharmacies in mexico that ship to usa mexican pharmacy

mexican online pharmacies prescription drugs mexico drug stores pharmacies mexico drug stores pharmacies

mexican rx online mexico pharmacies prescription drugs mexican pharmacy

purple pharmacy mexico price list mexico drug stores pharmacies pharmacies in mexico that ship to usa

mexican rx online mexican pharmacy reputable mexican pharmacies online

mexican pharmaceuticals online mexican border pharmacies shipping to usa purple pharmacy mexico price list

https://mexicanph.com/# pharmacies in mexico that ship to usa

mexican rx online

mexican rx online mexican rx online mexican drugstore online

best mexican online pharmacies mexico pharmacies prescription drugs mexico drug stores pharmacies

mexico pharmacy mexican online pharmacies prescription drugs mexico drug stores pharmacies

purple pharmacy mexico price list mexico drug stores pharmacies best online pharmacies in mexico

http://mexicanph.com/# purple pharmacy mexico price list

mexican pharmaceuticals online

best mexican online pharmacies mexican online pharmacies prescription drugs mexico pharmacies prescription drugs

mexico drug stores pharmacies buying from online mexican pharmacy mexican online pharmacies prescription drugs

furosemide 100mg: lasix generic name – buy lasix online

lasix generic Buy Lasix lasix online

https://buyprednisone.store/# prednisone otc price

buy liquid ivermectin: ivermectin australia – ivermectin tablet 1mg

amoxicillin 500mg prescription ampicillin amoxicillin ampicillin amoxicillin

lisinopril cheap brand: lisinopril 5mg tabs – lisinopril rx coupon

generic lasix: lasix uses – furosemide 100mg

order amoxicillin 500mg amoxicillin 500 mg brand name buy amoxicillin online uk

ivermectin 6mg dosage: stromectol online pharmacy – buy ivermectin for humans australia

https://furosemide.guru/# furosemida

amoxicillin buy no prescription buy amoxicillin online cheap canadian pharmacy amoxicillin

ivermectin 0.5% lotion: ivermectin uk – buy oral ivermectin

ivermectin generic name ivermectin for humans can you buy stromectol over the counter

https://buyprednisone.store/# 100 mg prednisone daily

ivermectin lice: ivermectin 4 tablets price – ivermectin cream canada cost

zestril 5 mg prices: can i buy lisinopril over the counter in canada – lisinopril 0.5 mg

buy lisinopril online lisinopril price 10 mg lisinopril discount

http://lisinopril.top/# lisinopril 200mg

lisinopril 90 pills cost: zestoretic medication – lisinopril 5 mg medicine

lasix 40 mg Buy Furosemide furosemide 100mg

http://buyprednisone.store/# buy prednisone 20mg without a prescription best price

ivermectin 4 tablets price: ivermectin 8000 mcg – can you buy stromectol over the counter

prednisone 2 mg daily prednisone 300mg 50 mg prednisone canada pharmacy

prednisone 10 mg tablet: buy prednisone online paypal – cost of prednisone in canada

price for 15 prednisone prednisone without prescription medication prednisone 10mg canada

prednisone buying: 100 mg prednisone daily – prednisone best prices

I found post to be good. The shared are greatly appreciated

http://buyprednisone.store/# can i buy prednisone over the counter in usa

buy amoxicillin 500mg online rexall pharmacy amoxicillin 500mg how to get amoxicillin over the counter

amoxicillin 500mg no prescription: generic for amoxicillin – ampicillin amoxicillin

п»їwhere to buy stromectol online: stromectol cost – ivermectin lotion cost

lisinopril 20 mg buy 40 mg lisinopril for sale lisinopril 80mg

amoxicillin 500mg cost: amoxicillin generic brand – amoxicillin buy online canada

http://furosemide.guru/# lasix 100 mg

ivermectin 4000 ivermectin 500ml ivermectin lotion

lisinopril 3.125: lisinopril 10 12.5 mg – lisinopril pills 2.5 mg

http://lisinopril.top/# can i order lisinopril over the counter

prednisone online paypal: buy prednisone no prescription – prednisone 40 mg tablet

amoxicillin 30 capsules price where to buy amoxicillin over the counter amoxil pharmacy

order lisinopril without a prescription: lisinopril generic price comparison – lisinopril coupon

where to buy amoxicillin 500mg without prescription: amoxicillin without rx – where can i get amoxicillin

buy cheap amoxicillin amoxicillin 500 mg price amoxicillin 500mg capsule buy online

http://buyprednisone.store/# prednisone 20 mg tablet price

http://furosemide.guru/# lasix furosemide

lisinopril 40 mg price cost of lisinopril lisinopril 5 mg buy online

zestoretic tabs: lisinopril with out prescription – lisinopril 40 mg pill

amoxicillin buy no prescription: buy amoxicillin 500mg usa – order amoxicillin online uk

online pharmacy india best online pharmacy india buy prescription drugs from india

http://indianph.com/# world pharmacy india

http://indianph.com/# online pharmacy india

indian pharmacies safe

india online pharmacy cheapest online pharmacy india top 10 pharmacies in india

pharmacy website india indian pharmacies safe india online pharmacy

https://indianph.xyz/# indian pharmacy online

india online pharmacy

https://indianph.com/# legitimate online pharmacies india

indianpharmacy com

https://indianph.xyz/# world pharmacy india

top 10 online pharmacy in india mail order pharmacy india best india pharmacy

https://indianph.com/# indian pharmacies safe

mail order pharmacy india

http://cipro.guru/# buy ciprofloxacin

https://nolvadex.guru/# nolvadex during cycle

http://doxycycline.auction/# buy doxycycline without prescription uk

buy diflucan without a prescription: where can i buy over the counter diflucan – diflucan 200 mg

where to buy diflucan otc generic diflucan prices where to buy diflucan

http://cipro.guru/# where can i buy cipro online

http://cipro.guru/# buy cipro online canada

tamoxifen therapy raloxifene vs tamoxifen buy tamoxifen

https://nolvadex.guru/# nolvadex 20mg

http://diflucan.pro/# diflucan for sale uk

buy doxycycline monohydrate: buy doxycycline without prescription – doxycycline 100mg capsules

Cytotec 200mcg price buy cytotec online fast delivery buy cytotec online

http://doxycycline.auction/# order doxycycline 100mg without prescription

http://cytotec24.shop/# Cytotec 200mcg price

diflucan 150 mg price where to get diflucan diflucan cost uk

http://doxycycline.auction/# doxycycline 100mg dogs

https://doxycycline.auction/# doxycycline hyclate

generic doxycycline buy doxycycline cheap doxy

http://cytotec24.shop/# cytotec abortion pill

http://cipro.guru/# ciprofloxacin generic

http://angelawhite.pro/# Angela White

https://angelawhite.pro/# Angela Beyaz modeli

https://sweetiefox.online/# Sweetie Fox izle

https://sweetiefox.online/# Sweetie Fox modeli

http://evaelfie.pro/# eva elfie

https://lanarhoades.fun/# lana rhoades filmleri

lana rhodes: lana rhoades filmleri – lana rhoades filmleri

http://sweetiefox.online/# sweety fox

https://sweetiefox.online/# Sweetie Fox filmleri

https://evaelfie.pro/# eva elfie video

lana rhoades filmleri: lana rhoades video – lana rhoades

https://lanarhoades.fun/# lana rhoades video

http://evaelfie.pro/# eva elfie izle

http://evaelfie.pro/# eva elfie filmleri

https://evaelfie.pro/# eva elfie izle

https://angelawhite.pro/# Angela White izle

?????? ????: abella danger izle – abella danger izle

https://abelladanger.online/# Abella Danger

https://evaelfie.pro/# eva elfie

https://angelawhite.pro/# Angela Beyaz modeli

http://lanarhoades.fun/# lana rhoades modeli

http://evaelfie.pro/# eva elfie filmleri

http://sweetiefox.online/# swetie fox

http://abelladanger.online/# Abella Danger

http://angelawhite.pro/# Angela White filmleri

https://lanarhoades.fun/# lana rhoades filmleri

Angela White filmleri: Angela Beyaz modeli – Angela White izle

http://angelawhite.pro/# Angela White video

http://sweetiefox.pro/# sweetie fox new

fox sweetie: sweetie fox full video – sweetie fox new

mia malkova hd: mia malkova photos – mia malkova only fans

eva elfie videos: eva elfie – eva elfie photo

https://lanarhoades.pro/# lana rhoades videos

naked dating: http://evaelfie.site/# eva elfie new video

mia malkova new video: mia malkova full video – mia malkova latest

eva elfie: eva elfie photo – eva elfie videos

lana rhoades boyfriend: lana rhoades hot – lana rhoades

http://miamalkova.life/# mia malkova movie

mia malkova hd: mia malkova full video – mia malkova only fans

eva elfie videos: eva elfie – eva elfie hot

https://sweetiefox.pro/# sweetie fox

https://lanarhoades.pro/# lana rhoades videos

lana rhoades full video: lana rhoades hot – lana rhoades videos

lana rhoades: lana rhoades pics – lana rhoades hot

http://sweetiefox.pro/# sweetie fox new

sweetie fox full video: sweetie fox full – sweetie fox new

sweetie fox cosplay: fox sweetie – sweetie fox video

facebook dating: http://evaelfie.site/# eva elfie photo

http://lanarhoades.pro/# lana rhoades hot

eva elfie: eva elfie hd – eva elfie photo

fox sweetie: sweetie fox full – sweetie fox video

http://evaelfie.site/# eva elfie full video

https://miamalkova.life/# mia malkova new video

sweetie fox full: ph sweetie fox – sweetie fox cosplay

lana rhoades unleashed: lana rhoades videos – lana rhoades

http://miamalkova.life/# mia malkova new video

mia malkova movie: mia malkova only fans – mia malkova movie

http://aviatormocambique.site/# aviator mz

aviator jogo de aposta: melhor jogo de aposta para ganhar dinheiro – site de apostas

http://pinupcassino.pro/# pin up

https://aviatorjogar.online/# aviator jogo

play aviator: aviator bet – aviator malawi

http://aviatorjogar.online/# pin up aviator

http://aviatorjogar.online/# estrela bet aviator

http://aviatorjogar.online/# estrela bet aviator

http://jogodeaposta.fun/# jogo de aposta

jogar aviator online: aviator betano – aviator bet

aviator bet: aviator game – aviator ghana

http://aviatormalawi.online/# aviator bet

https://aviatorghana.pro/# aviator game

aviator sinyal hilesi: aviator hilesi – aviator hilesi

aviator oyna slot: pin up aviator – aviator oyunu

zithromax 1000 mg online: where can i buy zithromax uk – generic zithromax 500mg

http://jogodeaposta.fun/# deposito minimo 1 real

zithromax cost australia: zithromax suspension zithromax azithromycin

aviator pin up casino: pin up – aviator pin up casino

buy zithromax 500mg online – https://azithromycin.pro/azithromycin-zithromax-500mg-price.html where to buy zithromax in canada

https://aviatorjogar.online/# aviator pin up

zithromax price canada: how to get zithromax – generic zithromax over the counter

canadian pharmacy price checker CIPA approved pharmacies escrow pharmacy canada canadianpharm.store

п»їlegitimate online pharmacies india: Best Indian pharmacy – indianpharmacy com indianpharm.store

https://mexicanpharm24.com/# mexico drug stores pharmacies mexicanpharm.shop

india pharmacy: Pharmacies in India that ship to USA – india pharmacy mail order indianpharm.store

reputable indian online pharmacy Pharmacies in India that ship to USA п»їlegitimate online pharmacies india indianpharm.store

india pharmacy mail order: indian pharmacy – indian pharmacy online indianpharm.store

http://canadianpharmlk.com/# northwest canadian pharmacy canadianpharm.store

http://indianpharm24.com/# Online medicine order indianpharm.store

canadian pharmacy india Cheapest drug prices Canada canadian mail order pharmacy canadianpharm.store

cheapest online pharmacy india: Pharmacies in India that ship to USA – Online medicine home delivery indianpharm.store

http://canadianpharmlk.shop/# buying from canadian pharmacies canadianpharm.store

mexican drugstore online: order online from a Mexican pharmacy – pharmacies in mexico that ship to usa mexicanpharm.shop

canadian pharmacy canadian pharmacy meds reliable canadian pharmacy canadianpharm.store

https://mexicanpharm24.shop/# mexico pharmacy mexicanpharm.shop

https://indianpharm24.shop/# buy medicines online in india indianpharm.store

https://indianpharm24.com/# india online pharmacy indianpharm.store

https://indianpharm24.shop/# top online pharmacy india indianpharm.store

http://indianpharm24.shop/# indian pharmacy online indianpharm.store

top 10 online pharmacy in india: Pharmacies in India that ship to USA – best online pharmacy india indianpharm.store

reputable mexican pharmacies online Medicines Mexico medication from mexico pharmacy mexicanpharm.shop

http://amoxilst.pro/# amoxicillin 500mg prescription

prednisone 20 mg tablet: 5 mg prednisone tablets – prednisone in canada

where to get generic clomid: clomid symptoms – order clomid without rx

buying generic clomid without a prescription: femara vs clomid – where to get clomid no prescription

https://amoxilst.pro/# amoxicillin 500

prednisone 5 50mg tablet price: where to buy prednisone 20mg no prescription – prednisone 20mg prescription cost

http://clomidst.pro/# can i buy generic clomid online

amoxicillin from canada: is amoxicillin the same as penicillin – amoxicillin 500mg buy online canada

prednisone pills cost: how much is prednisone 10 mg – prednisone 2.5 mg tab

where can i buy amoxocillin: buy amoxicillin 500mg online – amoxicillin price without insurance

http://prednisonest.pro/# buy 40 mg prednisone

amoxicillin 500mg: side effects of amoxicillin in adults – buy amoxicillin online mexico

amoxicillin capsules 250mg: amoxil cost – amoxil pharmacy

https://clomidst.pro/# clomid otc

http://clomidst.pro/# how to buy clomid no prescription

amoxicillin discount coupon: generic amoxicillin cost – buy cheap amoxicillin online

prednisone 1 tablet: prednisone pill 20 mg – prednisone purchase canada

how much is amoxicillin prescription order amoxicillin online uk amoxicillin order online no prescription

how can i get clomid without a prescription: can you get cheap clomid without prescription – can i purchase generic clomid without dr prescription

http://clomidst.pro/# where to get generic clomid

http://edpills.guru/# ed medications online

prescription drugs from canada: online pharmacy delivery – canadian pharmacy no prescription

http://onlinepharmacy.cheap/# rx pharmacy no prescription

overseas pharmacy no prescription: canadian online pharmacy – best canadian pharmacy no prescription

legit non prescription pharmacies canadian pharmacy online online pharmacy no prescription

https://pharmnoprescription.pro/# buying prescription drugs online canada

prescription drugs from canada: mexican pharmacy online – canadian pharmacy world coupon

http://onlinepharmacy.cheap/# canadian pharmacy without prescription

http://edpills.guru/# best online ed pills

erectile dysfunction medications online: ed medicines – top rated ed pills

http://onlinepharmacy.cheap/# canadian pharmacy no prescription needed

http://pharmnoprescription.pro/# mexico prescription drugs online

top rated ed pills: online erectile dysfunction – cheapest ed treatment

http://pharmnoprescription.pro/# online no prescription pharmacy

online drugstore no prescription: medications online without prescription – canada drugs without prescription

http://pharmnoprescription.pro/# cheap prescription drugs online

http://edpills.guru/# cheap erection pills

purple pharmacy mexico price list: medicine in mexico pharmacies – purple pharmacy mexico price list

http://canadianpharm.guru/# canadian pharmacy antibiotics

https://indianpharm.shop/# online shopping pharmacy india

mexican pharmaceuticals online: mexican pharmacy – п»їbest mexican online pharmacies

mexican pharmaceuticals online: medication from mexico pharmacy – п»їbest mexican online pharmacies

pharmacy online no prescription: online pharmacy without a prescription – best no prescription online pharmacies

http://pharmacynoprescription.pro/# quality prescription drugs canada

http://pharmacynoprescription.pro/# order medication without prescription

best online pharmacies in mexico: pharmacies in mexico that ship to usa – best mexican online pharmacies

https://indianpharm.shop/# buy medicines online in india

indian pharmacies safe: buy medicines online in india – india pharmacy

buying prescription drugs in mexico: best online pharmacies in mexico – mexican pharmacy

http://canadianpharm.guru/# canada drug pharmacy

buying from online mexican pharmacy: mexico pharmacy – buying from online mexican pharmacy

http://indianpharm.shop/# Online medicine home delivery

https://canadianpharm.guru/# northwest pharmacy canada

reputable indian online pharmacy: Online medicine home delivery – india pharmacy

buy medication online with prescription: online pharmacy no prescription – no prescription needed pharmacy

http://canadianpharm.guru/# canadian pharmacy sarasota

reliable canadian pharmacy: canada cloud pharmacy – precription drugs from canada

canadapharmacyonline: canadian pharmacy phone number – canadian pharmacy review

https://pharmacynoprescription.pro/# no prescription medication

http://canadianpharm.guru/# recommended canadian pharmacies

online canadian pharmacy reviews: ed meds online canada – canadian pharmacy service

http://canadianpharm.guru/# canadapharmacyonline legit

reputable indian online pharmacy: buy medicines online in india – Online medicine home delivery

best canadian online pharmacy: best canadian online pharmacy – canadian pharmacy online ship to usa

https://pharmacynoprescription.pro/# how to get prescription drugs from canada

https://indianpharm.shop/# indian pharmacy online

http://pharmacynoprescription.pro/# buy drugs without prescription

no prescription needed pharmacy: best no prescription online pharmacy – no prescription on line pharmacies

online pharmacy india: online shopping pharmacy india – indianpharmacy com

http://mexicanpharm.online/# pharmacies in mexico that ship to usa

canadian king pharmacy: best mail order pharmacy canada – canadian king pharmacy

canadadrugpharmacy com: safe canadian pharmacy – certified canadian pharmacy

http://canadianpharm.guru/# canadian pharmacy 24h com

mail order pharmacy india: indian pharmacies safe – п»їlegitimate online pharmacies india

http://indianpharm.shop/# reputable indian online pharmacy

buying prescription drugs from canada online best online pharmacy without prescription canadian prescription drugstore reviews

http://canadianpharm.guru/# best canadian pharmacy

india pharmacy: Online medicine order – Online medicine order

canada mail order prescription: buy medications online no prescription – how to get a prescription in canada

http://pharmacynoprescription.pro/# no prescription pharmacy online

safe reliable canadian pharmacy: best online canadian pharmacy – recommended canadian pharmacies

pin-up bonanza: pin-up online – pin-up giris

https://slotsiteleri.guru/# bonus veren casino slot siteleri

aviator oyunu: aviator oyna slot – aviator hile

http://aviatoroyna.bid/# aviator bahis

aviator oyunu 10 tl: aviator bahis – aviator mostbet

deneme bonusu veren siteler: slot bahis siteleri – en cok kazandiran slot siteleri

en guvenilir slot siteleri: canl? slot siteleri – slot siteleri bonus veren

https://pinupgiris.fun/# pin up indir

slot oyunlar? siteleri: canl? slot siteleri – slot kumar siteleri

http://aviatoroyna.bid/# aviator oyunu giris

https://sweetbonanza.bid/# sweet bonanza slot

sweet bonanza siteleri: sweet bonanza 100 tl – sweet bonanza oyna

http://gatesofolympus.auction/# gates of olympus demo türkçe

sweet bonanza hilesi: sweet bonanza demo oyna – sweet bonanza guncel

aviator giris: aviator hilesi ucretsiz – aviator sinyal hilesi ucretsiz

https://pinupgiris.fun/# pin up bet

gates of olympus demo: gates of olympus nas?l para kazanilir – pragmatic play gates of olympus

Online medicine order Generic Medicine India to USA indian pharmacy

northwest canadian pharmacy: Large Selection of Medications – canadian pharmacy meds reviews

canadian pharmacy no scripts: canadian pharmacy 24 – canada pharmacy

vipps canadian pharmacy pills now even cheaper best mail order pharmacy canada

indian pharmacies safe Cheapest online pharmacy top online pharmacy india

thecanadianpharmacy: pills now even cheaper – canadian valley pharmacy

top online pharmacy india: Cheapest online pharmacy – online pharmacy india

best online pharmacy india: Generic Medicine India to USA – indianpharmacy com

buy prescription drugs from india Healthcare and medicines from India india pharmacy

vipps canadian pharmacy: canadian pharmacy 24 – canadian pharmacy review

canadianpharmacymeds com pills now even cheaper canadian discount pharmacy

purple pharmacy mexico price list: Mexican Pharmacy Online – mexican pharmaceuticals online

mexico pharmacies prescription drugs Online Pharmacies in Mexico buying from online mexican pharmacy

canadian drug stores: canadian pharmacy 24 – canadian pharmacy prices

mexican drugstore online: Online Pharmacies in Mexico – mexican border pharmacies shipping to usa

mexico pharmacies prescription drugs Mexican Pharmacy Online pharmacies in mexico that ship to usa

п»їlegitimate online pharmacies india: Healthcare and medicines from India – online pharmacy india

pharmacies in mexico that ship to usa: Mexican Pharmacy Online – mexican border pharmacies shipping to usa

http://indianpharmacy.icu/# pharmacy website india

cross border pharmacy canada www canadianonlinepharmacy best rated canadian pharmacy

mexican border pharmacies shipping to usa: Mexican Pharmacy Online – mexican online pharmacies prescription drugs

canadianpharmacy com: Prescription Drugs from Canada – reputable canadian pharmacy

indian pharmacy online indian pharmacy world pharmacy india

http://prednisoneall.shop/# prednisone 5 mg tablet without a prescription

where can you buy zithromax: where can i buy zithromax medicine – zithromax capsules price

amoxicillin capsule 500mg price antibiotic amoxicillin amoxicillin 875 mg tablet

https://amoxilall.com/# amoxicillin 500 mg

https://prednisoneall.shop/# buy 10 mg prednisone

buy zithromax online australia can i buy zithromax online where can you buy zithromax

http://prednisoneall.shop/# prednisone 30 mg daily

azithromycin zithromax generic zithromax azithromycin zithromax over the counter

https://zithromaxall.shop/# buy zithromax online cheap

viagra canada generic ed pills п»їBuy generic 100mg Viagra online

http://sildenafiliq.com/# viagra canada

http://sildenafiliq.com/# viagra without prescription

Cialis over the counter Cialis without a doctor prescription Buy Tadalafil 10mg

Cialis 20mg price in USA Cialis without a doctor prescription п»їcialis generic

http://kamagraiq.com/# cheap kamagra

buy viagra here: buy viagra online – sildenafil over the counter

Kamagra 100mg Kamagra Iq Kamagra 100mg price

https://kamagraiq.shop/# п»їkamagra

https://sildenafiliq.com/# Cheap generic Viagra

Buy Tadalafil 10mg: cialis best price – Generic Cialis without a doctor prescription

Sildenafil Citrate Tablets 100mg best price on viagra buy Viagra online

http://sildenafiliq.com/# sildenafil 50 mg price

buy viagra here: generic ed pills – sildenafil online

Kamagra Oral Jelly kamagra best price Kamagra tablets

http://tadalafiliq.shop/# Buy Tadalafil 5mg

http://tadalafiliq.com/# cheapest cialis

https://sildenafiliq.xyz/# viagra canada

Cheap generic Viagra Sildenafil Citrate Tablets 100mg cheapest viagra

https://tadalafiliq.shop/# Cialis without a doctor prescription

http://tadalafiliq.com/# Buy Tadalafil 20mg

Cialis 20mg price in USA: tadalafil iq – Cheap Cialis

http://kamagraiq.com/# Kamagra 100mg price

cheap kamagra Sildenafil Oral Jelly buy kamagra online usa

http://sildenafiliq.xyz/# viagra without prescription

viagra canada cheapest viagra Order Viagra 50 mg online

https://sildenafiliq.com/# Order Viagra 50 mg online

buy viagra here: cheapest viagra – sildenafil over the counter

https://sildenafiliq.xyz/# buy Viagra over the counter

http://kamagraiq.shop/# super kamagra

Buy Tadalafil 5mg cialis best price buy cialis pill

http://kamagraiq.shop/# buy Kamagra

canadianpharmacymeds My Canadian pharmacy canadian online pharmacy

buying prescription drugs in mexico: online pharmacy in Mexico – mexican pharmaceuticals online

http://canadianpharmgrx.com/# recommended canadian pharmacies

pharmacy in canada: Canadian pharmacy prices – northwest pharmacy canada

mexican pharmaceuticals online Pills from Mexican Pharmacy best online pharmacies in mexico

mexico pharmacies prescription drugs: Mexico drugstore – п»їbest mexican online pharmacies

Online medicine order: Generic Medicine India to USA – indian pharmacy paypal

canada drugs reviews Cheapest drug prices Canada certified canadian pharmacy

best india pharmacy: Generic Medicine India to USA – online shopping pharmacy india

https://mexicanpharmgrx.com/# medication from mexico pharmacy

medication from mexico pharmacy Mexico drugstore mexican rx online