It was interesting observing the ramp to launch Apple TV+ and Disney+ by both companies. Both were marketing their service more than I’ve ever seen a competitor market their TV service other than Hulu and the live sports campaign. Ads were on every major network, Twitter, Facebook, and more. Having spent some time thinking about the landscape, I think a few observations are worth pointing out.

Storytelling’s Golden Era and Competition

I use the framing of the Golden Era of storytelling because it was used by an executive of the MPAA during a presentation earlier this year. I thought the point was apt, and barring any major new player, we are right in the growth cycle for original stories via TV and movies. This chart I came across in a private report visualizes not just the sheer growth of new content but also how the new emerging players contribute.

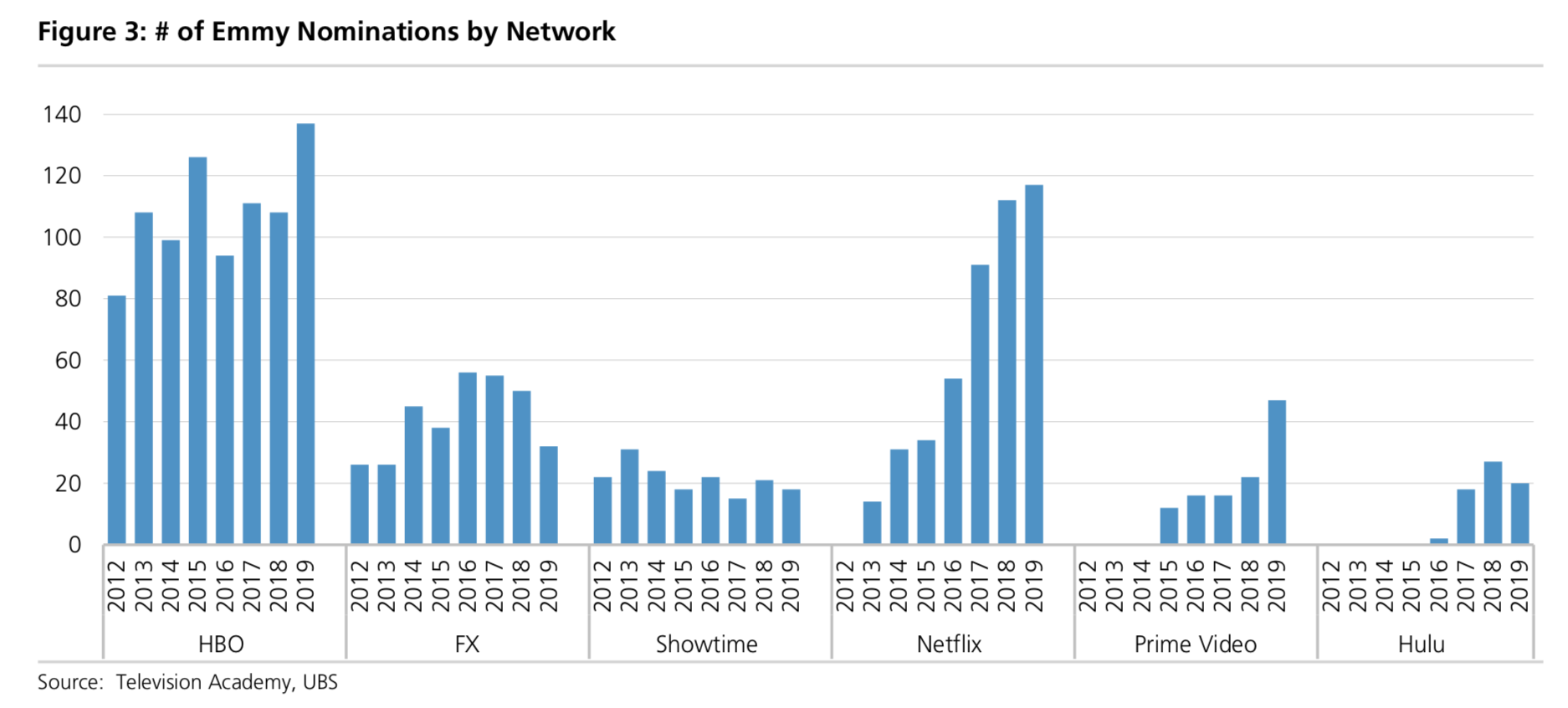

Assuming the trend lines hold, 2020 will see over 500 scripted shows, and one can argue the addition of Apple TV+ and Disney+, essentially the addition of Apple and Disney studios could increase this number faster than estimated. What I believe we are on the cusp of is a dramatic increase in competition for high-quality long-form content the likes we have not seen before. Prior to Netflix, one could argue HBO was the bar for producing routine quality original programming. Netflix and it is now ~$15 billion dollars a year on programming. Knowing that big investment in original content yields rewards, quite literally in this visualization, see the below chart I find fascinating.

Not to say Emmy nominations are the defacto way we can quantify we are in the golden age of storytelling, but just look at the growing number of nominations by network and in particular, how the newer entrants are growing. It will be fascinating to see where Apple ranks on this chart in a few years.

The big point I want to make here is competition is an all-time high. This is good and possibly bad for consumers.

Competing for Money and Time

There has already been a loud sounding bell by pundits that consumers simply can not, and will not, sign up for all these streaming services. Current research pegs the average number of streaming services a consumer will sign up for at 3. However, I think that number can go higher once they stop paying for traditional cable. Let’s just use a dollar number of $70-$80, which is the average cable bill in the US as the dollar amount up for grabs as consumers shift that budget to other things. Assuming people still need a streaming TV service (with live TV) and the front runners right now are Hulu and YouTubeTV, both services varying costs of $44-$60 per month, then it’s possible that anywhere from $10-$35 of the budget is up for grabs. This goes quickly but supports the idea of 3-4 additional streaming subscriptions.

The other thing to watch here is if consumers shift budget by season. We are already seeing this happen in certain situations where people subscribe on a month to month plan, watch the series they want then cancel. I sense this behavior could grow in popularity with younger consumers who are more savvy and creative, but if it becomes normal for a good size segment of the market, it could change how competitors think about their content strategy as well as their bundle options and pricing.

Within the broader point I just made, the biggest thing I think consumers are going to be hit with comes down to time. I know I may be making this point within the launch window of two new services from big, very good at marketing, players but I already feel overwhelmed by the amount of content/shows I like and/or am interested in and where am I going to find the time to watch. I know I’m not alone in this feeling.

This is why the CEO of Netflix Reed Hastings has always been keenly aware that Netflix’s biggest competitors are the ones that steal the most time from their service. He has used gaming/video games as his biggest worry, but he has to be concerned about Apple and Disney because both of them are not just well-positioned to deliver great content but to also better market that content than Netflix. Demand generation from Apple and Disney is absolutely going to impact time on Netflix, and Disney, in particular, has the best chance to hurt Netflix the most.

I am convinced we are about to see an explosion of high-quality content from those competing in this space, and together, between them all, it amounts to quantity. The challenge/impact on our time, especially with how good a few of these companies will market these services and create demand is going to be fascinating to watch but also a challenge to navigate for the mainstream consumer.