I genuinely love the industry analyst business. I love the role we analysts, our data, and our commentary play in helping companies make strategic decisions. However, I’ve noticed a disturbing trend. ((It’s a “Jump to Conclusions” mat! You see, you have this mat, with different CONCLUSIONS written on it that you could JUMP TO! — Tom Smykowski from the movie Office Space))

The challenge with data is that the truth lies in the interpretation. Without context genuine data can lead to disingenuous conclusions. This is why data cannot be put out in the public without context. Yet this is exactly what happens. It creates a scenario where a media industry who thrives on negativity can take genuine data, miss the context, and create stories around a false narrative. It is not their fault entirely. It is the fault of the data firms who release data to the public, without proper interpretation or context, and allow the media industry to draw their own conclusion, and often a false one.

Genuine data should point out market truths. However, when presented in the wrong way, it has the potential to do just the opposite.

Why We Count Things

The bottom line is data matters. If you are a company that makes touch-based displays or sensors you need a fairly accurate view of shipment growth related to the areas you care about so you can plan your long term product cycle. If you are a company that makes screens you don’t necessarily care what the operating system market share is of specific platforms. All you care about is how many screens will be sold over the next few years, and what the likely segment mix of screen size will be. For you, the data matters because you need to know how many to make. This is why forecasts and segment tracking statistics are relevant.

Data, forecasts, and other statistics, should help reveal an opportunity to the interested party. It should also help point out where there are not opportunities.

Not all data that gets put out in the public leads to disingenuous conclusions. However, it is the market share statistics that do so more often than any other. To make my point, and highlight how this happens, I will use the tablet market share narrative as an example.

The iPad Has Lost to Android

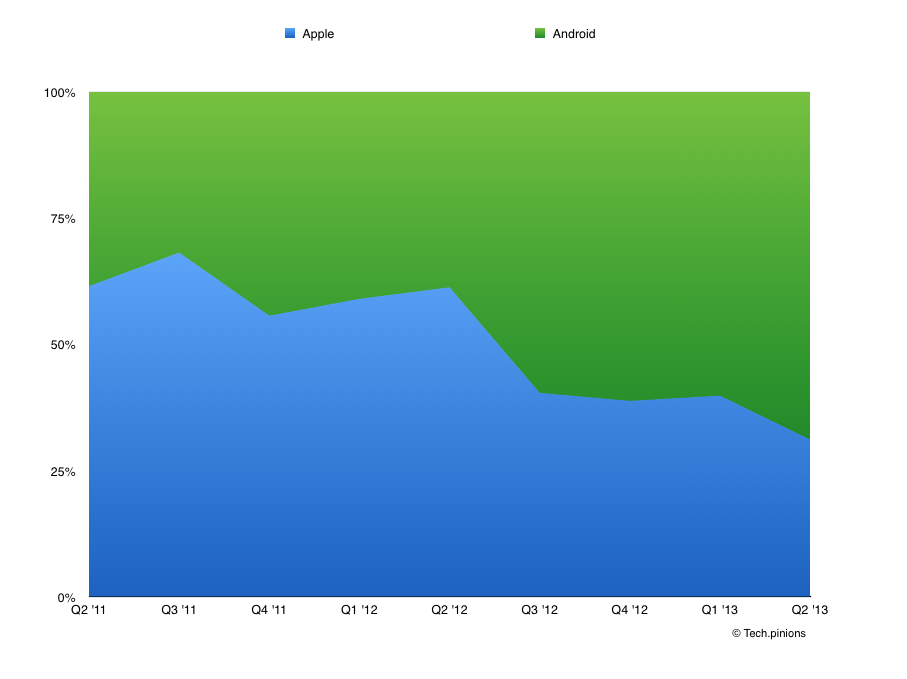

When you track the global sales of tablets, it is easy to look at the market share statistics and say that it is game over for the iPad. You can stare at the chart and conclude that the iPad can no longer grow as the world and the growth shifts to Android. There is some truth to the global statistics of Android’s tablet market share. At face value we create charts that look like this:

That is genuine data. Android is being shipped on more tablets than iPads. Therefore, the narrative that Android tablets outsell iPads is accurate at a bullet point level. However, the graph does not tell the whole story and yet so many are left to conclude it does.

If you are a software developer ((Software developers are ones for whom a market share discussion does matter. Perhaps the investment community does also but at large it is irrelevant for most.)) you will look at that chart and say “I should be writing tablet apps for Android.” The problem is… that is an incorrect conclusion when you have the context of the market share data points.

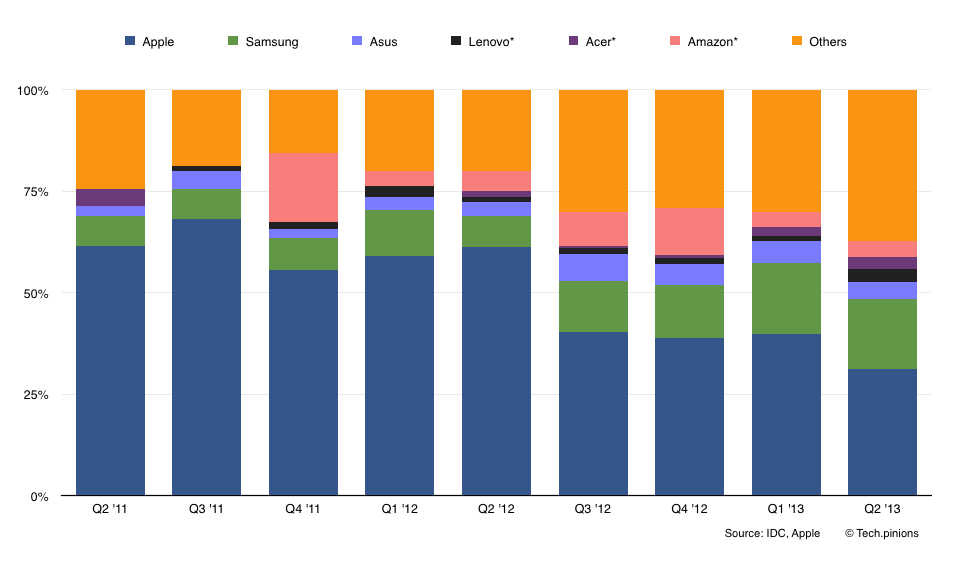

The picture starts to get more clear when we look at the market share of each vendor as a makeup of total sales. Here is that chart. ((Graph viewed with a stack chart.  ))

))

When we look at that chart we realize that the name brands shipping Android tablets are not shipping nearly as many as the iPad. We will also notice that the largest segment of Android tablets being sold come from this category labeled ‘other.’ Upon learning that ‘other’ makes up a significant portion of the number of Android tablets being sold; we must seek to understand what ‘other’ is and ask if it represents the same opportunity as the vendors who are shipping Android as a tablet platform tied to services and app stores.

Understanding Other

The category ‘other’ represents the no-name brand white-box tablets being sold at razor thin margins mostly in China and other emerging markets. Here are some visuals to help with some context.

I wrote about this point in particular where I dug into the gray market for tablets in China. It is a big market.

As I have been digging into the white box segment–which makes up the bulk of Android tablet shipments–I have been trying to understand what consumers are doing with these extremely low-cost devices. As we know, Android tablets globally make up a minuscule share of global web traffic. The latest estimates I saw peg Android tablets at less than .08% of global traffic while iPad is at 4% of global internet traffic. This has always been the stat that has caused us researchers to raise an eyebrow. Android has more volume but significantly less internet traffic. So what is happening?

Nearly all evidence and data we find comes back to a few fundamental things. First, most of these low cost tablets in the category of ‘other’ are being used purely as portable DVD players, or e-readers. Some are being used for games, but rarely are they connecting to web services, app stores, or other key services. I have asked local analysts, local online services companies, app tracking firms, and many many more regional experts, and the answer keeps coming back the same. They affirm that we see the data showing all these Android tablet sales. But they aren’t actually showing up on anyone’s radar when it comes to apps and services in a meaningful way.

Understanding the context, it is hard to genuinely conclude that ‘other’ represents an opportunity for anyone but the white box hardware companies making less than a dollar of profit and component vendors who can supply the parts to make such low-cost tablets. It is certainly not a genuine revenue opportunity for app developers, services companies, or other constituents in the food chain. And other makes up almost 40% of the Android tablets shipped world wide.

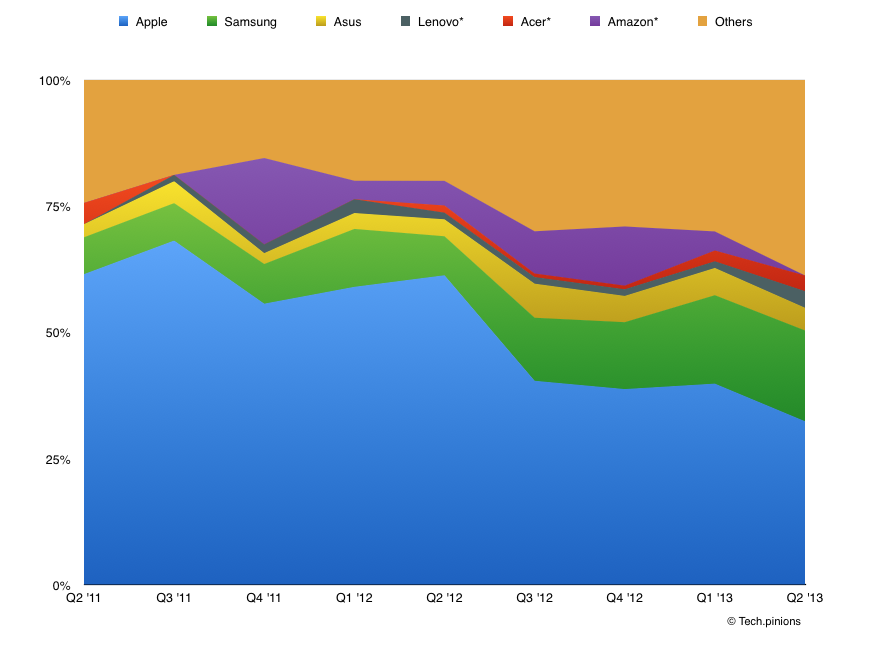

So let’s look at the chart without ‘other.’

Now we get a slightly clearer picture. If we eliminate ‘other’ Apple’s tablet share goes to over 50% WW with the closest competitor being Samsung at 18%.

Yet we are still left with a legitimate question which is relative to vendor growth. ‘Other’ is causing a downward trend for the competition. We know that ‘other’ was growing but ‘other’ is not an area any branded hardware OEM wants to go near. So, can vendors grow their share in a growing market against other? That is the key question. To shed insight into that question a little more context is necessary.

Our research, and many others, suggests that over half of first-time purchasers of low-cost tablets had buyers remorse and intend to spend up on their next one. This is why with many of the latest branded crop of OEM tablets, prices went up in order to invest in better components to better the experience.

Our research also suggests that those in the market for a tablet–who plan to use it to do meaningful things for the value chain–prioritize the experience over price. The tablet market as a whole is growing and I tend to view that growth separately from the ‘white box’ category. ((There is likely some percent of ‘other’ that does represent an opportunity, however, we have no idea how much. My suspicion is it is very small so I lean toward leaving it out entirely.)) Doing so brings much more clarity to what is happening in the market for the stakeholders.

We are still waiting for updated figures on these but I wanted to add the needed context about what is happening in the tablet market so that accurate opinions, and more importantly accurate business decisions, can be made with regard to this category.

A similar analysis can be done on the market for smartphones, but I will leave that project for another time. Data is good. But it is dangerous when it is released into the public without context. Data should inform not confuse. Yet, more often than not, data that gets thrown around in the public sphere clouds the truth rather than brings clarity to it.

Very well presented, Ben. I’ll have to send you a Zeedpad for Christmas.

He’d much prefer a FlyTouch. They’re 10″!

And they’re too poisonous to be used by children under 10 years old!

Then how are they made?

One thing you didn’t mention is that at least some of the name-brand tablets are likewise being used in the same way as “other” tablets. For example, kindle tablets (especially the lower end ones) are being marketed very much as the first world equivalent of “other” — extremely low cost, designed to be of benefit only to Amazon’s ecosystem, and likely not being used much outside of the Amazon store.

At this point I’m not going to split hairs on what I consider legitimate tablets. Of course, we can nitpick those points but I get the point of those products from a business model standpoint to Amazon. I’m sure I can find that some percentage of even legitimate tablets are not doing many things Steve Jobs believed a tablet should but if I tried.

Actually Samsung is probably the manufacturer whose products are most spread out, with some of their many many tablet models going to high-end use and competing against Ipad, and the rest of their tablets competing against the Chinese white boxes.

Except there is no high-end tablet PC software on Samsung devices, which means they are always a low-end tablet even if you pay $2000 for one. Also they have no security and privacy and run a million malwares.

Truth is, iPad is part of the $300–$800 PC market and the other tablets are DVD players and giant generic phones. When everything has a touch screen, the practice of lumping together unlike devices solely because they have touch will look ridiculous to everyone.

Yes, but. Yes, many do use them that way. I’ve also seen stats that show Kindle users spend a lot more money on apps and content than other Android users, which makes sense, since someone buying a Kindle knows they’re essentially buying a digital vending machine.

Kindle’s a bit of an odd duck in the tablet flock. High user engagement with Amazon’s ecosystem, but are they really being used for web browsing, or as netbook replacements, the way the Ipad is being used.

The Apple equivalent of Kindle is iPod — a media player — not iPad, which is a tablet PC.

iPod heritage is music, Kindle heritage is books. So Apple’s media players are small, pocket-sized, and gym-friendly, but Amazon’s media players are book-sized and super cheap. Both are still $200 devices that have top-level content menus (music, movies, books, games) and run apps made for phones.

Nothing to do with iPad.

What surprises me about the graph is Samsung having such a large chunk of the Android market. Their tablets are kind of crappy.

The galaxy tab 3 7″ still has a 1024×600 screen, with slow processor and weak GPU. Why wouldn’t everyone buy a Nexus 7 or Amazon Fire instead of this POS.

You saw my post on the state of tablets? I threw my own Samsung estimates in there and from other sell through folks I know I was told it was pretty accurate.

Samsung is also practically giving the tabs away in Europe with the purchase of new phones and data plans from a carrier.

Samsung also gives away tablets with many of its high end TVs, though that stat alone can hardly account for all the volume. My analysis concurs with DarwinPhish – you can buy a Samsung tablet pretty much anywhere in the world, and Samsung also invests in marketing and merchandising at retail pretty much everywhere in the world. Amazon and Nexus products are sold in limited geographies, and even then primarily through online channels in those countries. If you want a branded, non-Apple tablet outside the U.S., UK, and a handful of other places, Samsung is your go-to brand of choice.

“Why wouldn’t everyone buy a Nexus 7 or Amazon Fire”

Distribution and availability.

Nexus and Kindle are boutique brands and US-only and sell in minuscule numbers.

Why use an area graph when a stacked bar graph of actual tablet sales per quarter will show more context?

Exactly. Rather than falling into the trap of talking about share in the first place, let’s just talk about actual sales growth.

I suppose that is what this article is about. Market share without understanding market dynamics us useless, i.e. falling market share in a rapidly expanding market might not be bad.

Except that if you only read this article you don’t actually know the rate at which this market is expanding (or even that it is expanding). Breaking down the share chart does accomplish the first step of showing how it can be dangerous to accept numbers at face value. I think we’d just agree that also showing actual sales would further the argument that there is life left in Apple tablets.

Yes, that is one of the faults of the graphics in the article. But, the article itself is trying to highlight some of the market dynamics, and how they affect the data. I think Ben could be more clear on how to properly analyze market share, including the use of appropriate charts.

I actually did look at the data as a bar graph and because so many vendors had such minuscule share it made it hard to look at and and more confusing than insightful. I looked at the the data every way I could and the graphs I used showed the trending lines in a way more representative at what is happening.

What is very interesting is that tablets have slowed but other is growing. We thought for a while that other would slow but it has not. My point about the China article I mentioned is that there is ample evidence to suggest these low-end tablets pave the way for upgrades to better tablets as consumers mature their interests with the device.

This is why for me the fact that other is growing presents and opportunity for other brands with better experiences to get those customers to graduate up.

That is why I pointed out that overwhelming data is coming in supporting that customers buy a cheap tablet then look for a better one next time around.

Knowledgable readers understand the context of market share, and the limitations it holds. But if you were to present these types of graphs to a wider audience, many would think that the iPad is selling less and less as they will likely just read the graph, and, even if they do read the article, the graph will stand out more than the text. So, in that case, I think to the layman, these graphs are misleading about what is going on in the tablet market.

Personally, I would still like to see the quarter by quarter stacked bar charts, especially for the first graph. I am wondering how they would be received by the audience here. I know that Horace Deidu on Asymco went through this a while back, and stopped using area charts like this because, I think it was Matt Drance made a comment on how area graphs tend to be visually misleading (no links because this is a vague memory), but still technically accurate.

Ok, look at the footnotes again.

Thanks. Look at Acer for a bit on both of the graphs. The bold red on the stacked area graph makes it seem that they are significant, even in Q3 ’12. However, you can’t even see their piece on the stacked bar for that quarter. Even colour is going to affect the perception of your data. You provide a lot of context around your graphs. Many “analysts” who write in a prolific way purposefully obfuscate the context to preach a point. It is easy to hide behind lazy data and purposefully misleading visual. I am glad that you aren’t.

And it wasn’t Matt Drance, but Dr. Drang who talked about stacked area graphs in this post:

http://www.leancrew.com/all-this/2011/11/i-hate-stacked-area-charts/

Ah, thanks for sharing. I still see some value in the area graph just because it does show more clear if something is trending up or down. But provably best to just use them both. I always start with the stacked charts.

What I need to do is now layer that on top of the markets growth rate and what I feel are accurate forecasts going forward. Need to think about how best to present this but the idea is to show that picture as a part of a growing segment over the next few years.

Kudos, Ben. This is one of the best articles I have read on TechPinions.

Thanks. Much appreciated.

I agree that there is a lot of misuse of data, but I raise an eyebrow whenever anyone talks about “truth” in data; truth is far too slippery, and markets are far too complex.

And also look at ‘share of use’ – i.e. what portion of tablet-consumer ecommerce, social networking, streaming video is iPad vs various makes of Android. Would be interesting to know. From what I’ve read, iPad has a higher market share in those areas.

Some good points, Ben, but let’s also remember that as recently as ten years ago, Apple itself was in the “Other” category of PC makers—not in the top 5. While Jobs & Co were trying to get a break with the iPod, Microsoft and its many OEM partners were comfortable enough that Gates could hand over the reins to Ballmer.

Market share by brand is inherently backwards-looking. Extrapolating trends works OK for the short run, but isn’t likely to give you much insight about the next decade, as the PC example shows. In the tablet subset of PCs, where we’ve had a couple of famous brands implode (HP/WinSlate, Motorola/Xoom, HP/WebOS & BlackBerry/Playbook) in the <4 years (!) since the iPad was introduced, trends by brand might measure in weeks, not years.

The backward bias is important. In investing, throwing away all the history of a firm that does poorly leads to “survivorship bias” in fund analyses, making it look like all the ones available did very well. Here, tossing out “Others” simply on the basis of not having achieved scale yet, leads to a discounting of the low-end disruption effect, the same thing that took Microsoft's market share of computing down by about 75%.

I don't mean to support the ‘Apple is doomed” meme by this comment; your usage analysis is right on the point. What comes next is what matters. Apple apparently believes that they have a sufficient edge on app developers that they don’t ALSO need to cut prices to fend off competitors, and surely they understand their business better than I do.

Agreed. There is a deeper analysis to be done on other, but since they are mostly non-name brands and really none of them have any interest in becoming name brands, it is hard to see them as a brand challenger. Huawei, ZTE, etc., are not in the other category. There is a gold rush right now in those cheap low-end devices.

I’m yet to see ‘other’ as a threat yet to the name brands who are not just trying to be the cheapest product out there. That is obviously the bit I track a bit more close in trying to understand who is under pressure and who is not.

No. Apple was always a name-brand, and even at the worst time in the 1990’s, Apple had over 50% of the high-end PC market, which is the only PC market they participated in before 2010.

By your logic, you can use the sub-$20,000 car market to prove BMW no longer exists.

Graphs worth a thousand words.

Ben,

Why not blame the media? Do they not have access to webbrowsers, computers and telephones? Nothing is stopping them from getting the truth behind the numbers, but desire and frankly, enough professionalism to want to be accurate.

Even since the Steve Jobs passed, the media and tech punditry have been tripping over themselves to be the first the say “I called it first. Apple’s demise!!” And as Apple continues to defy this expectation, instead of mea culpas, we instead get a “doubling down.” Who was it, Gene Munster who seemed to all but accuse Apple of lying and channel stuffing because he failed to predict the number of units sold on the iPhone launch weekend.

As long link-baiting and “Apple is doomed.” stories remains the primary objective, the narrative will never be accurate.

Agreed. I am being kind to them by not placing more blame on them. I’m sure that even if my analyst colleagues at the big firms put the perspective around the data the media would still distort it.

The error that all of us make is the assumption that the analysts in question are on a quest for truth or have a desire to present the unvarnished facts.

They are not and do not.

The financial press has a vested interest in promulgating a narrative to move stock in the direction they need to move to make money for their Wall Street puppet masters. Almost all of the most egregiously stupid commentary from the financial press (Trip “Tim Cook Should Be Fired” Chowdry leaps immediately to mind) is predicated on the fact that all Wall Street ultimately cares about is the price of APPL and how it can be made to move or dance in a matter that allows the firms on Wall Street to make money. They do not care for one minute about the effort Apple puts into it’s products, the loyalty of Apple’s customers or even technology in general. To them, Apple is a company that makes Widget 1, and according to their charts and figures Widget 1 must do B while also doing A and in the future be seen to do 5 while not doing M. Plug any combination of “margins” “profits” “market share” “stock price” “emerging markets” “innovation” and “colour” into that formula, heat to lukewarm and ladle out to skittish investors whose money you need to move around to make money.

Carl Icahn’s “wag the dog” mentality is the epitome of a nearly delusional mindset that dictates now that Apple has built this amazing financial empire, Apple is beholden to parasites like Icahn to take on staggering amount so debt so that others can have leverage on Apple and buy and sell this debt in “vehicles” designed to maximise profits while abrogating responsibility and leave governments holding the bag.

As far as I am concerned, the spectacle of Icahn pressuring Apple to load up on debt is a microcosm of the exact mentality that led the banks to cause a meltdown of the global economy while escaping any and all responsibility for said meltdown.

The media write a sellable story first and then get the “facts” to fit. That is capitalism.

Good article.

The car analogy is overused and abused, but the tale that the “analyst” press is pushing is that BMW should be horrified by sales of the TaTa.

Good post Ben.

While reading it I found myself thinking about the whole “Is a Tablet a PC?” hair splitting then went on a few years ago.

I do wonder if these “other” are poised to be a low end disrupters of the future; good enough to do the job the are hired to do know while creating an enviorment where am innovative alternative ecosystem develops.

No. You can’t plant an oak tree in a thimble. You can’t build a 100 story brick house — you need girders and steel to build a skyscraper. These low-end tablets do not support PC class apps at all. They lack a ton of infrastructure that takes decades to develop.

Someday we’ll see Windows tablets in the data. Right? Right? (hold the snark, please)

Windows tablets are there, but too small a number are sold to show up.

Super, Super article.

The problem is that “tablet” and even “smartphone” are very loose categories. So “data” about the “tablet market” and “smartphone market” will always need to be contextualized by removing pretenders from the category.

If you split the tablets into “tablet PC’s” (PC replacement) and “tablet media players” (DVD/book replacement) then Apple has 99.9% of tablet PC’s and the rest is Microsoft.

OMG an Analyst that actually provides factual data. Charts, clear factual analysis and no click baiting conclusions! Good job sir!

There are three basic ways to look at the market for a given type of products: Market share of major participants, Units sold by these participants, and Profit of individual participants.

Market share has no meaning outside of commodities and products that are technologically and functionally near-undistinguishable from brand to brand. For many years in the western world, this was largely the case in the sector of machines running Windows. Today, however, analysts who still use this sole metrics to judge between brands make a serious error. Thus, the charts of Ben Bajarin are interesting but they are insufficient to provide meaningful information for the shareholders of the individual participants.

Data on units sold by each participant has some validity in individual sectors, but lack the usefulness of dollar sales which factors in the fact that some machines are much more expensive (and often more profitable) than base models. From a shareholder, it is a valid information but still insufficient.

To shareholders, the only meaningful data is profits; gross profit and net profit. If Ben Bajarin were to produce the same charts based on sector profits of participants, the reader would instantly get a clear and meaningful picture and understand Apple’s strategy. I don’t claim any of his statements are false, but they are insufficient and by reason of this fact risk confusing readers with little financial background. To put it another way, profits on sales are the only elements that can be trusted to be meaningful.

This makes sense to me. Market share is not important to Lamborghini or Burberry. What is important to them is providing what people who buy Lamborghini and Burberry want. Apple is the luxury brand of what it sells. Others commoditize imitations of Apple products then compete with each other on price for market share. For them, market share matters. For Apple, it’s meaningless. I ignore all analysis of AAPL based on market share.

They key to all of this discussion, which is mainly my point, it that context is important for the audience. If I was presenting data to investors I would do it one way. If I was talking to developers, I would do it another. If I was talking to a semiconductor company another way.. etc.

In a public analysis you simply can’t address everyone. That is why we try to address a more business audience with our site here. But even then it is hard to distill 25 slides of data to a public article.

The goal of this post was just to point out why context matters. And of course that context varies by audience.

excellent analysis!

Two things:

1) Even in the “no other” second chart, we see Samsung rapidly improving its share relative to Apple.

2) I think charts of total shipments (that would show Apple growing for most of ’11-’13, albeit more slowly than some of their competitors) are much more useful.

Let’s put Sony, Dell, HP, Toshiba… in the “other” category and pretend they’re cheap OEMs for cheap users who’ll never ever pay a cent for apps….

very satisfying in terms of information thank you very much.

Unbelievable Transformation: How a £80 Shed Clearance Netted £2K!The world of reselling is filled with stories of ordinary individuals turning small investments into substantial profits, and one such story that stands out is the incredible transformation of an £80 shed clearance into an astonishing £2,000 windfall.The Initial GambleIt all began with a seemingly modest £80 investment in a shed clearance. Shed clearances are often overlooked opportunities to uncover hidden treasures amidst what might seem like junk. This particular venture started with cautious optimism and a determination to explore what lay within.The Treasure HuntAs the shed clearance progressed, it became increasingly apparent that there were items of value tucked away amidst the clutter. From vintage motor memorabilia to forgotten DJ music equipment and even dusty reels of vintage film, the shed held a trove of potential treasures.The Reselling StrategyRecognizing the potential value of these items, our intrepid reseller took a strategic approach to reselling. Each discovery underwent careful research to determine its market value and potential demand. Armed with this knowledge, the reseller set out to maximize profits through online platforms like eBay, Etsy, and various reselling communities.The BOLO AlertAmidst the research, a momentous discovery was made – a BOLO (Be On the LookOut) alert-worthy item. A vintage Walkman, seemingly forgotten in the shed, turned out to be a coveted collector’s item worth an astounding £500 or more. This unexpected find served as a significant boost to the potential profits.The £2K PayoffThrough diligent research, effective marketing, and strategic pricing, the reseller’s efforts began to bear fruit. Collectors eagerly snapped up the vintage motor memorabilia, musicians embraced the DJ music equipment, and cinephiles cherished the vintage film reels.The Unbelievable TransformationIn the end, what began as an £80 shed clearance transformed into an incredible £2,000 in profits. This remarkable success story serves as a testament to the untapped potential that can be found in the most unexpected places. It’s a reminder that with a discerning eye, thorough research, and access to online reselling platforms, anyone can turn a small investment into a substantial financial gain.This story not only inspires resellers but also highlights the hidden opportunities that may lie dormant in old sheds, garages, or attics. It encourages individuals to explore their own spaces, searching for overlooked treasures that could be converted into valuable assets.In the reselling world, every item has a story, and with the right strategy, those stories can lead to truly unbelievable transformations.

!This could be a little off the mark. Can you elaborate for me please? 🙂

Simply wanna tell that this is very beneficial, Thanks for taking your time to write this.

I’m impressed, I must say. Actually rarely must i encounter a blog that’s both educative and entertaining, and let me tell you, you have hit the nail within the head. Your concept is outstanding; the pain is an element that too little consumers are speaking intelligently about. I am delighted that we found this within my search for some thing relating to this.

Nice post. I learn some thing very complicated on different blogs everyday. Most commonly it is stimulating you just read content off their writers and rehearse a specific thing from their website. I’d would prefer to use some while using content on my small weblog whether or not you do not mind. Natually I’ll provide you with a link on your web weblog. Appreciate your sharing.

i like to search the internet for new kitchen gadgets to add to my kitchen..

Can I just say such a relief to find someone who in fact knows what theyre referring to online. You actually know how to bring a concern to light to make it important. More people need to check this out and understand this side in the story. I cant believe youre less popular since you certainly develop the gift.

Hey there, You have done a fantastic job. I will certainly digg it and personally suggest to my friends. I’m confident they’ll be benefited from this website.

The Linden method is known cure for anxiety conditions seen in many people all over the world. The creator’s long time research and study made it a dependable treatment for the disorder.

Really nice style and design and excellent content , nothing at all else we need : D.

Many thanks for making the effort to discuss this, I feel strongly about this and like learning a great deal more on this matter. If feasible, as you gain knowledge, would you mind updating your webpage with a great deal more info? It’s really helpful for me.

Valuable information. Lucky me I found your site by accident, and I am shocked why this accident did not happened earlier! I bookmarked it.

This committee help to many people. You can use their services in your work. You can read research papers about all details of their work.

This particular thread may seem to get quite a few page views. Exactly how do you support it? The application provides marvelous uncommon take onto matters. I reckon that going through things tremendous or possibly a lot of furnish home elevators is the main problem.

I admire your work , regards for all the useful blog posts.

A very informative film that helps me understand how complex the world financial landscape has become.

I always visit new blog everyday and i found your blog.,,-:*

Superb brief which write-up solved the problem a lot. Say thank you We searching for your data?-.

There are a handful of fascinating points over time in the following paragraphs but I don’t know if I see them all center to heart. There’s some validity but I most certainly will take hold opinion until I check into it further. Excellent article , thanks therefore we want much more! Added to FeedBurner as well

That is certainly when I commenced contemplating learn how to do anything at once. I commenced rearranging facts on my blog in order to provide my loyal guests the capability to comment and obtain do-follow backlinks and virtually remove all of the automated comment posting as soon as and for all.

Hello. i can see that you are a really great blogger,

performing arts is my thing, i am very much interested to learn more on this art’

I was just looking for this info for some time. After six hours of continuous Googleing, at last I got it in your site. I wonder what is the lack of Google strategy that don’t rank this type of informative web sites in top of the list. Normally the top websites are full of garbage.

i frequent hair salons because i always want to keep my hair in top shape;;

Thank you, I’ve been searching for information about this subject matter for ages and yours is the best I’ve located so far.

Youre so cool! I dont suppose Ive read anything in this way prior to. So nice to uncover somebody with some original applying for grants this subject. realy thanks for beginning this up. this fabulous website is one thing that is needed online, somebody after some originality. helpful project for bringing new stuff towards net!

Spot up for this write-up, I actually think this excellent website wants far more consideration. I’ll probably be again to learn to read a lot more, thank you for that info.

Greetings! This is my 1st comment here so I just wanted to give a quick shout out and tell you I truly enjoy reading through your posts. Can you recommend any other blogs/websites/forums that go over the same topics? Thanks!

You could certainly see your skills within the paintings you write. The arena hopes for more passionate writers such as you who are not afraid to say how they believe. At all times go after your heart.

Unquestionably believe that which you stated. Your favorite justification seemed to be on the internet the simplest thing to be aware of. I say to you, I certainly get annoyed while people consider worries that they plainly don’t know about. You managed to hit the nail upon the top as well as defined out the whole thing without having side effect , people could take a signal. Will likely be back to get more. Thanks

Great web site. Lots of useful info here. I am sending it to several friends ans additionally sharing in delicious. And of course, thank you in your sweat!

I am extremely inspired together with your writing abilities and also with the structure to your blog. Is that this a paid topic or did you modify it yourself? Anyway keep up the nice quality writing, it抯 uncommon to look a nice blog like this one nowadays..

Sweet, naughty girl, hottest sex chat for free, going to give you the best pleasure!

I’ve been surfing online more than 3 hours today, yet I never found any interesting article like yours. It抯 pretty worth enough for me. Personally, if all webmasters and bloggers made good content as you did, the web will be a lot more useful than ever before.

Hi there, I found your web site via Google while searching for a related topic, your web site came up, it looks good. I have bookmarked it in my google bookmarks.

This web site is mostly a stroll-by for all the information you needed about this and didn抰 know who to ask. Glimpse right here, and also you抣l positively discover it.

等身大 ラブドール 2021年に精力的に提案された7つの最新のダッチワイフ