It looked like Apple and the banks on one side and retailers on the other were headed for a war over phone payments. But now, Samsung seems ready to make it a three-sided fight. An article by Jason Del Ray on Re/code reports Samsung is negotiating with Massachusetts-based LoopPay over adding a third method for mobile payment to its product line.

Assuming Samsung jumps in, and the company is so far not commenting, it adds new complexity to the fight (Insiders). Apple Pay has the advantage of being the most sophisticated emerging standard with broad support of banks and credit card companies who are already advertising its availability. But it requires hardware accessible only in the iPhone 6/Plus, and Apple has shown no indication of any plan to make it available for use on non-Apple phones. CurrentC, the product of Merchant Customer Exchange (MCX), a consortium of big retailers, will work on a variety of iPhone and Android phones. While Apple Pay (and the related Google Wallet) uses Near Field Communication (NFC) to send encrypted data from the phone to the retailer, CurrentC uses a QR matrix on the screen of the phone to be read and interpreted by the retailer.

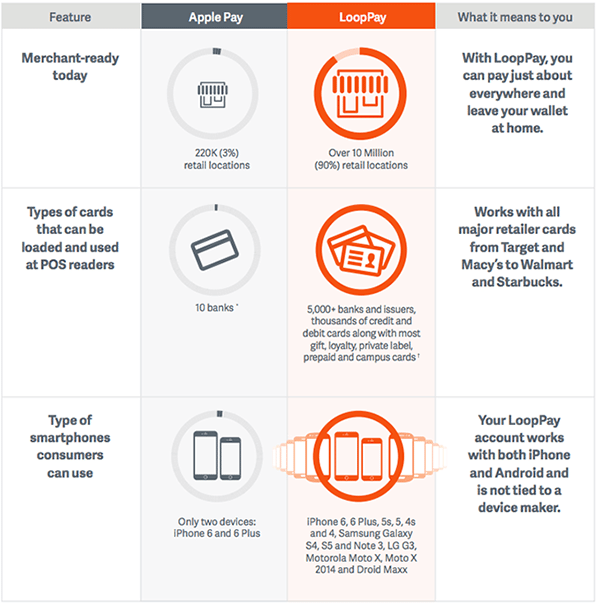

LoopPay (video demonstration) generates a data signal through a technology it calls a Magnetic Secure Transmission. The data can be read by existing retail devices that believe a card was just swiped. There are two big drawbacks. One is it requires the use of one of several devices that include a LoopPay CardCase, which serves as an iPhone case, and a LoopPay Case, a free-standing device that can be used with no phone attached. Both of these devices has a built-in system that can be set up for retail use by swiping a card once. Presumably, an adoption by Samsung would result in the LoopPay function being built into phones. The second disadvantage is it is designed to need standard swipe-able credit cards at time of purchase. Apple Pay and CurrentC may disagree on just about everything else, but they agree on the desirability of eliminating traditional credit cards as quickly as possible.

LoopPay is trying hard to argue its choices represent the strongest option. In a public note, LoopPay CEO Will Graylin argues the company’s approach, described as David v. Goliath, is superior to Apple Pay, Google Wallet, and the largely abandoned Software (CurrentC is not discussed). He claims LoopPay provides equal security to Apple Pay and LoopPay allows consumers to stop worrying about credit cards. “One less thing to carry is one less thing to worry about or lose,” Graylin writes. “They want to use the cards they already have, at their favorite merchants, on the devices they own. Their wallet account is personal. It should belong to them, and not be tied to any one device or just a few select banks.”

It looks like Samsung would face a serious hurdle with LoopPay in challenging both Apple Pay and CurrentC. Apple and its supporters are moving aggressively to take advantage of the solo control of credit card transactions. The other night, I saw back to back TV ads from CitiBank and BankAmerica supporting Apple Pay. MCX supporters Target and Walmart are likely to advertise CurrentC when it becomes available on phones next year.

It looks like Samsung would face a serious hurdle with LoopPay in challenging both Apple Pay and CurrentC. Apple and its supporters are moving aggressively to take advantage of the solo control of credit card transactions. The other night, I saw back to back TV ads from CitiBank and BankAmerica supporting Apple Pay. MCX supporters Target and Walmart are likely to advertise CurrentC when it becomes available on phones next year.

Unlike the Apple-bank alliance and CurrentC, Samsung’s use of LoopPay, assuming they could get phones supporting it into the markets quickly, is going to find it tough to fight with one force already working hard and another that will enter the market soon with a big pitch. But Samsung has been active in trying to add consumer services beyond making phones and its complex relationship with Google may account for its lack of interest in promoting Google Wallet. They would be getting into the fight very late, but Samsung could make the battle more interesting.

Can someone please invent a technology that makes me keep my money? 😉

Anarchist!

We are REQUIRED to spend, spend, SPEND!

Savers are worthless in the eyes of the market.

My finances improved hugely when I dumped credit cards.

I spend but never borrow.

Piggy bank! 😉

Waiting for Apple to invent it so I can get the Android version…

🙂

Did someone mention “CurrentC” and “LoopPay”? …

CurrentC is a “dog”; the MCX consortium should cut its losses on this clearly ectopic pregnancy and arrange a D&C ASAP, before it is too late to lawfully do so; for, surely, the result of this union will undoubtedly be a most ugly, seriously handicapped child, which will be an enduring embarrassment for all those that ever spent any time in the MCX bed working on this unnatural conception. All MCX finally needs to finish the job is to hire eBay’s Johnny Ho: he has proven extremely capable of disposing of even perfectly good body parts.

The fact is, buyers receive none of the statutory “credit card” protections if they give the payment processor (eg, PayPal, CurrentC, whoever) an authority to make direct debits on their bank debit account. Consumers get the protections that merchants pay for when they pay via a credit card; it’s a cost of doing business for the merchant—for the buyer, no credit card, no statutory protection.

Merchants are also at risk; such Automated Clearing House (ACH) direct debit transactions are not interactive; they are aggregated for overnight settlement; the ACH mechanism was never intended for, nor is it therefore suitable for, payments for goods that are going to immediately walk out the door because, if there is an insufficiency of funds/credit in the payer’s bank account, then the bank will reverse the transaction the following day.

LoopPay sounds to me like just another intermediary, like eBay’s clunky PayPal …

But the odd thing about this article is that there is still no mention of MasterCard’s “MasterPass” or Visa’s “Visa Checkout”. Regardless, with the arrival of these new online/NFC mobile digital wallets from MasterCard and Visa, and now Apple Pay, outside of the atrophying eBay marketplace—except for its rightfully deserved place as the online merchant account provider of last resort—the clunky “PreyPal” is now effectively redundant—and so is LoopPay …

I’m inclined to believe that CurrentC is never really going to take off, but I want to give the backers a chance to launch it before I write it off. It does have powerful backers, but it’s not clear they know what they are doing.

MasterPass and Visa Checkouts don’t really seem to be going anywhere, at least in the U.S. MasterPass has the support of only Citi and a bunch of small regional banks. I think that’s why they decided to throw their support behind Apple Pay.

I want to give the backers (of CurrentC) a chance to launch it before I write it off. – Steve Wildstrom

Your wait and see attitude makes eminent sense. However, based on what I’ve read about CurrentC I just can’t see how it’s going to catch on. It sounds like it makes payments much, much harder, not easier.

Isn’t that a good business model?

Which business model is that?

The one where you makes things (more) painful for prospective customers by making PayPal look reasonable. Take that suckers…how does that make you feel? Pain? Regret? Yes please sir.

The attractiveness of Apple Pay to the issuing banks is, of course, the apparent improved security; still, “MasterPass” and “Visa checkout” appear to offer a similar level of security, if not quite as conveniently applied as Apple Pay; regardless, why the issuing banks would be so eagerly pushing Apple Pay instead of MasterPass or Visa Checkout (which are available on any NFC-enabled phone) for POS transactions is strange …

essentially, Apple seems to have the best (most reliable, able/willing to spend, credit availability?) customers. Why wouldn’t you go with a captive audience that appear to make purchases not solely based on absolute cheapness, especially when the offered system provides better security that will lower operating costs with virtually no friction. Loopay might offer some similar benefits, but seems to require more equipment to manage on the customer side.

If not conveniently applied, few might bother with the risks and setup hassles of a new system, especially after previous experiences with credit card related setups. Remember the fun and loops involved with our Paypal friends, the special feeling of more passwords, logins and new providers? Figuring out which menu might be hiding the action you were trying to recover from or get information about?

And you think that these people are going to spend more simply because they can now use their iPhone to pay—I think not, at least not after the novelty wears off. The real market for the banks is in all smart phones, not just iPhones …

Regardless, Apple Pay will be a success to the point that iPhone users choose to use it—no more, no less …

To set up “MasterPass” for myself I only had to click on the “activate” button on my internet bank account “MasterPass” page; by default all the necessary info was taken from that already known by my issuing bank—that’s even easier than setting up Apple Pay. Maybe in some years to come you will have the same ability in the U.S.

We certainly can agree on one thing: PayPal—Ugh!

My understanding from reading the policy/privacy info from both Mastercard and VISA is that both share customer data with the merchant. In fact they both pitch better customer data as a benefit for the merchant, and this is with the contactless cards they offer. It seems that Apple Pay prevents the merchant from getting any customer data (probably one of the reasons some merchants don’t like it).

I’m no insider but my understanding is that Apple Pay is only an interface to Amex, MasterCard and Visa cards; Apple Pay is not a payment processor standing in the way as does eBay’s clunky “PreyPal”, so I don’t see why the use of Apple Pay would stop the credit card companies from sharing the resulting data with merchants; after all there is still a card and a merchant directly at each end of the transaction—no intermediary, like “PreyPal”; I think that it is only “Apple Pay” that is data neutral …

My understanding is that it is mainly the delusional merchants of the MCX consortium that don’t like Apple Pay, because it represents the credit card companies and not some cheaper form of payment service, such as ACH, which was never designed, nor intended, nor is suitable for the payment for goods that are going to immediately walk out the door at POS.

From what I’ve been able to learn so far, it seems Apple Pay is more like a pipeline between the merchant and the bank, and there is no opportunity for the card company to gather or share data as purchases are made, since all data is anonymized in real time. But when it is the contactless (or other) card from the card company being used, that data can be gathered and shared back to the merchant. VISA actually has a service for merchants to help them store and secure that customer data. And both Mastercard and VISA (and I would assume other card companies) make a point of promoting ‘better customer data’ as a benefit to the merchant. So they’re getting that data somehow and making sure the merchant gets it as well.

I think with Apple Pay it’s just the bank that has the purchase data, as far as that data being tied to you. Surely the bank must list the merchant name, the date, the amount, as you use Apple Pay. The question then is whether the card company also has that data. Maybe they do, but perhaps the issue is that since you used Apple Pay there’s no way for the card company to tie that purchase data to your account. The bank can because they are the other end of the pipeline. Interesting questions anyway. I’d love to find out more from people who actually know the technical details.

It does seem obvious that gathering customer data is a big part of how most businesses operate. Apple doesn’t need that customer data, so they have an opportunity to be disruptive on the privacy front.

EMV was never going to go anywhere in the in the U.S. either until pushed; and some of the idiot U.S. banks are talking a “chip+signature” model which defeats the whole purpose of the chip—they may as well stick to the mag stripe …

Steve, the fatal flaw with CurrentC (other than showing up way late to the party) is that it benefits the merchant, not the customer. The customer doesn’t give a —- about the merchant’s problem!

You say it’s not clear the backers of CurrentC know what they’re doing? I say they’re just plain blind to reality.

As best I can tell, Apple has already won this war.

Apple Pay operates only on the latest iPhones; Apple will never win this war because the majority of smart phones in the world are not, and are never likely to be, iPhones; and even then not every iPhone user will use Apple Pay …

Winning for Apple has never been about having the most users or most devices. I think that’s where a lot of analysis of Apple fails miserably. Winning for Apple is being able to deliver a great experience for their users (which in turn results in profit), and it does look like Apple Pay will be yet another win for Apple.

It also seems painfully obvious that Apple Pay is not the end of the road for the technology/concepts at work here. Apple is going to expand this into identity in many ways that deliver value to users.

“Apple is going to expand this …”

I assume that you are referring to the fingerprint ID mechanism, a concept that has been on the Samsung smart phone for some years; even eBay’s clunky “PreyPal” has been making use of it for some years but admittedly to little effect; then that is because “PreyPal” is clunky, not because of the phone …

I am not referring to the fingerprint ID mechanism. I am talking about the entire system Apple has put together, the fingerprint being only one part of the whole. Apple has created a secure pipeline and proof of identity which doesn’t only have to be applied between a point of purchase and a bank. There are many applications that are very interesting, and there is no scenario where this expansion won’t work because Apple doesn’t have the most users or most devices. That metric is not relevant to the discussion.

Oh, please, do explain it to me more fully …

Lucky for me, this has all been explained in great detail already, over on Asymco about three months ago in a discussion about Apple Pay. From a commenter named Martin:

————————-

Apple built a generic, almost foolproof device-level identity security system around TouchID, Secure Enclave, and custom secure element hardware at the lowest level of iOS that can be opened up to pretty much anyone Apple wants to let in. This is unique, and I don’t see anyone else who can replicate this. Apple is merely renting this security service out to the banks for the price of a percentage of the transaction. They don’t need to build a proprietary payment network, or even be a link in the payment chain. And this system can work equally as well for health providers securing user identity to exchange HIPAA covered health data for Healthkit (for a modest fee, naturally). They can rent it to employers to secure their employee identity – not just for getting into corporate applications but add HomeKit into the mix and a company can put an NFC lock on a door, issue tokens to the iPhones of the 10 employees allowed into that room, and that gives them the ability to unlock the door with their iPhone following a positive fingerprint check. The employer can remotely revoke those tokens as needed. This is effectively a way to replace username and passwords for anything from your iPhone or Apple Watch, if Apple builds it out to its full potential. It relieves the burden of choosing good passwords, remembering them, securing them, and puts all of the control on the agency that needs to control the security, rather than on the one being secured. The recent partnership with IBM might make more sense now.

Apple has spoken quite a lot about privacy the last few days. They’ve deleted their own copies of encryption keys that would let them get access to our devices. I don’t think this is coincidental, nor do I think it’s a message to users. I think it’s directed at the banks, health providers, and other companies that Apple is looking to build services for, telling them that they truly have a secure place in our devices to store identity credentials. And Apple can speak about not wanting to monetize our data, because that doing so would completely undermine the effort.

Apple patented this idea in 2009. They’ve been working on it a long time. The bought AuthenTec to get another piece in. Bringing their SoC work in-house helped to do this. They’ve hired countless financial services people to do this. And they’ve been working with the banks for at least a year on it, and I believe they’ve been running a closed subset of this system to secure their 800 million cards-on-file for several years (I believe Amazon is doing this as well).

This is much bigger than mobile payments and Apple’s head start is enormous. I think some cheap clones of this system are possible within 2-3 years, but I can’t envision a path for anyone to match, let alone pass Apple. Nobody controls the OS, SoC, sensors, and infrastructure like Apple does. Oh, and this should allow Apple to virtualize the carrier SIM. That’s important in many scenarios, particularly that enterprise one above. A current or future iPhone may be able to carry multiple virtual SIMs to allow it on multiple carriers. That’s important in some geographic regions, but it also allows enterprise to have clean separations of work and personal data. An employer should be able to have a carrier ID provisioned to them and then pushed out to a phone just like a token (or revoked), without any physical access needed. Apple has a patent on that as well.

————————-

Here’s the original link to the article/discussion as well, it’s great reading: http://www.asymco.com/2014/09/15/the-critical-path-122-where-the-money-is/

And you really think that no one else can do this? Dream on …

Did you read the comment? I realize it’s fairly long but it does answer your question. I certainly didn’t say no one else could do something along these lines, and the original comment also makes that point. Not sure where you’re getting that idea.

Of course others will follow Apple’s lead here but there are technical and strategic reasons why it will be difficult. No other company is as vertically integrated, and no other company seems interested in becoming as vertically integrated. Keep in mind that the tech industry, generally speaking, views Apple’s approach as wrong.

Apple is also in a unique position when it comes to dealing with customer data, Apple simply doesn’t need that data as part of its business model. Google does need to gather and use your data, that’s how it makes money.

However, the more others can copy Apple here, the better off we all are as consumers. Samsung may have an opportunity here, since they do make money off hardware. But they do still depend on Google.

Back to my original point, it isn’t terribly relevant whether others manage to implement systems that are similar to what Apple is doing. What matters is what Apple can do for their users. Apple also has the unique advantage of being the only company that sells iOS devices and Macs.

You asked how Apple could expand what they’re doing with Apple Pay, and I gave you a fair bit of info on that subject. There’s a lot of opportunity here for Apple to expand and deliver value to its users.

I have a Samsung Galaxy S5 and the fingerprint scanner is a joke. Works best with a pin. Just saying.. 🙂

Hi Doc; was it the fingerprint scanner or the “PreyPal” system, or both, that were a joke? …

It’s the finger print scanner. I don’t use PayPal. But i set my new S5 with fingerprint as the default login, but half the time it wouldn’t read my fingerprint. You get 6 tries then have to wait a few minutes before trying again. PITA!

After some trial and error i found that it’s too sensitive. If your finger is clean or dry when initially scanning it in it must be the same when trying to log in. I my case i washed my hands before adding my fingerprints to my profile, later in the day after being out and about it wouldn’t read them to log in.

Is beaming your credit card data to a machine more or less secure? I would think the latter.

The fact that you need a bulky, heavy case to use it is already a deal-breaker for me but more importantly Apple Pay offers a singular solution for NFC payments as well as in-app purchases (like the new iPad Air 2). With a Samsung phone you’ll have LoopPay for NFC-like payments and PayPal for in-app/online purchases.

Sounds like a lot of personal information spread across different applications and devices. I doubt even Samsung will be able to put a positive spin on that.

“… and PayPal for in-app/online purchases.”—Yuk!

Are you sure of this? Why would they use eBay’s clunky intermediary “PreyPal” when they could deal directly with the banks via “MasterPass” or “Visa Checkout”? Does not make any sense to me. And, a transaction via “PreyPal” is always going to be dearer for the merchant than directly to the payer’s bank via MasterPass or Visa Checkout …

Then, why would any payer chose to use other than their bank’s “MasterPass” or “Visa Checkout”, if they had a smart phone—other than an iPhone, of course ???

“PreyPal”. That’s funny!

PayPal (excuse me, PreyPal) and Samsung partnered up in order to bring online, mobile payments to the Galaxy S5. I haven’t heard/seen any reports on whether that’s been a successful venture but some PayPal executives are little salty about the deal because it now means they’re forced to compete with Apple Pay. Apparently PayPal wanted to partner with Apple and (somehow) be integrated with Apple Pay but that can’t happen now that they’re in cahoots with Samsung.

So, back to my original theory of having two mobile payment solutions when using a Samsung phone. LoopPay for on-the-go credit card transactions and another for online payments (and apparently via Samsung watches in the future), neither likely to communicate/share information so your sensitive credit card and/or bank account data will be in multiple places.

Yes, Yuck!!

source: http://www.businessinsider.com/apple-pay-and-paypal-partnership-failed-2014-9

You’ll have to excuse my ignorance; being a simple peasant, I don’t use a “smart” phone, so I had no idea what phone PayPal’s clunky mobile operation was running on.

Regardless, if you want to know how not well “PreyPal” mobile is going, ask a cashier at Home Depot the next time you are there.

“PreyPal” is a clunky, intermediary payment processor that rides on the back of the banks’ existing systems and charges its merchants more for the service.

Now that “MasterPass” and “Visa Checkout” are available, “PreyPal” is effectively redundant—except for its mandated place on the atrophying eBay marketplace, and as the merchant account provider of last resort for those very small online merchants that don’t have the confidence of their own banker.

Apple does not claim to be a payments processor; all they do is supply a secure interface to those card-issuing retail banks that have agreed to pay Apple a 0.15% cut of their share of the transaction fee that is payable by the acquiring bank’s merchants, a fee that would be less that that being charged by “PreyPal” to their “merchants”.

What point would there be in Apple accepting “PreyPal” in as a source of payers’ funds in addition to the accepting-banks’ credit cards when, in the main, “PreyPal” is then sourcing the funds from those same credit cards; then there is the possibility of “PreyPal” sourcing funds via the ACH system with the potential of a reversal the following day if the payer has insufficient funds/credit. No, I can well understand why a professional corporate like Apple would not expose themselves, and their partners, the agreeing banks, to PayPal’s clunky operation …

Again, MasterCard and Visa have recently launched online and mobile EMV/NFC wallets that will operate on any NFC-enabled smart phone (except the iPhone?); download one of these apps to your NFC-enabled Samsung smart phone, cut out the clunky middleman “PreyPal”, and deal directly with your card-issuing bank; the merchant will appreciate the lower discount fee too …

Didn’t Apple just accept preypal as a payment option in their stores?

PayPal works for the online store yes, but I’m not sure that’s for in-store purchases and frankly there’s really no need for it.

There’s a high probability that the majority of Apple Store shoppers own iPhones which gives them the option to pay with Apple Pay or via the Apple Store app that uses the iTunes credit card on file. Otherwise they just swipe a traditional credit/debit card.

Yes, but that’s not the same thing as letting eBay’s “PreyPal” leech ride on the back of Apple Pay …

Copycats! Samsung with all its mighty technological resources cannot come up with one paradigm shifting product. It is always copying some other company’s innovation and building around it, try various sizes, shapes and flood the market. I am surprised Microsoft has not taken off on e-credit card.

They came up with the finger-print scanner first …

No they didn’t, they copied Nokia.

Actually, it was Motorola on their “Atrix” in early 2011 …

http://www.dailymail.co.uk/sciencetech/article-1383133/James-Bond-Motorola-ATRIX-smartphone-operate-using-fingerprint-recognition.html

This is one of those things that some tech companies are obsessed with, but haven’t thought through. The problem in a nutshell: credit cards are better than a phone for this task. Easier, more reliable, and more secure.

This is snatching defeat from the jaws of victory. It imitates a “swipe” just when EMV is pushing all the merchants to chip-based transactions (transition for regular retail by next October).

And it requires an extra plug-in “thingie” that contains the “loop” that couples to the read head in the POS swipe slot. Another thing to plug and unplug, and get lost.

The fact that Samsung is planning to use this soon-to-be-obsolete scheme indicates that they’re even further behind the curve than I had thought. Way behind.

For the reason that the admin of this site is working, no uncertainty very quickly it will be renowned, due to its quality contents.

Wonderful post! We will be linking to this great article on our site. Keep up the great writing

Your posts never fail to enlighten me. Thanks for consistently sharing your knowledge and expertise.

Wow, marvelous weblog format! How lengthy have you ever been running a blog for?

you made running a blog look easy. The entire glance of your web site is wonderful, let alone the content material!

You can see similar here e-commerce

chrysler pacifica auto start stop warning light

hiukkassuodatin tukossa oireet

best center console boat brands https://twitter.com/consoleboat