The consumer electronics industry has always fascinated me. I spent my first ten years as an analyst covering the telecom industry, which historically has had very good margins. But, when I started covering the consumer electronics industry, I was struck by the fact the vast majority of players in that market make razor-thin margins, if they’re profitable at all. Even more striking is Apple, which might be described accurately, if incompletely, as a player in the consumer electronics market, makes telecom-like margins while competing with those barely profitable vendors. And just as interesting is the fact that, as players that have historically only competed indirectly in the consumer electronics business enter it, at least some of them are choosing to follow Apple’s route to the high end of the market.

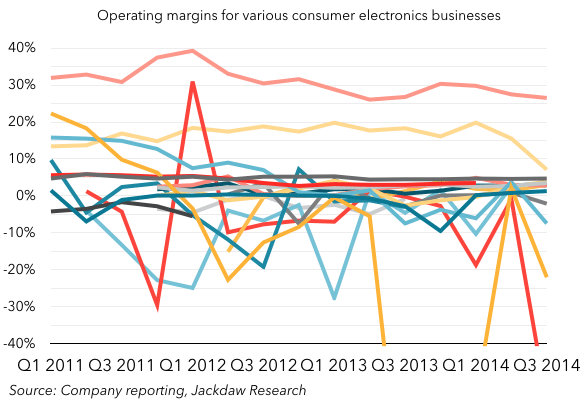

Historic consumer electronics margins are abysmal

It’s been quite a while since I updated this chart, but the broad picture it shows remains largely unchanged. It shows operating margins for most of the major companies in the consumer electronics business. The point isn’t to highlight specific companies, but to show the broad pattern of there are only two companies consistently above the 5% mark (Apple and Samsung) and Samsung was rapidly reverting to the consumer electronics mean (shown in yellow):

As I mentioned, Apple is the one exception to all of this, with between 25% and 30% operating margins during the latter half of this chart, while everyone else scrambles at 5% or lower margins. How does Apple achieve this distinction? Well, it’s due to a combination of factors but it’s probably best summarized this way: Apple provides premium products at a premium price, and is able to justify the premium through differentiation based on a tightly integrated approach to hardware and software.

Three new players: three different strategies

So far, we’ve largely focused on those vendors who make the bulk of their revenue from selling consumer electronics hardware. But there are three relatively new players in this business who have traditionally participated only indirectly in this competition and who are entering the computing hardware market (in its broadest sense) in new and interesting ways. Google and Microsoft have traditionally participated mostly by providing operating systems to hardware vendors, while Amazon has participated largely as a seller of other people’s hardware. Each of their strategies is unique and different but, with two of them, there’s an emphasis on the high end which I find interesting.

Look at Microsoft’s most recent hardware event: it announced the Surface Pro 4, a Windows tablet which starts at $899, and the Surface Book, a Windows laptop which starts at $1499. Both of those price points are well above the average prices in their respective categories and very much represent premium products. These (along with older versions of the Surface line) are essentially the only computing hardware products Microsoft sells, and they’re very much premium merchandise. In fact, the Surface Book starts at a higher price than the vast majority of Windows laptops on sale today and almost all the products announced by OEMs during the same period had lower prices. Microsoft is very much pursuing the same “premium product at a premium price” strategy as Apple and attempting to provide the same levels of optimization and integration as well (with mixed success).

Arguably at the opposite end of the scale here is Amazon, which has moved increasingly down-market with its tablet strategy. One of the reasons people were so surprised by the pricing of the Fire Phone was it seemed to fly in the face of the clear strategy Amazon had laid out with its tablet line: decent hardware at prices that undercut the competition. Since the Fire Phone launched, Amazon has lowered the prices for its low-end tablets even further and it’s increasingly clear this is the main focus of Amazon’s hardware strategy today. Yes, it has some “premium” devices too, but even these tend to sell at prices that fall much more into the mid-tier rather than the high end. I’m still unconvinced as to whether this is a good idea, as I’ve explained elsewhere, but there it is.

We come now to Google, who also had a hardware launch event this past fall and where its strategy was on display. Google’s approach has arguably been something of a mix of Microsoft’s and Amazon’s. Attacking the low end with devices like the Chromecast but also moving increasingly upmarket in the smartphone and tablet categories. There was no new Chromebook at this event but the only one Google has sold under its own brand so far is the Pixel, which retails at $1000, well above any other Chromebook. In smartphones, the Nexus line is an odd mix of Google branding and OEM manufacturing but even that line has been moving steadily up-market, while taking something of a cue from Amazon’s higher-end tablets, with premium hardware at discounted prices. But the product that perhaps signifies Google’s pursuit of the high end best is the Pixel C tablet, with high-spec and well-designed hardware, but at a starting price of $500, with an optional keyboard for another $150. In a world of cheap Android tablets, the Pixel C is as unrepresentative as the Surface Book is of Windows laptops.

The only Android and Windows vendors not struggling

Even though Google continues to pursue a low-end strategy with some of its own hardware, it’s increasingly clear that both OS vendors turned hardware vendors have decided to embrace the high end along with its high margins, while leaving the scale and the thin margins to their OEMs. Meanwhile, their OEMs continue to struggle to make the business work, with several exiting segments of the market entirely and several others clearly having a hard time staying afloat. Sony has abandoned PCs and continues to struggle in smartphones, HTC increasingly looks like it’s on its last legs as an Android vendor, Toshiba is considering spinning off its PC business, and Samsung’s smartphone business – once the poster child for success making Android phones – continues to slip. It sometimes seems as if the only vendors making Android phones and Windows PCs who aren’t struggling in some way are the licensors of the operating systems. And though we don’t have detailed financials for either company’s hardware business, they’ve both done it by focusing on selling premium devices at premium prices, and by tightening the integration between hardware and software.

What’s interesting is we haven’t seen any of the OEMs pursue this strategy. That likely reflects, in equal parts, a lack of capability and a lack of will, as these OEMs have neither the experience nor the desire to pursue the high end of the market. And yet it’s been clear for years that, while scale may be in the mass market, the margins are in the high end. These OEMs’ continued focus on the low end and mid-tier of the market, combined with their licensors’ focus on the high end, is likely to make life increasingly difficult as saturation and even decline begins to set in within the markets they serve.

I think that you are missing the upper end of the OEM’s product lineup. At least a few are successful at the higher end as enterprise machines. Certainly what they push on their consumer web stores and the brick & mortar stores is the low-end.

Some of them even offer a higher priced consumer notebook in the $1500 range, it’s just not the “starting at $849” model which has a paltry 4GB of memory with 128GB of SSD. The $1500 machine has comparable specs to an Apple machine although a this level of Apple notebook is going to reach more toward the $2100 range.

Not all of the $600 drops down to the profit line. I think one could easily prove that Apple spends a big part of that $600 on things that the PC OEMs don’t such as spaceship office buildings and more expensive engineering & marketing teams.

“I think one could easily prove that Apple spends a big part of that $600 on things that the PC OEMs don’t such as spaceship office buildings and more expensive engineering & marketing teams.”

Relative to annual cash flow, Apple’s $5B Spaceship Campus is not a high percentage drag on profits. The profit question on this campus will be answered over the next 30 years by what gets to be invented and delivered there.

“Not all of the $600 drops down to the profit line. I think one could

easily prove that Apple spends a big part of that $600 on things that

the PC OEMs don’t such as”

customer service that’s actually rather good, industrial design that looks and feels beautiful instead of cheap, and superior build quality.

Fixed that for you. Apple’s spaceship campus is 3 million square feet of office space custom built to enable Apple’s programmers and designers to do their jobs at peak efficiency. Find me a Corporate HQ of similar size, with a similar amount of landscaping, that costs less than 3 billion dollars (apple’s original budget). In the world of huge ambitious projects that experience cost overruns, an extra two billion isn’t all that excessive either, especially considering they had to sack their prime contractor partway in.

After spending a lot of years in the Android camp, I moved to Apple a few years ago just for those things you mentioned. I believe that Apple has more expensive design teams because they are worth more than the cheap teams.

I’m unconvinced about several of your assertions:

“It sometimes seems as if the only vendors making Android phones and Windows PCs who aren’t struggling in some way are the licensors of the operating systems.”.

?? We’re indeed missing any financials specifically for the hardware business. Getting nice-ish to raving reviews (and the occasional shoot down) is one thing, making money is another. MS have sunk billions in Mobile but even disregarding the past, their new phones are still purely a question mark; Surface also bled red ink for a long time, I have seen no info on whether it’s profitable overall or at runrate; Google’s Nexus is also a question mark (and only went high-end recently) and Pixel is so marginal I can’t imagine it’s making any money, but at least it’s not losing much either.

From where I stand, they aren’t struggling because they’re making their money somewhere else, not because they’ve cracked “being successful OEMs”.

“by tightening the integration between hardware and software.”

What are MS and Google doing that everybody else isn’t doing ? The fanciest thing I could think of is the Surface switchable graphics card, and that’s been available for years from nVidia and AMD. Ditto pen w/ pressure sensitivity… I’m really not grokking what you’re talking about. At best, they have a few new features implemented early because inside track ?

On the flip side, most of Android’s officially new HW+SW features have been available from individual OEMs way earlier than from official Android or Nexus: touch ID, pen, windowing, per-app rights…

“Meanwhile, their OEMs continue to struggle to make the business work, with several exiting segments of the market entirely and several others clearly having a hard time staying afloat.”

True, but at the same time, several new entrants are thriving. And not just in phones: Xiaomi is starting to make Windows tablets and laptops on top of Android phones and tablets and media players; LeTV and a litany of seemingly viable 2nd-and 3rd-tier OEMs are either doing only Android or Windows too. Did Kaypro’s demise mean anything for Wintel’s OEMs s as whole ?

“What’s interesting is we haven’t seen any of the OEMs pursue this strategy.”

?? Samsung is going relentlessly more high-end, now in materials as well as specs, as is Huawei (even their Honor sub-brand is ?). HTC Sony and LG aren’t backing down either. Granted, Lenovo and Asus haven’t graced us with a flashy high-end device, but they never have, so that’s not a recent change. Android had managed to avoid glass and metal phones until recently, now it’s hard to avoid even at the midrange. If anythign, what surprises me is the 1st-tier OEMs reluctance to fight for the low+mid range ?

Just curious: what makes the Galaxy S battery “undeniably better than the corresponding iPhone”? It’s specs? Maybe materials, or power efficiency per gram and cubic mm, speed of charge, life span, or what? And if not superior in every single way imaginable, who decides which metrics to use that makes it “undeniably better”?

Globally same battery life, but with fast and wireless charging.

So your article has me wondering a hypothetical. Assuming pricing is an important factor in premium branding, what would happen if Apple decided their cash horde was large enough, they no longer need to make the margins on their products they have and reduced prices to razor thin or even zero margin. But everything else remains the same, both in products and services.

Does that drive the price of premium level offerings down for everyone? Would there be a trickle down affect forcing mid and low tier products out of the market? Or do MS and Google depend on their own brand to keep their pricing higher?

I mean, this is even only possible as a hypothetical because of Apple’s cash on hand. And historically I would assume Apple has set the bar for premium pricing in the markets they compete.

Just curious.

Joe

Just as hypothetically, perhaps more so, I would guess (yes, guess) that part of the ‘aura’ of a premium brand is it’s pricing. The pricing is actually a vital part of the positioning. It’s also aspirational. You won’t feel as ‘special’ if Apple products are not priced the way they are.

So here’s my guess…

It will then become a spec game, which Apple will lose.

Thank goodness I’m not a gambler.

In what way would it become a spec game?

Joe

I base my hypothesis on that if there is not longer an aspirational ‘aura’, which is heavily influenced by price as a perceive value, then the value proposition changes to specs.

I say this fully recognizing that the game is much more complex than that. It’s the impact that one variable, price, plays on perception.

The natural evolution of abstraction and simplification and the shift to consumer-facing products and services means specs will continue to decrease in importance. Specs will always be important to a few, but when an industry becomes abstracted enough, consumers no longer prioritize specs. Example, did you know the horsepower and torque of your BMW before you bought it? For the vast majority of car buyers the answer is no. I might take the time to find out because I’ve rebuilt engines, but most people simply don’t care, because it no longer matters. At a certain point everything becomes good enough and the focus shifts to other factors, such as the overall user experience. This natural evolution helps Apple.

“consumers no longer prioritize specs”-Caveat Emptor

“did you know the horsepower and torque of your BMW before you bought it?”.

Yes I did. I knew it was a 2 liter turbo charged 4 cylinder 230 hp engine, 255 ft-lbs of torque. I could almost take it for granted that it would perform in it’s class, but that is what the brand stands for. If it didn’t spec that way, I would feel ripped off.

Addendum: If I were buying a Toyota, I would be even more aware of the specs.

But, do you understand that you are in an ever-diminishing minority? Do you know the technical specs of your fridge? Do you know all the various gauges of wiring in your home? Do you know the specs of the framing in your home? Do you know the sizes of pipes used in your plumbing, or the psi ratings? Do you know the details of how your attic is vented (if you have an attic). Do you know the details of how the roads you drive on were constructed?

I know all these things, and I can guarantee I know more about the details of the vehicles I drive than you, but I still understand that I am in an ever diminishing minority. The spec wars are over, and the industry will not move backwards, different pricing won’t change that.

I don’t want my computer to be ‘just’ an appliance. It’s too important, and too personal, for that.

Still, if my expensive refrigerator is actually a poor device, then I expect my HVAC or fridge guy to inform me. If I can get the same quality for less, then I will.

I know my wiring is up to code. Again, an informed party set those rules.

If a consumer doesn’t care, they do so at their own peril. That there are fewer of us that do, it’s to our benefit that we do. Based on what we’ve learned, some of us can choose to debate the merits or deficiencies of various computers.

PS-You ‘might’ know more about cars than me, but what makes you so sure?

“I don’t want my computer to be ‘just’ an appliance. It’s too important, and too personal, for that.”

Oddly enough, that sentiment is one reason why many technically minded people have tended to buy Macs — especially in the early 00’s — because they care deeply about their computers and their operating systems. If you care about computers, you probably don’t want to run Windows when you can run unix. But now that Sun no longer sells unix workstations, you’re left with either Linux or Mac OS X. And linux is legendary for its poorly implemented UI, for having places where you inexplicably have to go hunting through man pages or futzing with command lines or recompiling the kernel to do something simple like get a working sound card or get your networked printer to function. In the early 00’s, there was really only one choice if you wanted unix but didn’t want to have to waste your valuable time getting the OS installed and running on your hardware, and that was to buy a Mac.

Linux has gotten better since then, but it still can be challenging if your hardware isn’t perfectly compatible, and in some circles at least the consensus is that Linux is still not there yet and may never be there yet — after all, the corporations that have developers working on linux are interested in creating a server OS. So the Desktop shells that linux offers continue to be put together by volunteers in their spare time, with all that implies for quality, security, bugginess, and usability.

Well when we consider the early ’00s we have to put things in context. There was XP, Vista (yuck!), OSX and Linux.

OSX was, and still, is a great Unix. There is nothing wrong with Unix (that a good UI won’t fix) except prevalence of commonly used programs at that time. At that time Macs were more serviceable too, but still not where they needed to be vis a vis Windows hardware. You couldn’t get drivers for a lot of things.

I agree with you on Linux. I’ve compiled my own kernels, and once a year I revisit, only to end up not using it.

Since Win7, Windows is quite good. Yes, even Windows 8.

Being I’m a hardware kind of guy, and since there is no OSX outside of Apple hardware, and since Apple has pretty much sealed the hardware, they are generally out.

I did replace my Mac Mini, which I use as a media center in my summer home, with a Mac Pro (6 core). It’s my token Mac, and it’s the only Mac I would consider, though, it too, leave me wanting. It’s somewhat serviceable, but looks like an octopus with everything dangling off. I have it, should I need/want to use a Mac program.

There is no iMac, or Mac Mini I would buy. Not at the prices charged. For me, serviceability is up there with ‘experience’. It’s part of my ‘experience’.

Right. But there are so many other use cases. So many technically-inclined people are mystified by why anyone would use a Mac. They must be very ignorant people.

But in fact, many very techy people use Macs. They’re nice machines, the laptops made from solid aluminum. Great screens, trackpads, etc. They enjoy the highly polished OS, the GUI hiding the enormously complex UNIX beneath. I prefer the OS over Win or Linux, a personal preference. And I haven’t used Win except occasionally for games since 2002. No desire to build my own systems, either. That’s where I’m at. And I used DOS starting at about 3.3 and Windows since 2.0.

It’s a large and diverse world. And that’s okay.

I’m not sure I’d call the MBA screens “great” ^^

Neither would I. That’s not their only laptop line.

Yep, but you didn’t differentiate. That type of over generalization mightily skews opinions…

That’s a very common phenomenon, to paint with a broad brush. Not that ext2bot is doing this intentionally, but it’s a trait of what Brian Hall calls the ‘Echo Chamber’.

That’s worth pointing out though. We had the reverse exchange a while back with another commenter who wrote “Asus makes crap”. That is true, but they also make non-crap. It’s fascinating how Apple manage to control perceptions this way, and others don’t.

The interesting thing is that you don’t seem to consider all the criticism of Apple in the press.

ZD Net and Slasdot for ex. have plenty of criticism for Apple. There are myriad comment-section pundits across the net who can’t think of any use-case for Apple products.

I, myself, have several criticisms of Apple:

–Prices are too high (chop $100 off low-end and more off high-end computers, lower list price of phones by $100)

–Relax App Store restrictions to a certain extent with exceptions for top utilities (I’d love to be able to use DiskWarrior on my phone, for ex.)

–Don’t be quite so stingy with RAM and storage across the line, especially now that most devices’ RAM / storage can’t be upgraded.

I’m sure you have criticisms of your favorite brands.

I don’t really have favorite brands, jut preferred-at-the-time devices. I’m actually wondering if I should make a list to help me not forget any feature next time around, choice is a blessing and a curse .

Early on I bought Samsung stuff because it was the only one with no horrendous drawback (camera, battery, screen, build quality, SD), then they went a bit crazy with pricing and stopped making ever huger phones, so I switched to a 6″ and then 7″ Huawei. They’re good, but not excellent: the last one is missing an FM radio, the promised 5.1 September update hasn’t arrived yet, the camera is good-not-great, the performance is bearable not good…

I skipped upgrading this year, I would have gotten a Nexus 6 (but battery) or an LG G4 (that one ticked all the boxes even wireless charging, FM, tap-to-wake, and the camera +app on the G3 was already excellent, the G4’s is even better… but 5.5″ only).

I’ll certainly upgrade next summer, but that will be “extended choice” again, no shortlist based on brand. Probably first-tier though, and then a cornelian choice between flagship or huge… I’ll agonize for a bit, then choose huge. Huge flagship anyone ?

Or, better yet, restore user maintainability…

It’s not that “Apple” controls perceptions. It’s that there really is a pretty consistent level of expectation/experience/satisfaction right across the “Apple universe” and its users, regardless of who those users are, their level of experience, or how large the user base gets.

That’s why you cynically think there is some kind of cult, and that Apple “controls” perceptions. But, of course there is a pretty consistent level of expectation/experience/satisfaction right across the board with Apple, because that is what proprietary, integrated software and hardware is all about!

So, it’s Apple on one “side”, and everyone else on the other, whether iOS vs Android, or Mac OS vs Windows. Which is great for you when you want to lump all the good things about Android or Windows together (regardless of whether that is a relatively rare experience across the whole Android or Window’s universe); but not so good when you are trying to poke holes in the consistently high customer ratings Apple gets across the board.

Of course, MS and Google try to manage their own perceptions. They’d love to, but they can’t; because, with all manner of OEMs who care about different things to different degrees, there is a real mixed bag of experience across the entire user bases.

The idea was that the MS world represented “compatibility”, while Apple did not. That was the “perception” for decades — still is, being as how “drivers” were mentioned above. But the fact is, I can still plug almost any (decent) peripheral from any company in the world into my Mac with a higher level of expectation out of the box than most Window’s users. Many people I know (no doubt less experienced than yourself) have tons of issues when they upgrade Windows, or change from a device they had taken time and effort to configure — they feel like their drivers and peripherals just don’t work any more. Same again with docs — I get Windows users sending me Word or Excel docs they’ve been given, asking me to open them on my Mac because they couldn’t open them, then resave and export them, and send them back so they can open them.

I’m just wondering where this perception of “compatibility” comes from, and how it is that MS controls it so effectively. Hmmm?

“I’m just wondering where this perception of “compatibility” comes from, and how it is that MS controls it so effectively. Hmmm?”

Well, mostly because it’s true:

– what do you do when an iOS user wants to send over an Apple Office doc to a Windows user. Save it as a PDF ? What about edits/collaboration ?

– Windows supports 2 or 3 or 4 orders of magnitude more devices and peripherals than iOS. You can’t even get a decent gaming vidcard on an iOS computer !

– have fun connecting to non-Apple equipment. My iBrother’s NAS has to run specific apps for Apple, because the apps everyone else uses (Windows Android Linux) either don’t work or are a pain to set up.

Do you mean that if I say anything positive about Apple, I’m part of Hall’s echo chamber? (And that’s not to even mention the enthusiastic anti-Apple echo chamber!)

Hall was complaining about certain tech press trumpeting unsubstantiated numbers re: Apple Watch sales. I don’t think in that situation it would be too difficult to estimate Apple Watch sales anyway. Wait for earnings, then look at change in the category that includes the Apple Watch.

The only thing I could see in my comment that might need to be substantiated is the claim that lots of Mac users are expert users. If you disagreed, though, and claimed that most Apple laptop / desktop users are novice computer users (that perhaps are getting ripped off b/c they don’t know specs), you would need to substantiate as well. Right?

I actually ruled you out and called others part of the echo chamber. Sorry if I wasn’t clear.

Oh, I see. My mistake. I think the general theme is anti-fanboyism. And I agree with that.

I admit that I tend to stick with Apple stuff, but I certainly don’t think they’re the be-all and end-all. The advantages I’ve had with sticking with Apple stuff is that the devices are generally very reliable and well-made.

One disadvantage is that, until recently, Apple wasn’t putting enough RAM and storage in their devices. For MacBook Pros, that *was* easy to rectify by puttin more RAM and Drives in them. With the new laptops, that’s impossible.

For the phones and iPads, insufficient RAM meant I could only open a couple browser tabs at a time (or they would reload the pages). On fast connections, it’s not a problem, but on my crummy satellite Internet it is.

The newest phones and iPads now have 2GB, allowing over 20 browser tabs without refresh due to memory pressure. 2GB is more than it may seem because iOS uses ARC instead of traditional automatic garbage collection. Less overhead.

It was actually specific to me, to the laptops I would buy, either a MacBook Pro or possibly the new MacBook. Both have very nice screens.

Apple does need to update the Air screens. The MacBook is the blueprint for future Airs.

” If you care about computers, you probably don’t want to run Windows when you can run Unix” ? Why on earth would that be ? And why on earth would Apple’s rather proprietary version of a Unix variant be preferred in that case ?

“I know my wiring is up to code.”

Exactly. It’s good enough so you no longer think about it. You don’t need to care about it, and no ‘peril’ exists in this regard.

“PS-You ‘might’ know more about cars than me, but what makes you so sure?”

One can never be sure, but I grew up on a farm, started driving when I was 8 years old. By age 12 I was trucking grain and operating heavy machinery of all kinds. I’ve rebuilt a number of cars and trucks and done quite a lot of mechanical work on all kinds of farm equipment. There aren’t many people that have the same experience re: vehicles, other than the people I grew up with (other farm kids). Now, if you happen to be a licensed mechanic, that’s a different story.

But I digress, that isn’t the point, whether I know more or you know more. The point is we’re both in the minority when it comes to caring or knowing about ‘specs’. Abstraction is the future, whether you like it or not.

It’s your future, it isn’t necessarily mine, unless I’m not given a choice.

When I purchased my house, just like everyone else, I hired an expert as my proxy to ensure the house was up to code, among other things. So yes, I most certainly cared. Anyway, the bank required it.

Abstraction is *the* future, I’m just describing reality. Although there’s a good chance that modular systems will allow for a good range of choice for those that want it. But it will be a small segment. I can still build a hotrod if I want to, it’s just that almost nobody does that anymore.

As for construction codes, minimum code isn’t always great. I built my own house, far above code. It doesn’t cost much more. Even building it yourself the project is subject to all the same inspections and codes, it has to pass.

“I just want to make you more careful. You know what you know, you don’t know the other person.”

Knowing what I know is why I was pretty confident I was right about where we stood re: car knowledge. I was already being careful, but thanks for your concern.

“Addendum: If I were buying a Toyota, I would be even more aware of the specs. If my BMW were priced like a Toyota, even more so, I would get suspicious.”

Interesting. Now apply that to computer buyers instead of car buyers. Like Space Gorilla said, you are getting close.

Now suppose, that were the BMW to drop to Toyota prices (just because it could afford to), and you became “suspicious”, why would you think that BMW would have to compete with others at their spec game?

The BMW would still be the same BMW — build quality, performance, etc. As you said: “I could almost take it for granted that it would perform in it’s class, but that is what the brand stands for.”

The others would still not be able to compete with the BMW on build quality, performance and all the things BMWs had come to be known for. So, what would they do? Play the spec game even harder and throw in even more specs — free sun roofs and cup holders, electric this and electric that…

So, yeah, there would be loads of people bamboozled by those specs. But, fortunately, there are lots of people who just like to drive.

You’re ignoring other things. In this case the ‘cars’ all use the same engines, suspension systems, etc. We would be arguing over upholstery. If a non-BMW is more ‘moddable’ it can kick the BMW’s butt.

You’re relying on false equivalence again. Here’s how I summed it up for Naofumi about a month ago:

“From a buyer’s perspective what I want from my computing products is: closed and curated, abstracted and simplified, a whole solution from wrist to pocket to pad to desktop from a single vendor, all well supported (including a good retail presence), well-designed, integrated services as well as hardware/software, quality build/materials, and safe, secure, private. Who else in tech is even attempting to offer this? Who can even afford to try? Is anyone else in tech even motivated to offer this, given that much of the tech industry views Apple’s approach as ‘wrong’?”

This is the user experience I value, it affords me more freedom and control, it meets my needs best. As you said: “Who are we to judge what others value?”.

It’s not for me to judge what you value, other than how it impacts me. As a consumer, I criticize Apple over exactly what you value, because Apple offers no alternative.

You should have stopped at “It’s not for me to judge what you value.”

That would make me a sycophant.

No, it would simply mean you were actually sincere when you said “It’s not for me to judge what you value.”

I was perfectly sincere. Thank you.

Nonsense, you show no respect at all for what I value and the choices I’m making re: Apple products. You continually argue that Apple’s approach is wrong/bad/harmful/etc. Wow, you just added to your other comment and proved my point: “other than how it impacts me” and so on.

I could do the same with your BMW, simply because that vehicle is a terrible choice for me and doesn’t meet my needs and doesn’t offer what I value. I could rant and rave about how bad BMW is and all the things that are wrong with their vehicles. But I don’t, because I actually do respect that other people value different things. This conversation has become pointless. You seem unable to think outside yourself.

I don’t speak for you SG. Just as it’s not for me to judge what you value, it’s not incumbent upon me to defend what you value. I speak for me and what I value. You value exclusion of my needs and wants, when it need not be this way.

If Apple were to offer a tower Mac Pro, fully user configurable, that would bother you? Or would you just choose a different model?

If there were an iPhone with a SD slot? Alternate stores for Apps?

What would change for you? Curate yourself by shopping only at the App Store and buying the curated models. Since there are no other type, that is what I criticize.

And you just proved my point again. You have no respect for what I value. None. Please have the last word. I’m out.

You’re right. I have no respect whatsoever for what you value. I would not deny you though.

Ignore

That’s what choosing between models from OEMs is: arguing over upholstery. That’s the “spec game”.

But I hope your BMW doesn’t have the same engine and suspension. Why did you buy it? When you say, “that’s what the brand stands for”, what are you referring to? Not the upholstery and cup holders, the intangibles that Obart denies.

Now, it may be that BMW’s engines are less proprietary and differentiated these days than they used to be (maybe even less differentiated than Apple’s silicon is from others’); but I sure hope you expect your BMW to out-perform cars one-third to two-thirds its price.

Why did you buy it?

a) The same engine… does not apply to cars, it does apply to computers.

b) I like it.

c) I don’t defend them. I’m not a fan, and their cabin layout totally sucks.

I do expect a $2000 computer to outperform a $1000 computer, but lo, the 27” iMac sports an i5!

a) And all computers use electricity, silicon, 1’s and 0’s, so? The OS, however, isn’t the same. And, that makes all the difference.

Perhaps the OS has a different set of priorities, or lays off more on the GPU, or something intangible like that. See, You and OBart want to dismiss that OS X makes any difference. But then, Obart is wanting us to imagine Apple used Android or Windows. Well, then, sure, we could say everything has the same “engine” and it only comes down to the way the door feels when it slams, or the cabin layout, or whatever.

But right now, having hardware integrated with proprietary software (however similar some of the hardware elements might be), is exactly what delivers the experience and expectation that is selling premium Apple products.

c) so, your BMW isn’t a “premium” product because it doesn’t deliver the cabin layout that you or the next guy might expect in a “premium” car. Well, if I had a BMW, I can tell you, I would certainly expect that it better have the cabin layout that fits my every conceivable need.

The iMac probably does more with its i5 than most Windows OEMs do with i7’s in most models that have them. Remember, the Formula one car is restricted to 2.4L (I think). Man, if I paid a cool mill for a car, I’d expect it to have a 12L engine, at least! What are they thinking?

I get a free mediocre Mac with an i5 attached to a sensational screen, that I can’t use as a monitor…

Anyway, I wasn’t referring to the 5K iMac. I was referring to the 27” iMac, which apparently has been discontinued.

And what’s with the spinning drives???

Post Jobs, Apple has never played a feeds and speeds game. So your hypothesis is that Apple’s only premium differentiator was a higher price and once gone is no different than anyone else’s device regardless of software and ease of use? People paid money for their own customer satisfaction? That’s interesting.

Joe

Like I said, it’s not a one dimensional problem, but think of it this way…

The customer that buys on price tends to buy on spec (I think). I buy on spec at any price, intangibles come second or third. So that customer says ‘I’m going to buy an iPhone’, only to be told by someone like me, ‘Why? You can get more for the same price, or the same thing cheaper.’ Experience is hard to quantify, and there is good enough, just like with specs.

But you don’t think a 25% price reduction answers that?

Joe

I’m with you. Pick a sufficiently small number. 25% of $800 is still a $600 phone. Is that enough to prompt a price war? Probably.

Incorrect, the user experience can never be good enough, this is why Apple will be very hard to disrupt.

There you go proclaiming again…

An Android at $200, full price, may well give a more than good enough experience for the money to many people. Who are we to judge what others value?

You’re starting to get it, I think. Most of the market doesn’t value the kind of user experience Apple delivers. We see this in your good enough $200 Android device, which isn’t far off from the majority of Android sales (I think the ASP is around $250 and falling).

But, there is a good-sized segment that does value what Apple is delivering re: user experience, and they aren’t going to suddenly shift from Apple to your $200 good enough Android device. The user experience and value being delivered are quite different. That said, many pundits don’t understand this, or won’t admit it, and use the logical fallacy of false equivalence to say “Oh, as soon as people realize they can get the same experience for less on Android devices, Apple is doomed.”

Then I must admit that I’m confused. Which is it? There is such a thing as good enough experience or isn’t there?

Switch gears now to premium. I will almost always go for premium spec regardless of price. To my reply to jfrutral, if Apple drops prices significantly, thus forcing others to drop prices significantly as well, then the others will have to match price AND out-spec Apple to compete, and for me that’s a good thing. And I don’t care if it’s Samsung, LG, Moto, HTC, Nokia, etc. No loyalty.

“Then I must admit that I’m confused. Which is it? There is such a thing as good enough experience or isn’t there?”

But you’ve already answered your own question when you said “Who are we to judge what others value?”.

Think about what you said there for a minute, and then think about market segmentation. You’re so close to understanding this, I think.

But it’s you that said the user experience can never be good enough. Now it appears you say it can.

Exactly. It depends where you find value within your own experience.

Then don’t make absolute statements. ‘Incorrect, the user experience can never be good enough’

It is a true statement, the user experience can never be good enough. But not everyone values the user experience in the same way, and not all user experiences are the same. It’s not either/or, there’s no us vs them here for you.

I see, it all depends on what the meaning of the word ‘is’ is. Homage to Bubba Clinton, I loved the guy.

Sigh, I thought you had it, but you just don’t get it.

ha it ever occur to you that a huge chunk of the 80% who brought an Android phone do so because it provide a better user experience to them than an IPhone?

Yes. That’s exactly right. Different people find value in different experiences, and that’s fine. When it becomes a problem is when we attempt to apply our own values to an entire market, or deny that value exists because we personally don’t value a similar experience, or when we use the logical fallacy of false equivalence to argue that two different kinds of value/experience are the same.

This seems to be what you implied when you focus only on price when talking about Android user as if the only reason for their purchase of an Android Phone was because the iPhone is out of their reach

Not at all. There are many good reasons to buy Android instead of Apple. I’ve said this many times. But the reverse is also true, those of us that choose Apple products are doing so for good reasons.

i agree

The nice thing about user experience is it cannot be measured, so they can harp about it till the end of times.

A nice user experience is… having apps that crash more, using 80s icons instead of widgets, no choice of keyboard, launcher, browser nor default apps. You just have to state that *that* is your version of “a superior user experience”. Plus it’s more expensive, so that must be true :-p

I understand that this is maybe practical only in the US where contracts were the norm, but I just bought my daughter a new 6S for $100. Is Android so much cheaper?

Speaking of specs, the 6S has a highly competitive microprocessor and gfx procs. The screen res on the non-plus ain’t great, but overall the specs are very competitive.

There was a time after Jobs died when Apple drifted a bit (taking forever to bring out bigger screens, for ex., and the OS languishing). That’s not true any longer.

iOS and Android both have unique strengths and unique weaknesses, I understand. But to say that Apple’s phones don’t compete on specs? Macs are in a somewhat different situation. They don’t compete 1 to 1 on specs, but that’s a different conversation.

First of all, Jobs is not dead.

His so-called “death” was an elaborate hoax designed to get movie studios to make biopics.

Meanwhile, Apple is building a death star. It runs on Windows 10. Once everyone has updated to Windows 10, it will become operational.

The Alliance knows this. That is why they resist upgrading.

More will be revealed in Spec Wars Episode Eight: The Kindle Uprising. In theaters, Spring 2017. No spoilers!

It’s a trap!

Oh great! The ‘Elvis’ Jobs…

As long as people commit to multi-year contracts for inflated prices and don’t realize they’re way overpaying for their phone that way, price differences will have no impact, indeed.

Is it more? My bill was the same after buying a contract phone as it was before (Verizon). Now, having said that, the new (for Verizon) installment plans look like they’re cheaper. Looks like paying for an iPhone in installments would be roughly comparable to the old-style billing but with the addition of unlimited texting. Cheaper phones would obv. be less.

Verizon is the best choice for me as I live in the boonies.

How much is you monthly rent ? How does it compare to Veruzon-based MVNOs ?

Your answer does speak to why cheaper makes no impact though. As you say “my bill was the same”. Mine went from $100+ to $20 over 5 years….

How do you pay $20/mo. for a smartphone??

Good question. I have an unlimited data plan, so I’m not giving that up willingly. The rest of the family could, I suppose.

It looks like we’re paying a *total* of $60 per phone. So, that would be very roughly $50 before taxes and fees. All phones on contract. We may eventually switch away from contracts if it proves less expensive. As I wrote above, only Verizon has reasonable coverage out here in BFE. I don’t know much about the MVNOs.

There’s a list of Verizon MVNOs and contracts there: http://bestmvno.com/verizon-mvnos/

I can’t say w/o knowing you contract details, but an MVNO’s 300 minutes/unlim text/1GB is $20. If that’s what your wife has, she’s paying $100 + ($50-$20) x 24 = $820 for her iPhone. Roughly: fees and taxes ignored on both sides.

She had 2 gigs for her phone only until recently (now 5).

That $20 sounds great. That includes an iPhone for $200 or less? I’ll take a look.

Where did you find a 6S, full price, for $100, and can I buy ten of them?

Please re-read my message. You’re mistaken.

I definitely buy for the Apple experience and ease of use, not for specs or the idea that price makes me feel special. If I were interested in Specs I would have switched to a large screen Samsung phone before the iPhone 6 was released but I didn’t, I waited for the iPhone 6. I did this because the user experience, ease of use, software updates etc is one that only Apple with its closed and completely controlled OS can provide.

Yes, but you also don’t buy on price either.

It has never been a “spec game” for Apple. It has always been a “customer experience game”.

If your hypothesis is correct, then Mercedes Benz, BMW, Miele, Prada, Tiffanys etc. should have disappeared a long time ago.

If we imagine a world of unicorns and fairies in which Apple gets bought and taken private, and the new owner says to them, “I don’t approve of being greedy. 15-20% margin is enough for me,” then I think that apple’s products would become cheaper, more people would be able to buy them, and they would become an even more dominant player in the world of technology.

Cutting margin to zero makes no sense whatsoever. Just one example of why: with zero margin, you no longer make any profits at all, which means you are no longer able to pay your programmers with the profit sharing incentives that are mandatory in Silicon Valley to retain talent. SO your best employees jump ship, and you are no longer able to deliver high quality software for your gadgets. Which might be a clue as to why the bundled software made by most hardware OEMs is so poor.

Healthy margins enable the company to be healthy at all levels, not just the profit-loss column. There is a range of healthy margins (in between “company is starving” and “company is greedy”), and Apple does indeed put itself at the top of that range. But cut margins too much and you can no longer afford things like customer service or employee profit sharing, you enter a downward spiral towards where the PC clone makers have been living for the past decade or more.

Sure, “hypothetical”, right? This isn’t really about margins, except that Apple is probably the only company who could afford, even long term, to cut margins. So pick a level of cut, I don’t care. Although I think in order to parse out what premium means and how price affects it and the broader market, one would have to at least hypothesize at least razor thin margins of the competing mid-low end.

The article talks about high-end premium as delineated by price and most agree, until the recent entrants, owned largely by Apple and Samsung.

Using Samsung as an example for the thought experiment is tough because they also compete in the mid and low-tiers and are already retreating to razor thin margins that won’t likely impact the over all market.

So if Apple definer of high end premium cuts the entry price carte blanche, without an actual entry model, what does that do to the perception of premium in the general market and Apple specifically? Does that not automatically put pressure on the whole market?

Would Google and MS need to reduce price, too? Or are their OSs sufficient differentiator and let them say “If you want premium, you have to go with us”.

But if the only thing premium and high end about Apple was price, then how do they continue to own the high end?

Joe

So let’s be generous and say Apple’s margins are easy enough 30% (the high end of Jan’s measurement) and let’s say the need to keep it above zero, let’s say a 5% margin, a 25% cut.

I could be misunderstanding “operating margin” (it isn’t always easy to keep all the different “margins” straight for me) but let’s say that results in an across the board 25% price reduction in products. Would that simply devalue Apple’s brand and tarnish sales in both directions (low and high)? Or does that immediately put pressure on both ends? Does price directly dictate premium, high end?

Joe

I don’t think the reaction to that would be monotonic: I’m sure some customers are driven by cachet, other by hardware, and others by software, and would react accordingly to lower prices.

Instead of cheapening the main brand, creating a sub-brand would probably make more sense. And making sure it’s both cheap-looking and under-specced so 2 of the 3 categories don’t switch down. Also, that move only makes sense if extra sales make up for intra-Apple switchers, and/or if ecosystem sales make up for lower revenue+margin.

I’m wondering what the impact on the second-hand market would be though.

I guess that’s one of the questions i am getting at, does it cheapen the brand? Or does the definition of premium shift?

BMW and Mercedes cheapened their brand when they made cheaper cars, but not just in price, but in what they offered for their price. What would happen if they had just lowered their prices? Does it lessen the premium brand or does it force other premium makers to reciprocate? And what of non-premium brands? Do they need to lower their prices, too?

Two other non-tech examples that always make me wonder about pricing:

The media industry hates “free”. They say the music or movies or TV shows have value, and by that they mean economically, that is erased if the product is given away. So Taylor Swift holds her music back until the outlets pay more.

Yet, at least in the old days when media came on physical product, they loved variable pricing to drive demand by lowering prices for a time being. Movies would also vary as to when they are available. Disney releases for a short tie then stops so they can re-release at a later date with fan fair. To me this does not speak to intrinsic value. This is just economic gamesmanship. The intrinsic value of media really does not depend on what people charge. If the work is meaningful enough people will get it.

Minimum wage. Don’t get me wrong, I am all for people making a living wage. But the affect of raising minimum wage does not automatically equate to lower income people being able to afford the things they couldn’t before. There is a trickle up affect, too. All of a sudden people making just above minimum wage are making minimum unless their wages are raised. Rents go up as landlords figure the tenants can now pay more. Etc. Things get more expensive even as everyone starts to make more. Minimum wage then does not define affordable living, no matter how much we want it to.

So if the premium high-end tech device maker who has shaped what premium means, particularly in pricing, decides price will no longer be dependent on their margins, then either the definition for high-end premium shifts or nothing changes and they weren’t really premium to begin with.

So then what really defines premium? Is it pricing? Or is there something more intrinsic, meta-monetary?

Joe

First, I don’t think content works the same way as hardware: marginal cost is essentially 0, there is no resale market; but there is lock-in (Disney fans ^^). The way I understand it, content first banks in full-price sales, then tops up the revenue and recruits more fans by reaching impulse purchase prices, then cycles high-low for a very durable long tail. iDevices cannot go into impulse buy territory for cost reasons, and to avoid ruining the secondary market, and the long tail is way shorter. Lock-in still applies though.

We’ve been struggling with the definition of premium for a while. To me, it’s too vague, and can mean:

– Expensive. Some stuff sells simply because its price signals you can/want to spend that much. Lots of teens clothes are that way, crummy t-shirts with the right logo, special-issue snickers… people like $500 wine way more than $5 wine, even when it’s the same. We can decide premium phones are those above $500, regardless of why.

– Luxury. Not quite the same as expensive, though both are linked. Luxury means a focus on quality of process, product and service, and carrying values beyond the mere usage value of the product. The brand justifies the price as much as the actual product. It’s clear Apple are working that angle, though how that can get any traction for a product made by quasi-slaves, with no hope of lasting more than a handful of years, made from materials that are literally run off a mill is beyond me.

– High-specced: some stuff is just faster, more powerful, more durable, more capable. Maximizes usage value, even if that means a higher upfront cost.

Right now, Premium seems to be defined as a combination of those 3, mostly 1 and 3, with random weights. The funny thing is last year’s premium phones compete with this year’s midrange (at least in the Android world). I really don’t know if they still count as premium.

Yeah, I’ve never seen anyone try to compress the economic model. It either expands (by continually raising the top end and continually redefining highend by price) or simply just shift the model by raising the floor.

Not to mention all the discussions about “People only perceive value if they pay something”. Well, Google is going to great lengths to blow that notion out of the water (sans hardware, apparently). I’ve never believed that anyway.

Joe

Re: Edit: you’re right it does, if others don’t follow. Apple becomes a value brand ^^. that’s in theory though, in practice I’m sure we’d see Samsung splitting ranges into an Apple-matcher and an Apple-bester and try to play both sides.

As for value being only perceived if it’s actually paid for, I’ll ask my shrink ;-p

It’s a fascinating question though, because phones are both handbags and TV sets. The handbag’s value is in the label, the TV set’s value is not at all in the device but in what it shows (Ill take a good show on a bad TV over a bad show on a good TV anytime). And device and Content seem to follow different value rules, I don’t think price affects the perceived value of content much. Probably because you can’t show it off. Google is in the business of selling content; apple sells devices.

Few more things to premium/luxury:

1. It lets you connect or be part of an “exclusive” group. Sometimes it is achieved by being expensive, but other times you limit access – to achieve premium (with high price as side effect).

2. Cultural meaning. Some things carry a shared cultural meaning and you buy it to be seen with that meaning. For example diamond rings became known as a symbol of commitment.Through enough ads you can create meaning to random things. So wearing NIKE means you’re an achiever etc. This meaning can also be a self meaning something that if you believe in ,helps you change your emotions and your psyche, motivate yourself, etc.

Apple was always strong in that. It had always had a cult like following ,and they we’re very wise to always transform long periods they had product leadership into cultural meaning about their users. And that kinda stuck .

One interesting question though: how do you “disrupt” a luxury brand ? is it just by better breakthrough products? or is there an option that doesn’t require that ?

The question that comes to my mind after looking at your chart is: how far back in time does this trend of hardware being sold on razor-thin margins go?

I have the feeling, based on my memory of system costs and component costs, that 20 years ago, margins were significantly higher, especially for brand name companies. There was a time when you could build your own PC for quite a bit less than the cost of buying it in a store. There was a time when the customer service provided by name brand OEMs was something other than a complete joke.

So I have the feeling, without more than anecdotal data to back it up, that Apple’s margins aren’t all that out of line with the margins that used to prevail in the industry among the name brands (Compaq, HP, Dell, IBM, etc), before all the other OEMs made the mistake of trying to compete with white box brands on price instead of competing on service, support, reliability, and the like. In other words, Apple held the line on margins while all the others succumbed to a foolish price war.

They had no choice but to succumb to a price war. People bought on specs, and yes, the OEMs didn’t have the imagination to be better. Compaq, in particular, was extremely arrogant, and somewhat proprietary. Apple was totally incompatible with everything else, and highly proprietary, and expensive, and they almost died. Only when they switched to Intel, and adopted more interoperable systems, did they take the turn.

Even today my ~$5K home-built (in stages) desktop blows away my $4K 6-core Mac Pro and is competitive with the $10K model (if you trust Geekbench). I moved video cards from my older desktop (which I still use) and that accounted for $2.2K of the $5K. It’s also much more configurable and serviceable.

Anyway, I think we agree that the ‘foolish price war’ (foolish for them, good for me) was basically a price/spec game.

“Apple was totally incompatible with everything else, and highly proprietary, and expensive, and they almost died. Only when they switched to Intel, and adopted more interoperable systems, did they take the turn.”

Nah. They “took the turn” immediately Jobs came back, years before they switched to Intel. What Jobs did was carry on with precisely what he wanted to do a dozen years before, when he was ousted.

He immediately scrapped most product lines with incomprehensible naming schemes like everyone else’s naming schemes, and focused on three or so product lines — all Mac, where he knew the future of the company to be. Other Apple execs had wanted to continue to milk old cash cows, and had wanted to sell the Mac at a far higher price point than Steve wanted to.

He was also in favour of more compatibility, not less. He pushed for Office on Mac, and standards for networking and connectivity like USB and ethernet rather than AppleTalk and ADB/SCSI, etc.

The internet at that time also helped. I remember living through that, suddenly it mattered far less whether you were on Mac or Windows since there were standard file formats because of the net.

History, timelines and facts are apparently invisible, irrelevant or easily rearranged.

The first thing Jobs did when he came back was disallow the licensing of Apple operating systems, the old leadership had in fact begun to open up the Apple brand to other manufacturers and Jobs stopped that immediately when he returned

“In 1994, Apple began licensing Mac OS

to a handful of select vendors who paid Apple $80 per machine to use the

operating system. As the years went by, it became apparent that this

wasn’t such a great idea. The clone manufacturers produced relatively

low-cost machines that cannibalized Apple’s most profitable product

line, and the clones did not have the intended effect of significantly expanding the footprint of the Mac platform”

By 1994 it was way too late. Wintel won the desktop by then.

I’m pretty sure Apple is making the most profit of any PC maker at the moment, from Macs.

A manufacturer’s profit plays no positive role whatsoever in my purchase decision. In fact, if anything, their profit runs contrary to my interests as a buyer, as described by jfrutral’s hypothesis in this thread.

Although I too do not have data, I agree that profits were probably higher before. Not uniformly, but those that did have competitive advantages, like Nokia, Blackberry for example, most likely had OK margins. Same goes for IBM and others.

Price War however is a bit more than foolish. Porter’s Five Forces illustrate what may cause a market to have good margins, and what might drive it to a price war. In the current smartphone, console and PC markets, what’s happening is that a lot of the reasons for hyper competitiveness apply.

Low margins are the very reason OEM companies like Compaq and Gateway appeared to be hugely successful, then collapsed seemingly out of nowhere.

Re: Microsoft and Google trying to enter the high end.

1. Google is weird. Because the founders own 50% of the company, it can do exactly as it pleases and ignore the temper tantrums of greedy shareholders. Now some of what Google pleases is very cold blooded and calculated, and some of it looks more like a bunch of nerds decided that it would be fun to do something without really caring whether it makes money or not. Most of their hardware projects seem, from the outside, to come more from the “wouldn’t this be fun” department rather than the “how does this help our strategic position” department.

The problem is, vanity projects don’t sell well. Google’s early hardware was priced and sold at or nearly at cost, and they made no bones about that fact. They were engaging in a price war. And their incredibly inexpensive hardware sold OK. but not in mass quantities, not in “taking over the world” quantities that would justify continuing the price war. Now that they know they have an ardent base of Android fans that will buy their hardware, but that outside of that group, nobody cares, they no longer have any reason to continue their price war pricing, so they’ve adjusted the prices upmarket.

2. Microsoft’s surface program has, from the beginning, looked like they set out to out-Apple Apple. The obsession with how the kickstand sounds when you shut it, the product launch videos that talk about the metal of the chassis, the awkward scripting of the event at which they announced Surface to the world, and the entry level price of the non-pro surface. it was all very clearly an attempt to do like Apple does… but without any knowledge of why/how these rituals work for Apple. In short, one could argue that Microsoft’s premium pricing on their Surface line is part of a cargo cult. They see Apple do certain things and rake in impressive margins on massive sales. They do the same, or try to, including setting their margins high, and then wonder where the massive sales went.

To be fair, after an initial year of flailing, in which MS had to write off the money they spent making millions of $500 surfaces that nobody wanted,.MS has been able to sell a reasonable number of Surface Pros, enough that unlike the ARM surface, the pro surface has not been ignominiously cancelled. But I’m still not quite sure if they have any idea of *why* they are in the market at a premium price point, other than “it’s what Apple does.”

It’s not just the Surface price point that is premium, the devices themselves are too. Everyone keeps harping about the OEM race to the bottom, so it’s not hard to understand why MS chose to buck that race instead of adding their drop to an already well-filled bucket ? Also, they did start with entry-level tablets too, which nobody wanted. And it seems to be working for them. And they have OEMs to cover to low and mid range anyway, so they don’t need to go there when the MS imprimatur also works at the high end.

As for “ardent base of Android fans”… that’s iFan speak for “committed, satisfied customers” I guess ? Indeed, there are a lot of those.

“As for “ardent base of Android fans”… that’s iFan speak for “committed, satisfied customers” I guess ? Indeed, there are a lot of those.”

I don’t know if it’s the same or not. You always like to maintain some kind of political correctness and optimistically assume that what is good for the goose is good for the gander, so to speak.

But, the fact is, it may or may not be the same in every respect on both sides of the fence. Sure, an ardent base of Android fans can profess to be committed, satisfied customers. But here’s me just thinking that is a bit too intangible a statement to swallow without closer examination. You got some details, or, better yet, some proof? ;P

I mean, for the “iFan’s” part, there are all kinds of things that make him committed and satisfied, such as: no worries about carriers, their agenda, who made the phone, or who sold him the phone, etc. — he just walks up to a genius bar and gets help, maybe a new phone; he gets an update the moment every other iPhone user on the planet gets one; he finds that his phone can actually work better for him two years after he bought it than the day he bought it; he finds that he can sell it after two or three years for more than most Android phones are worth new; he doesn’t worry about malware or viruses; he doesn’t worry about his personal data; etc.

Frankly, “it does the same things for a lot less money” seems to me like the only reason one would ever need to choose one gizmo over another.

But since you want to pretend I’ve never laid them out, a few specific reasons:

– choice of hardware. Small, large, Xlarge. 7-day battery. Rugged, swappable backs. There’s not 1 (sorry, 2) devices supposed to fit all.

– choice of software. We can substitute any app including system ones with any other: get a keyboard that takes handwriting, a home page that changes depending on hour/location, get rid of Google’s services and put HERE maps, Firefox, dropbox, Office… as default instead

– choice of supplier: when renewal time comes, you can switch OEM and move everything you learned and bought over to your new device.

– choice of wearables/peripherals. We’ve got more choice than getting either an iWatch or an iWatch.

– widgets. double-tap screen, see in one glance all recent messages and alerts instead of a sea of icons with little red toasts.

– innovative features. Want to know what iOS is getting next ? Look at what Android is doing today: tap to wake, wireless charging, widgets, multitasking/windowing, NFC/Pay… 3rd-party apps do the same on the software side (innovative launchers, ad blocking browsers, IFTT…)

You original post listed a few advantages on the iPhone side:

– no worries about carriers. ?? Get an unlocked phone ?

– who made the phone: the same, chinese quasi-slaves ?

– who sold him the phone. ??? the one he bought it from ?

– updates: well, 30% of iPhones users aren’t getting them either, which hurts them a lot more than with Android layered (OS/PlayServices/PlayStore) and modular approach

– works better 2 years after. Mmmm Ars Technica itself told older iPhone users not to upgrade….

– can resell for more than Androids worth new: indeed. And he still loses more money than with an Android. And that’s assuming he isn’t one of the 17% of people with a broken screen, because *that* resale value is essentially 0

– doesn’t worry about malware and viruses, personal data… well, he should http://www.macrumors.com/2015/09/20/xcodeghost-chinese-malware-faq/ Distributed by your “trusty” Apple AppStore.

But don’t take *my* word for it: (from https://www.theacsi.org/customer-satisfaction-benchmarks/benchmarks-by-brand/benchmarks-for-smartphones )

I think you need to realise we are talking about:

Reasons a single user should choose a single device.

Not: Reasons a plethora of Android devices from all OEMs might sell more in the aggregate than iPhone (which no-one disputes).

Of your list, only “choice of wearables/peripherals” seems to answer the question. Software is debatable, since not all Android titles work well on all devices, and many are redundant, malware, etc.

If a person decides on a basic screen size as his first consideration, and the iPhone or iPhone+ more or less fits the bill, the fact that there are 100 other incremental sizes available in Android Land is neither here nor there. He still has to choose one device.

Most of your arguments try to accrue all the possible features of Android devices into the one choice that the consumer ends up making. So, really, your arguments also apply to Android Land (all Android devices “do the same thing”, regardless of model, high-end or low-end, or configuration); there is no reason to buy a Galaxy 6 (which relatively few people are buying) over a basic Android device costing a quarter of the price; and one could also say the iPhone “does what all Android devices do”.

The reason that 50M iPhones get sold each quarter, more than any other single model of smartphone in the world, is because, like it or not, Apple actually gets most stuff right and makes something that more people want than any other single phone available to them or affordable by them.

What answer do you want ? “Oh, shiny !!” ? “User experience !” ? Your “Apple gets most stuff right” isn’t very insightful either. Is that also why people buy so many Vuitton handbags and Nike shoes, or is there possibly more than functionality at play ?

Mostly it’s “does the job for the lowest price”. People around me mostly don’t want to spend more than $250-ish on a

phone (this is France, unlimited calls/texts + 40GB data is $20/mo,

unsubsidized, so phone price is very visible and under pressure,

consumer credit is not routine – our “credit cards” are your “debit

cards” and actual credit is strictly supervised…). Most of them could

spend more, they just don’t feel the need to.

Some want large, some want small, some want a browser with Night Mode, most love widgets once I show them how to use them, those who’ve had double tap and wireless charging miss it if they lose it…

The few around me who don’t buy on price buy for the camera or the cachet or operator subsidies. Frankly, 90% of them on both the iOS and Android side under-utilize their phones so much it’s funny. My iSister-in-Law got an iPhone 6 because her iP4 broke. I’ve never seen her do anything but whatsapp and GPS on it, and she was happy with her 4 so a $100 Moto E would have been sufficient, but… Apple !

You love to bring Vuitton up. “Many” people buy Vuitton handbags… but not more than any single other “premium handbag” range that costs from, say, half the price up to a similar price. And not more than iPhones.

I think Horace Dediu was saying that selling 50M of pretty much anything (other than commodities and consumables) per quarter doesn’t really sink in it’s so enormous, and it is quite an achievement — particularly 600-dollar somethings. So, Vuitton’s a non-comparison. iPhone is the single largest-selling “smartphone” model. I am saying there are good reasons for that, all of which, whatever they are for different users, you promptly reduce into one epithet of “shiny”.

What answer do I want? How about something like:

1) Android users love the simplicity of universal and instant updates with one simple click from settings control panel the moment an update is available, no matter where or how they bought their phone.

2) Android users overwhelmingly love the state of malware on the different Android app stores.

3) Android users are completely happy, when they think about it, with the state of security on Android.

4) Android users are completely comfortable with the privacy of their personal data as provided by Google, and with how Google might share their personal data with others for different reasons.

5) Android users love how OEMs/Phone Providers may or may not fully adhere to Google guidelines, and their software customisations may or may not be consistent, and may or may not be complementary but in reality may in fact conflict somewhat with the best intentioned potential UX that Google and ardent fans would like to think is representative of the experience of virtually all Android users.

You could say those kind of quite specific, quite concrete things — and I promise I won’t come back and ask for loads of specific data points.

You seem to have missed that the Vuitton example is to illustrate that people spend mony to show off and associate with certain values. Are you saying phones don’t follow that mechanism ?

Let me guess, you think users care A LOT about updates and security because all your points are about that. As a matter of fact, there have been fewer actual security breaches on Android than on iOS, so… your point isn’t working the way you think. Also, users who care *can* get a Nexus, so your point is moot: users love other things about Android. Also, you’re confusing iOS and Android, the 30% of iOS users who no longer get iOS updates miss out on a lot more stuff than non-updating Android users. See the very old chart below to understand why that tired canard shows you just don’t get how Andorid works.

So the last point about being forced into an OEM’s Android variant. Which is untrue because

– as I said, users can actually put whatever UI and extra features they like on their Androids. Which you dismissed as “not answering the question”, only to serve it back just now. Color me confused.

– it’s not being forced, it’s a choice. If you can’t handle having a choice, get Nexuses. You have a choice of 2, just like for iOS. Yeah ! You’ll also get updates…

So you parody mostly proves you don’t get Android. If anyone had any doubts.

So again, Android does the job for cheap, lets you choose which hardware/OS/utilitools/features/apps you prefer (I’m sure we have gold casings now too). I know: how can anyone want that ? Choice is not a feature !

Oh, I almost forgot: Android’s user experience is vastly superior, user satisfaction is hgher than for iOS devices several times more expensive. Consumers buy becasue they xwant to be satisfied.

You prefer to do the same job for a lot more money and have no choice about anything. To each is own.

“- as I said, users can actually put whatever UI and extra features they like on their Androids. Which you dismissed as “not answering the question”, only to serve it back just now. Color me confused.”

I didn’t dismiss it, I said, “Software is debatable, since not all Android titles work well on all devices, and many are redundant, malware, etc”. That goes for UI’s too. I am sure you can change UI if you want, though I assume Samsung’s specially developed features and UI aren’t necessarily available to non-Samsung phones. If you can use Samsung developed features on any Android phone, then no wonder Samsung is losing sales.

My argument, that you seem confused about, is that you can’t argue that consumers choose an Android (over an iPhone) because Samsung makes this great software (but it happens to only be available for Samsung phones).

If a user is hung up on Samsung’s special features or UI, then he is going to choose a Samsung phone, thereby dismissing all other Android phones out of hand, just as much as he is dismissing an iPhone form consideration.

And color me confused: You go on about “shiny”, and image, and how many iPhone users only do Facebook, WhatsApp, etc. But then you want to make “customisation” a selling point of Android?!?

The “customised experience”, to me, is a set of good, useful apps! The App is the UI. The phone is a tool! I don’t want to customise the experience of staring at my home screen. I stare at a screen enough. I want a good app and an OS that doesn’t get in the way or need babysitting. The iPhone (and Mac) is a good, solid tool for getting things done, whatever that may be, without getting in the way or needing babysitting.

“since not all Android titles work well on all devices, and many are redundant, malware, etc””

?? My, do you think you know stuff about an OS you’ve never actually used. I haven’t had any issue ever with Launchers on any device. There’s “malware” on 0.15% of PlayStore only Android devices (and fewer actual breaches on Android than on iOS).

You’re irrational, at that point.

Samsung have developped some nice apps/tools. But most nice apps/tools come from independent 3rd parties and can be installed on any phone. You want resons to choose a GS6+Edge ? Curved screen, sooo cooool. Metal body, so classy ! Multitasking, so efficient. Performance, so fast. Camera, the best bar none. Wireless charging, so evident.

The “customised experience”, to me, is a set of good, useful apps!

I know that customization to iOS users is choosing apps. To Android userss it is also choosing widgets, homescreen/launcher, SMS/phone/contact/calendar/map and all default apps… you should try it someday, it’s a huge improvement.

Android si a “*better, more* solid tool for getting things done without getting in the way”. And if you want to tweak things to make them better for you, you can, but you don’t have too. I know, confusing right ? Icons or widgets on a home screen ? Overwhelming !

I don’t care if someone pulls an iPhone. I care if they start harping about “user experience” and “iOS is superior” and whatnot, because both are mostly false.

“I don’t care if someone pulls an iPhone. I care if they start harping about “user experience” and “iOS is superior” and whatnot, because both are mostly false.”

Yeah, Yeah. I don’t know anyone that “harps” about user experience (myself included), unless they are specifically being asked (such as in this forum), to explain why they think the iPhone is so successful. It doesn’t even come up when asked what they like about the iPhone.

But, as to being false: one-way switching and customer satisfaction seem to tell a different story.

Mmmmm, customer satisfation is higher on Android, including with models that cost a fraction of Apple’s devices.

Brilliant. I’d completely forgotten about cargo cults.

I’ve just read the wikipedia page and I’m still not quite clear what those are… I’m not good at getting cults. I’m with the Church of Our Lady of Perpetual Exemption anyway…