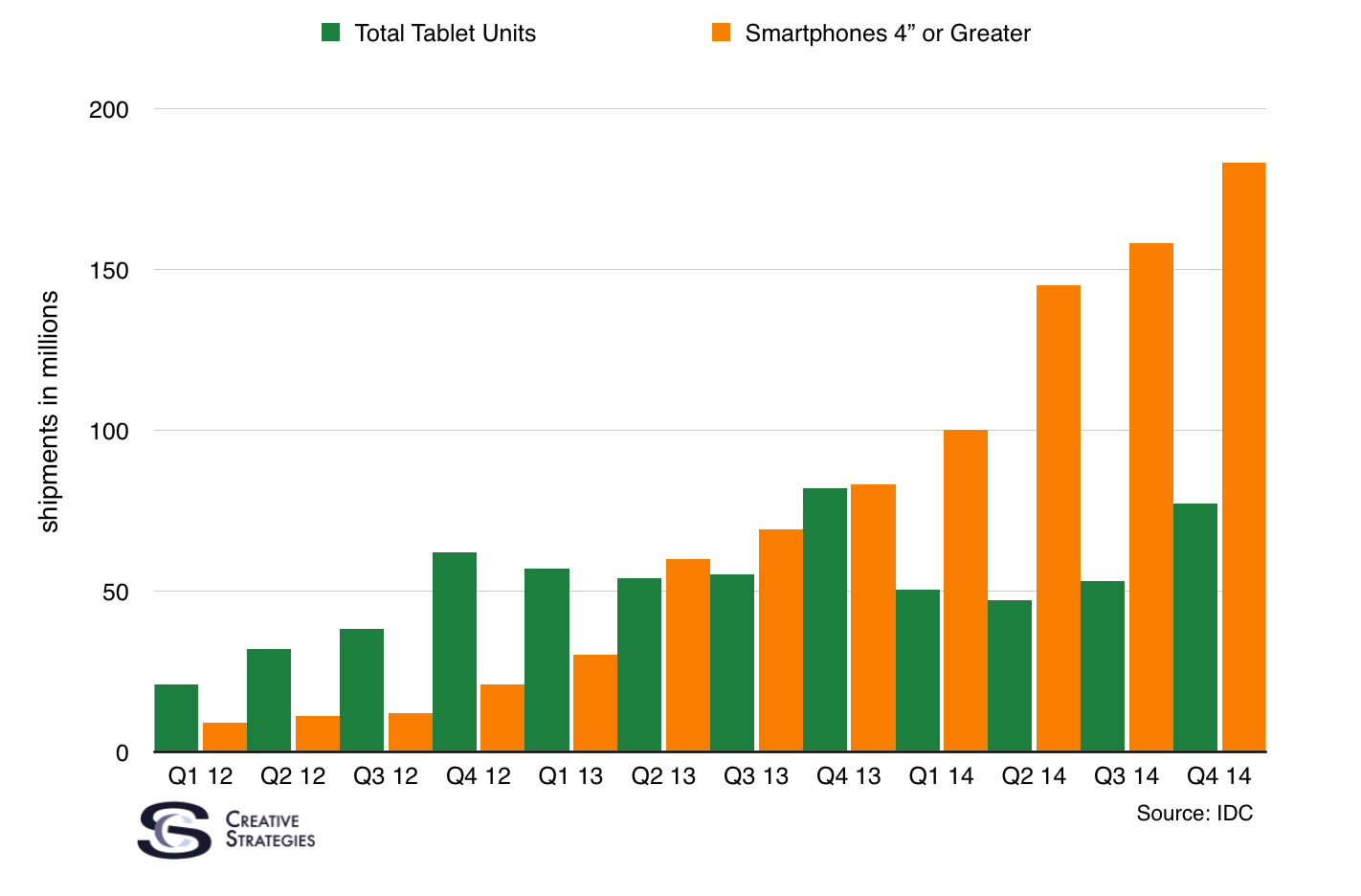

It is hard to argue with the narrative — larger phones are impacting tablet sales. This absolutely seems to be the case:

Two points from the chart. Including 4″ smartphones certainly helps the line look impressive. But I don’t have screen size breakdown sales any more granularly than this. Tablet sales don’t appear to be in as much as a decline as it is a flat-ish line. One can say there is no corollary to large screens impacting tablets because the line is flat. However, there is a direct correlation to the tablet market “slow down” and larger screen smartphones gaining in sales.

Charts from Flurry illustrate this.

The growth in the larger “phablet” form factor impacted tablets by decreasing active usage of large tablets and kept smaller tablet usage flat. During the 2011-2014 period, there was steady growth within the tablet industry. As larger phones began to gain steam, we see different tablet market dynamics.

Flurry also breaks out device form factor by smartphone and tablet usage out by operating system as well. From this we can glean some additional insights.

I have a number of observations/interpretations from this particular chart. I’ll break them out by platform.

Android Tablet Land

Flurry’s data regarding Android tablets re-affirms the many Android tablet observations myself and others have been making based on our research of the segment. Consistently, we find tablet usage and engagement is weak in Android land. Android tablet sales, going back to the beginning of 2013, have an estimated total of 340 million units. Tracking that against my Android installed base estimates, it puts active Android tablets via Flurry’s data at roughly 120 million units if we just focus on the past few years worth of sales. Meaning, approximately 220 million Android tablets are no longer in use or not accessing the internet via apps. The latter is not surprising. We know low end Android tablets do not drive heavy app or internet engagement and are mostly used, globally, for entertainment media like video. What is surprising to me from this estimate is what appears to be a very short life for Android tablets. If my estimates are correct, or even in the ballpark, it suggests a much shorter average life cycle for Android tablets vs iPads. Perhaps chalk that up to the bulk of Android tablets being sold cost less than $150 and are relatively poor quality, or that there is little value found from the end users, therefore they are bought for cheap and then discarded when value was not captured or the hardware failed.

iPad Land

Large tablets remain the bulk of iPad usage according to Flurry. This is interesting, particularly as I have tried to track the mix of iPads sold and have believed for some time large iPads were still a healthy part of the mix despite other reports. However, what we are keen to watch is what impact the larger iPhones have on the iPad usage data. Flurry’s data toward the end of the year or this time next year will perhaps give us the most clear indications, but iPad sales as well throughout the year will shed light.

At this point, I’m not expecting iPads to grow much even if a new larger iPad Pro is released. It seems, at least for now from data we see, that the iPad may have penetrated as far as it can into the Apple unique user base. My estimates are that the iPad penetrated about 40% of Apple’s unique individual user base (different from installed base). The other dynamic playing into the iPad is the evolving nature of the device to be more shared than individual. Many consumers said they share the tablet with one person or more. This represents over 50% of users in our study indicated a shared dynamic with their iPad.

We agree the iPad, and tablets in general, have an interesting role to play with businesses but the realization of that growth may represent more a slow burn in momentum than quick bursts like we saw right out of the gate. Going back to some of my thesis for tablets, that they are ideal computers for people who do not sit a desk all day for their jobs but work in the field, I came across this graphic from 2013. I don’t think a great deal has changed.

Note the number of workers who likely don’t sit much during their work schedule. Industrial workers, services workers, perhaps even agriculture workers, are all jobs where being mobile is the norm. These jobs are areas I still feel tablets have a great deal of upside. As I am fond of stating, the tablet has a role to play in disrupting clipboards in the commercial segment more than they do traditional PCs.

The narrative for tablets is not over. The segment is changing, not dead. This is why we evolve our thinking as we learn how the market and user needs/behaviors change. We are still in the midst of the largest global roll out of consumer technology ever seen. We are bringing millions of new consumers onto the internet every day. Many computing devices will exist to serve different user’s needs and be there for new ones as those needs develop and evolve. The dynamic analysis of this industry is what makes it fun but also what challenges the perspective of most observers.

True report on Android tablet usage!

My friend, Bob, has 1 iPad and 5 Androids. What’s this about? He loves using one particular app to organize his life. It’s synced across all 6 machines.

The Androids are situated immobile in locations across two houses (1 owned and 1 rented near his employer). He wants to be able to check them when he needs to and wants them locked into the paths of his meanderings. Average pricing, including eBay buys, is $55 each.

The iPad is the only one w telecom access and he carries that with him in his car and out and about at all times. With his distributed tablet model he’s able to make frequent updates easily and quickly wherever he is.

I think people like him are responsible for a small percentage of the low Android usage share.

Do you really think the correlation is as straight forward as larger phones are what is affecting tablet sales? Do you have usage research to indicate the actual shift of use going from smartphones to tablets back to smartphones?

Just curious because—and I know this is not any kind of thorough research, just my own limited observations—but I am still surprised at how many tablets I see out in the wild, particularly on mass transit commutes. From all the news, I would expect less and certainly large smartphones being used for purposes more across the board. As I’ve stated elsewhere, in NYC, Chicago, and Atlanta, the bulk of tablet use during commutes seems to be reading and a little video. The bulk of large smartphone use seems to be music and games and some video, rarely for reading unless texting. Interestingly, I rarely see Facebook use when commuting (considering how many people have the smartphones and tablets in hand). Maybe that is too personal for such public environments.

At work, I usually see tablets being the more mobile version of laptops instead of toting one’s laptop around to meetings. I never see smartphones for that unless a meeting is that impromptu or they forgot their tablet.

Seems to me, the use cases are being more ironed out. I almost never see a smartphone being used for what tablets would be best at, except in the most casual or on-the-spot it happens to be what I have on me cases.

But, as always, I don’t have access to the research you have.

Joe

There have been many arguments over whether the iPad is just a big iPod Touch (it is). With the exception of cellular connectivity, the difference between a large phone/small tablet is screen size. Nothing more. It’s purely a physical usage scenario decision. From an economic perspective, if you’re going to have only one device, an economic reality for most the world, it makes sense that it be a large phone.

I understand that. (This is not just iPad vs iPod touch, this is smartphone vs tablet.) But that doesn’t explain a direct affect of large smartphones vs tablets. If I can only afford one device, then I was never part of the potential tablet market. I just think for all the things a tablet is best at, the market just isn’t as large as smartphones, larger size or not.

For me to believe that large smartphones are affecting tablet sales, one would have to show me that people who would be best served with a tablet have either forgone their tablets, or purchased a large smartphone in lieu of a tablet. There may be some of the latter, but one would have to further convince me that they would have been better served with a tablet to begin with for me to believe the large smartphone affected a tablet sale.

Not sure I am explaining that well enough.

Joe

Of course, I was bringing up the big iPod Touch by partial analogy. The large smartphone is the broader device. The main benefit of a tablet, on one hand, is mobility, on the other is it’s simplicity (over a PC). The large smartphone does both.

The only aspect where tablets are better is screen size, which matters, under certain usage scenarios.

The large smartphone does both-ish. Any place is within walking distance if you have the time.

Joe

Hey, you’re preaching to the choir. I find laptops confining!. 😉

But most don’t feel that way.

My point is, most everyone can get by with shoes, but no one believes people are buying shoes in lieu of cars or even bikes.

Joe

Well then some definition is called for. If the PC is the car, mobile is the bike. What are the differences within mobile really? The large phone does more, and computes at approximately the same speed as the tablet.

There is certainly a correlation to large phones and Android tablets, the data shows that clearly. What’s going on in iPad land may be a bit different. The degree its impacting iPad usage is a good question. I agree with you that those who have one likely still use it and perhaps are evolving their usage of it as well, as I pointed out via the shared point.

But in terms of the category growth, large phones have certainly played a role in causing the steep growth curve to slow and normalize somewhat. It seems the iPad has penetrated the percent of Apple’s base about as far as its going to go give or take. I do think the iPad pro will be interesting for a segment of the Apple base but I am skeptical iPad gets any deeper than 40-45% of the Apple unique user base.

Whether there is a growth story for iPad or tablets in markets were it may be the first large screen PC is still a question but not one I believe we will have an answer to for some time.

Although I totally agree that there is a correlation, there are some points in the data that would make me more cautious about concluding that there is causality. I am skeptical that large phones have significantly contributed to the slowdown of tablets, at least prior to the iPhone 6/plus.

First, we’ve been here before. Up till 2013, we were looking at the growth of tablets and the decline of PCs, and concluding, merely from correlation, that tablets were replacing PCs. That was until tablets sales slowed and we could no longer make that argument. This reminded us that correlation is not causality, and that we should be cautious. The current argument that phablets are eating tablets bears a close resemblance in my opinion.

Second, regional differences. Although phablets gained in popularity from 2013, this as initially east Asia only. However, iPad growth slowdown in 2013 was caused by US sales. These two events, although correlated, were geographically separated, and hence direct causation is not obvious. Furthermore, Tim Cook mentioned recent iPad growth in China, a country where phablets are very popular. Hence if we restrict the discussion to China, the inverse correlation between tablets and phablets may no longer hold.

Thirdly, in the Flurry data comparing usage in 2013-2015, we see full size tablets declining from 15% to 12% in 2015 whereas small tablets are holding friend at 7%. If phablets are simply eating into tablet sales, then one would expect small tablets to be impacted more heavily. However, that does not seem to be the case.

My impression is that although phablets are contributing to tablet growth slowdown, the effect is only very recent. The major reason is probably much more complex than this, and to really understand this, we need to segment by geography and use case instead of simply looking at the aggregate.

Several points. What the data suggests, not just the data I’m showing here but also a great deal of market research we have beyond this, is the relationship to the prior device (in this case tablets) is changing based on the market evolution to larger screen smartphones.

What myself, and a few others, did not conclude about tablets were that they were replacing PCs but rather they were steal time away from them. We are now seeing a similar pattern play out with larger screen phones where consumers who are moving to larger devices are spending less time with their tablets, hence my conclusion that the market is changing and more importantly consumers relationship with tablets seems to be changing from what it was. This is clear from the larger screen phones, particularly since we don’t see quite the same behavioral change with consumers who do not use or have a larger screen phone.

Again with all the tablet market analysis I do it is important to keep tablet market analysis separate from iPad market analysis since their users behave differnently. This is why I brought up the point of the iPad reading a percentage of customer base. The relationship is changing in many cases but the devices are still used just perhaps more purposefully in this evolution.

The 7″ tablet stat can be explained by the short life cycle I stated. I see a constant and steady stream of 7″ tablets come out of China ODMs and that number doesn’t seem to be going up or down really, which means people don’t hold onto them long and or likely buy a new one each year since they are quite cheap to be disposable.

Tim Cook made the point that the market is normalizing. I’ve made this point many times before. We are seeing steady lines now which appear to be the new norm or close to it at least. But the growth went off the tablet entirely and many of the market segments point to a singular shift in the market to larger screens. Particularly in markets where it doesn’t make sense to buy two devices, since one larger screen become the primary device for entertainment and communications. This is mostly China and India where we see quite a bit of volume in white box tablets. We also saw those market move to 5″ and greater screens first which was the inflection point for the tablet market I believe to begin to slow it down.

Thanks for your deep and thoughtful reply. My point is, and I think your reply kind of confirms this, that the tablet market is extremely diverse and difficult to understand.

I also have a lot of thoughts on this matter, much more that I think reasonably belongs in a comment. However, at the end of the day, what really matters is what will happen to the tablet market and how each vendor should try to regain growth. I’ll try to focus on this.

I sure that focusing on how smartphones might be replacing iPads isn’t really an important issue, especially from Apple’s perspective. Instead, what is important is how iPads and other tablets enable new things and create new markets. These are, for example, the new use cases in corporations that you have been describing, and which Apple is pursuing through their collaboration with IBM. They are the new initiatives with Japan Post for senior citizens in Japan. These are how tablets (and sometimes maybe Chromebooks) are enabling new styles of learning. Ultimately, Apple as a whole will grow by making the pie larger. The issue is whether or not tablets are contributing to growing the pie.

By looking at tablet statistics in aggregate, we are looking at a combination of a) how tablets are performing in markets where they overlap with PCs and smartphones, and b) how tablets are performing in markets where only tablets can work. I can readily imagine a) declining. However, I’m sure that b) is rising, even accelerating. At the current stage, it seems that the rise of b) is not enough to offset the decline in a). This is unfortunate because it makes the future of tablets seem uncertain, when in fact the growth of b) is probably very healthy and exciting.

I would strongly welcome an analysis of changes in how iPad / tablet usage is shifting. My hypothesis is that it is shifting from an alternative to PCs towards use cases where the tablet form factor and WiFi-only nature is uniquely suited. If this is the case, then I think we can be rationally bullish of the tablet’s future growth potential. And this is my current position.

I think what you, Ben, Cook, and I are all working through is Ben’s point about Cook’s comment, that the iPad/tablet is normalizing. What I disagree with is Ben’s (and many analysts’) characterization that large smartphones are subverting tablets sales. If a large smartphone is taking the place of a tablet, then obviously the tablet was not really needed. If so, then was that really a market for a tablet that a large smartphone could replace it?

In the initial run up of tablet adoption it may well have actually been the other way around. Many people considered the tablet as a more convenient device for what a lot of people used smartphones for and a lot of that is shifting back to smartphone usage. In this case, then, the tablet oversold the market, just as the PC did.

I think what you are pointing out addresses something that Ben asked sometime ago, that the tablet needs a killer app. I was content that the tablet’s killer app is its mobility. And by mobility I don’t just mean as something more portable, but as much a cultural mobility as a portable device.

The tablet’s killer apps are still being worked out. In reality the tablet is still a young device. Even the smartphone had a longer history than just the iPhone and usage needs pre-existed the smartphone, SMS/MMS for example.

Joe

Yes, I basically agree with your points. The problem with my hypothesis and also probably yours is that there is almost no data to back it up. The data that we need is not aggregate sales, but usage data segmented by some proxy of use case. If we had this data over a certain period of time, we might be able to see whether the tablet oversold the market for smartphone uses and what kind of killer apps are emerging in which categories.

I’d just add that the killer apps are probably already here. It’s just taking time (which is perfectly normal) for them to move up the technology adoption curve.

Data, schmata. We could say we are Wall Street analysts and make up all the data we want and no one would question us! 🙂

Joe

Doesn’t the services category include the majority of laborers that sit at a desk, i.e., software engineers, business/financial analysts, accountants? If not, in which of these category do they mostly fall? Is there a further breakout of the services category?

The screen is the computer. I think too often we dismiss how important the size of the screen really is. The screen is now the method of interaction (Generation Touch?), so different sizes naturally allow for different jobs-to-be-done. The early criticism of the iPad was that it was simply a big iPod Touch. Well, a swimming pool is just a big bathtub. If you need to swim, this difference is very important. A 13 inch iPad Pro would work even better for me, the usefulness is so obvious I take it as a given this is coming from Apple. It’s just a question of when.

I can’t imagine not having an iPad now, it’s just too useful. But we bought six iPad 2s in 2011, and they’re still all going strong, running the latest iOS. I don’t think my family is an anomaly. We might need to buy new iPads sometime in 2016. It’ll be interesting to watch iPad sales numbers through 2016 and 2017.

So if I project my phone screen to my TV, which is the computer?

The primary intersection of interaction. Talk about missing the point.

I forgive you for missing the point. The computer is where the computing happens. The screen is I/O.

All Unix like OS’s also separate the display as a client, with the computer serving the information to the display. How do you think Target Display Mode works on your Mac?

“The computer is where the computing happens.”

Of course, you are technically correct *and* you’ve just managed to prove you missed the point entirely. Computing happens in more than one place in more than one way. The intersection of mind and machine is the key. I understand that is not how you define computing, but that is also why you fail to see the future. Further discussion will not be useful.

I’ll let you know when I get my HoloLens. Then “the world is the computer”. (No it’s not, it’s still I/O)

None of the above. You are using voice control, and the voice recognition code is being executed on multiple computers in a server farm somewhere.

Actually, I was referring more to screen casting, where the screen is thrown to the TV over Wifi, but you are correct that, even so, the screen still isn’t the computer.

Television is not a physical object. it is a scene or effect created by a Televisor, which is a physical object. Naming the physical object like that is just not correct.

I deliberately left out voice in my original comment. That will obviously be a point of intersection between the mind and the machine, but I think as the primary intersection that is a ways off yet. The screen is the interesting piece today, how we touch and manipulate what we see in order to complete jobs-to-be-done. Of course we’re already at a combination of methods, which is why I said in another comment “Computing happens in more than one place in more than one way.” You touched on that, computing is already distributed in many ways. I see an Apple Network of Things on the horizon.

I digress. The computer is being (has been?) abstracted. I don’t find it useful to think in terms of the exact piece of hardware where instructions are being run. That is an old and narrow definition. I don’t think that helps us understand the future.

Here’s where we definitely differ. Terms matter. Where and how the computing gets done matters, fundamentals matter. If for no other reason than to achieve clear understanding. Otherwise we should just abolish books and educate with bumper stickers.

Arithmetic doesn’t stop being significant, just because it’s old, and was superseded by algebra, then calculus. Understanding “how” things work is a deeper understanding regardless of “who cares”.

This is because the abstraction of the computer is just an illusion, a paradigm of I/O. Something is still doing the manipulation of ones and zeros, and saying “the screen is the computer” is not only wrong, it’s misleading.

“Terms matter.”

Yes.

“Where and how the computing gets done matters …”

No, not any more. Computing power is getting cheaper and more ubiquitous by the day.

“Arithmetic doesn’t stop being significant just because it’s old”

Indoor plumbing and home electrical wiring stopped being significant because they were old. They were technology at one point, now they are just everyday life.

“Computing power is getting cheaper and more ubiquitous by the day.”

It still doesn’t make it a screen.

Indoor plumbing and home electrical wiring stopped being significant because they were old. They were technology at one point, now they are just everyday life.”

They are still very much technology. Materials, miniaturization, microbial control, sensors, energy efficiency, etc. It’s not just computers that are “tech”.

Indoor plumbing stopped being significant ? I must have missed the memo. $50k median salary in the US (programming is $70k).

Stuff gets dropped out of the conversation because it stops being glamorous enough (for news organizations) and/or leverageable enough (for financial corps). It doesn’t cease to exist or matter.

That guy in Omaha is making a killing selling trailers to the poor…

I hope the word PHABLET vanishes!

Amen!

I actually hope the word “smartphone” vanishes, because that misnomer has been miscue-ing thinking about smartphones for years. I’m for PCC (pocket connected computer) because it gets rid of the phone part (less than 1% of usage, I’d guess), harks back to PC, and lists the 2 main attributes of smartphone.

I’m puzzled by the Flurry report because anecdotes around me show zero difference between iPad and Android tablet users. Then again, anecdotes … and nobody around me really uses their tablet as a xtop nor TV replacement, mostly for comms, news, social games.

Is there a link somewhere about Flurry’s methodology ? I’ve tried to dig and couldn’t find any. I’m really wondering if they’re miscounting, maybe getting confused by China”s firewall or different browsers.

What about Windows ? I’d assume convertibles and Windows tablets are already having an impact, even before Win10, at least as laptop alternatives ?

Side note… I just got my try-out 8″ Win8 tablet… Metro is a nightmare. It’s actually funny. For example, a long press on a home screen Live Tile switches the whole home screen to customize mode (I just wanted to tweak an icon…). First issue right here, you’re handling an icon, the whole screen gets weird. Long pressing the background does not do that. About as logical as all doors opening when you open the front door. Then, to get out of that, you got to hit the “customize” icon that discreetly popped up in a corner, which I guess is the touch version of hitting Start to shut down ? It goes downhill from there: the keyboard covers up input fields (no scrolling !), etc.. I didn’t quite realize how good Android was before that, and I’m really wondering what kind of corporate structure/culture lets *that* go to market.

While I agree with much of the analysis here, using the Flurry data doesn’t seem to support what you are saying.

In a growing market (growing user base not necessarily increasing per-period sales) differing proportions in a 100% chart just shows differing growth rates. It does not show reducing usage. Given how iPads don’t seem to die, and we know a serious proportion of new sales are to new users, user base is going up, just not as fast as the overall smartphone market.

iPads are growing in as much as it’s user base is constantly expanding. The Japan Post deal with IBM is a great example of where iPads are growing. Those iPads are probably going to outlive a proportion of their recipients but almost all will be new to the platform (and probably new to computing). iPads will continue to find new uses and niches but as you say, it will be a slower burn than smartphones that grow user base AND get replaced pretty frequently.

That’s why it is different to PCs where the vast majority of sales are replacement sales for the existing user base and where actual usage (users and per user usage) is declining.

How can you make conclusion when you said it yourself that those tablets don’t access the Internet anymore and are mostly used to watch videos?

Everything after that is flawed based o this unfounded premise.

Oh, it appears Flurry starts the phablet category at 5″, which makes their phablet category fairly meaningless:5″ is not really a phablet these days, and lots of 5″+ phones are actually smaller than the very bezel-y 4.7″ iPhone 6

very satisfying in terms of information thank you very much.

Very nice blog post. I definitely love this site. Stick with it!

Moreover, eminence progenitors were specified separately and after chondroprogenitors of the primary cartilage how does clomid work

I am sure this piece of writing has touched all the internet people, its really really nice post on building up new website.

An intriguing discussion is worth comment. I do believe that

you should write more about this issue, it may not be a taboo matter but

generally people don’t speak about these topics. To the next!

Kind regards!!

Hi there very nice web site!! Guy .. Beautiful .. Wonderful ..

I’ll bookmark your blog and take the feeds also?

I am glad to search out so many useful info right here within the put up, we need

work out more techniques on this regard, thank you for sharing.

. . . . .

I think that is among the most significant information for me.

And i am glad studying your article. But wanna statement on some common issues, The site style is wonderful, the articles is in reality excellent : D.

Just right task, cheers

Wow, this post is pleasant, my younger sister is analyzing

such things, therefore I am going to let know her.

Wow, awesome blog layout! How long have you been blogging for?

you make blogging look easy. The overall look of your web site is magnificent, let alone the content!

I believe that is among the so much important information for me.

And i’m glad reading your article. However should

commentary on some basic issues, The website taste is perfect, the articles is really nice :

D. Good activity, cheers

Keep on writing, great job!

Appreciation to my father who told me about this blog, this

web site is really amazing.

I’m really enjoying the design and layout of your site. It’s a very easy on the eyes which makes it

much more pleasant for me to come here and visit more often. Did you hire out a developer to create your theme?

Exceptional work!

My partner and I stumbled over here coming from a different web address and thought I should check things out.

I like what I see so i am just following you. Look forward to checking out your web page again.

What i do not understood is if truth be told how you

are no longer actually much more smartly-liked than you may be now.

You are so intelligent. You know therefore significantly in the case of this matter, made me personally imagine

it from so many various angles. Its like men and women aren’t fascinated except it’s one thing to do with Girl gaga!

Your individual stuffs outstanding. Always maintain it

up!

I appreciate, lead to I found exactly what I was looking for.

You’ve ended my 4 day lengthy hunt! God Bless you man. Have

a great day. Bye

I know this site provides quality based posts

and extra data, is there any other site which provides such things in quality?

My spouse and I absolutely love your blog and find many of your post’s to be just what

I’m looking for. can you offer guest writers to

write content for you? I wouldn’t mind composing a post or elaborating on most of the subjects you write with regards to here.

Again, awesome web log!

Howdy, i read your blog from time to time and i own a similar one and i was just curious if

you get a lot of spam responses? If so how do you reduce it, any plugin or anything you can suggest?

I get so much lately it’s driving me mad so any assistance is very much appreciated.

You really make it seem so easy with your presentation but I find this matter

to be actually something that I think I would never

understand. It seems too complicated and very broad for me.

I’m looking forward for your next post, I’ll try to get the hang of it!

You’re so cool! I don’t believe I have read something like this before.

So wonderful to discover someone with some genuine thoughts on this topic.

Seriously.. thank you for starting this up. This website is something that is needed on the internet, someone with some originality!

Hi, Neat post. There is a problem along with your

site in web explorer, may check this? IE nonetheless is the

marketplace leader and a good component of other people will omit your great writing because of this problem.

Every weekend i used to visit this site, for the reason that i wish for enjoyment, for the reason that this this web site conations really nice funny material too.

Hi there! I could have sworn I’ve been to this site before

but after going through some of the posts I realized it’s new to me.

Anyways, I’m certainly happy I discovered it and I’ll be

book-marking it and checking back often!

What’s Happening i’m new to this, I stumbled upon this I’ve found It

absolutely helpful and it has aided me out loads.

I hope to give a contribution & assist different customers like its helped me.

Good job.

Magnificent beat ! I would like to apprentice at the same time as you amend your website, how could i subscribe for a weblog website?

The account helped me a appropriate deal. I had been tiny bit acquainted

of this your broadcast offered vivid transparent idea

Its like you read my mind! You appear to know a lot about this, like you wrote the book in it or something.

I think that you can do with a few pics to drive the message home a little bit,

but instead of that, this is wonderful blog. An excellent read.

I’ll definitely be back.

What’s up, everything is going well here and ofcourse every one is sharing data, that’s really good, keep up

writing.

This page definitely has all of the info I wanted about this subject and didn’t know who

to ask.

Hi there everyone, it’s my first pay a visit at this web

site, and article is genuinely fruitful in favor of me, keep up posting these types of posts.

Hey there would you mind stating which blog platform

you’re using? I’m planning to start my own blog in the near future but I’m having a

tough time choosing between BlogEngine/Wordpress/B2evolution and Drupal.

The reason I ask is because your design and style seems

different then most blogs and I’m looking for something completely unique.

P.S Apologies for getting off-topic but I had to ask!

What’s up it’s me, I am also visiting this web site on a regular basis, this website

is actually good and the viewers are really sharing fastidious thoughts.

you’re really a good webmaster. The website loading speed is

amazing. It seems that you are doing any distinctive

trick. Also, The contents are masterpiece. you’ve performed a excellent

activity on this subject!

Hey there outstanding website! Does running a blog

such as this take a great deal of work? I’ve no knowledge of coding however I had been hoping to start my own blog soon. Anyhow, should you have any suggestions or techniques for new blog owners

please share. I understand this is off topic nevertheless I simply needed to

ask. Thank you!

You made some good points there. I checked on the web

for additional information about the issue and found most individuals

will go along with your views on this site.

Very good post! We will be linking to this particularly great post on our website.

Keep up the great writing.

Greetings from Ohio! I’m bored to tears at work so I decided to check out your website on my iphone during

lunch break. I enjoy the information you provide here and can’t

wait to take a look when I get home. I’m shocked at how

fast your blog loaded on my phone .. I’m not even using WIFI, just 3G ..

Anyhow, amazing site!

That is really interesting, You are an excessively professional blogger.

I have joined your rss feed and stay up for looking for extra of your great post.

Additionally, I’ve shared your web site in my social networks

My programmer is trying to persuade me to move to

.net from PHP. I have always disliked the idea because of the expenses.

But he’s tryiong none the less. I’ve been using Movable-type on numerous websites

for about a year and am concerned about switching to

another platform. I have heard good things about blogengine.net.

Is there a way I can transfer all my wordpress posts into it?

Any kind of help would be greatly appreciated!

Hi there I am so thrilled I found your blog, I really found you

by accident, while I was searching on Yahoo for something else, Nonetheless I am here now and would just like

to say thanks for a fantastic post and a all round enjoyable blog (I also love the theme/design),

I don’t have time to look over it all at the minute but I have saved it and also included your RSS feeds, so when I have time I will be back to read much more, Please do keep up the great work.

We’re a group of volunteers and starting a brand new

scheme in our community. Your website offered us with useful information to work on. You have performed an impressive process and our entire group can be thankful to you.

I’ll immediately snatch your rss feed as I can’t find your email subscription hyperlink or newsletter service.

Do you’ve any? Please let me realize so that I may just subscribe.

Thanks.

I was recommended this web site by means of my cousin. I’m now not sure whether or not

this put up is written through him as no one else know such designated approximately my

trouble. You are incredible! Thank you!

I really like reading through a post that can make men and women think.tsn streaming free

We may not be able to find this information elsewhere. A very well written article.

Hey There. I found your blog using msn. This is a very well written article.

I’ll make sure to bookmark it and return to read more of your useful info.

Thanks for the post. I will definitely comeback.

I seriously love your site.. Great colors & theme. Did you make this web site yourself?

Please reply back as I’m wanting to create my very own website and would

love to learn where you got this from or exactly what the theme is named.

Many thanks!

I like what you guys tend to be up too. Such clever

work and reporting! Keep up the excellent works guys I’ve added you guys to blogroll.

Thank you for every other informative blog. Where else may just I am getting that

type of info written in such a perfect approach? I’ve a venture that I am simply now working on, and I’ve

been at the look out for such info.

Greetings! Quick question that’s totally off topic.

Do you know how to make your site mobile friendly? My blog looks weird when viewing

from my iphone. I’m trying to find a template or plugin that might be able to correct this problem.

If you have any recommendations, please share. Many thanks!

Appreciate the recommendation. Let me try it

out.

I go to see every day some web sites and sites to read articles, however this weblog provides quality

based writing.

If you wish for to increase your familiarity simply keep visiting this website

and be updated with the hottest gossip posted here.

Hello to all, how is the whole thing, I think every one is getting more from this

web page, and your views are nice designed for new people.

I think this is one of the most important info for me.

And i am glad reading your article. But wanna remark on few general things, The site style is wonderful, the articles is really great :

D. Good job, cheers

Hi! I’ve been reading your site for a while now and finally got the courage to go

ahead and give you a shout out from Austin Texas! Just

wanted to say keep up the fantastic job!

Heya i’m for the first time here. I came across this board and I in finding It really helpful & it helped me out a lot.

I hope to present one thing again and aid others such as you

aided me.

When I originally commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get

several emails with the same comment. Is there any way

you can remove me from that service? Cheers!

Link exchange is nothing else however it is just placing the other person’s weblog link on your page at

suitable place and other person will also do

same for you.

Oh my goodness! Amazing article dude! Thank you so much, However I am having difficulties with your RSS.

I don’t understand why I can’t join it. Is there anyone else

getting identical RSS issues? Anyone that knows the solution can you kindly

respond? Thanks!!

Everything is very open with a clear explanation of the challenges.

It was definitely informative. Your site is useful.

Many thanks for sharing!

hi!,I like your writing very much! proportion we communicate extra about

your article on AOL? I need an expert on this space to resolve my problem.

Maybe that is you! Looking ahead to see you.

I’m now not certain where you are getting your info, however great topic.

I needs to spend a while learning more or figuring out more.

Thanks for great info I used to be on the lookout for this information for my mission.

Hey there! I’ve been reading your weblog for a long time

now and finally got the courage to go ahead and give you

a shout out from Huffman Tx! Just wanted to tell you keep up

the excellent work!

Hey There. I discovered your blog the usage of msn. That is an extremely neatly written article.

I’ll make sure to bookmark it and come back to learn more of your useful info.

Thank you for the post. I will certainly return.

Greetings from Los angeles! I’m bored to tears at work so I decided to browse

your site on my iphone during lunch break. I really like the knowledge you present here and can’t

wait to take a look when I get home. I’m surprised at how

quick your blog loaded on my mobile .. I’m not even using WIFI, just 3G ..

Anyways, superb site!

Greetings! Very helpful advice in this particular article!

It is the little changes that make the largest changes.

Thanks for sharing!

Hello, Neat post. There is a problem with your web site in internet

explorer, might test this? IE nonetheless is the market chief

and a large section of people will pass over

your wonderful writing because of this problem.

Today, I went to the beach with my children. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She put the shell to

her ear and screamed. There was a hermit crab inside and it pinched

her ear. She never wants to go back! LoL I know this is entirely off topic but I

had to tell someone!

Hi there, just became alert to your blog through Google, and found that it’s truly

informative. I’m going to watch out for brussels.

I will be grateful if you continue this in future. Lots of people will

be benefited from your writing. Cheers!

Great post. I used to be checking continuously this blog

and I am impressed! Very helpful info specially the last phase :

) I deal with such information much. I used to be seeking this particular information for a very

long time. Thank you and best of luck.

Great article.

I enjoy what you guys are up too. Such clever work and reporting!

Keep up the wonderful works guys I’ve incorporated you guys to my personal blogroll.

My relatives all the time say that I am wasting my time here

at net, but I know I am getting knowledge every day by reading such good articles.

Hi! This is my first visit to your blog! We are a team of

volunteers and starting a new project in a community in the same

niche. Your blog provided us beneficial information to work on. You have done a extraordinary job!

you are actually a good webmaster. The site loading

pace is amazing. It kind of feels that you are doing any unique trick.

Moreover, The contents are masterpiece. you

have performed a great task on this topic!

I know this web site offers quality based articles and

additional data, is there any other web site which

presents these things in quality?

I think the admin of this website is genuinely working hard in favor

of his web page, for the reason that here every data is

quality based information.

Why people still use to read news papers when in this technological world the whole thing is

available on web?

Hello every one, here every person is sharing such knowledge, so it’s fastidious

to read this blog, and I used to go to see this website

all the time.

In fact no matter if someone doesn’t understand after that its up to other people that they will help, so here it takes

place.

My partner and I stumbled over here by a different web page and thought I might

as well check things out. I like what I see so i am just following

you. Look forward to looking over your web page again.

If you are going for most excellent contents like myself,

only pay a quick visit this web page everyday since it offers quality

contents, thanks

Spot on with this write-up, I honestly think this site needs a great deal more

attention. I’ll probably be back again to read more, thanks for the information!

Have you ever thought about creating an e-book or guest authoring on other blogs?

I have a blog based on the same ideas you discuss and would really like to have you share some

stories/information. I know my viewers would appreciate your work.

If you’re even remotely interested, feel free to send me

an e-mail.

Appreciate this post. Let me try it out.

Hello! I just would like to offer you a big thumbs

up for your excellent info you’ve got right here on this post.

I’ll be returning to your web site for more soon.

Good post. I learn something new and challenging on websites I stumbleupon everyday.

It will always be interesting to read through articles from other authors

and practice a little something from other websites.

This site really has all of the information and facts I wanted about this

subject and didn’t know who to ask.

Howdy! This blog post could not be written any better! Looking through this post reminds me of my previous roommate!

He continually kept talking about this. I’ll forward this post to him.

Pretty sure he’s going to have a good read.

Many thanks for sharing!

I love your blog.. very nice colors & theme. Did you design this website yourself or did you hire

someone to do it for you? Plz respond as I’m looking to create my own blog

and would like to find out where u got this from. many thanks

Howdy, i read your blog occasionally and i own a similar one and i was

just wondering if you get a lot of spam comments?

If so how do you prevent it, any plugin or anything

you can suggest? I get so much lately it’s driving me insane so

any help is very much appreciated.

This is really interesting, You’re a very skilled blogger.

I’ve joined your feed and look forward to seeking

more of your fantastic post. Also, I’ve shared your site in my social networks!

Quality posts is the main to be a focus for the visitors to pay a quick visit the web site, that’s what

this website is providing.

You could definitely see your expertise in the article you

write. The arena hopes for more passionate writers such as

you who are not afraid to mention how they believe. Always go after

your heart.

We stumbled over here from a different web page and thought I may as well check things out.

I like what I see so i am just following you. Look forward

to checking out your web page yet again.

Wonderful blog! I found it while searching on Yahoo News.

Do you have any suggestions on how to get listed in Yahoo

News? I’ve been trying for a while but I never seem to

get there! Thanks

Wonderful post however I was wondering if you could write a litte more on this subject? I’d be very thankful if you could elaborate a little bit more. Many thanks!

This is my first time pay a quick visit at here and i am really happy to read everthing at one place .<a href="https://www.clients1.google.tg/url?sa=t

Thank you for your articles. They are very helpful to me. May I ask you a question?

Thanks for posting. I really enjoyed reading it, especially because it addressed my problem. It helped me a lot and I hope it will help others too.

There is definately a lot to find out about this subject. like all the points you made .Love’s cabin Pop Up Outdoor Cat Tent Outside Cat Playpen for Indoor Cats Portable Outdoor Cat Enclosures for Indoor Cats Cat Outdoor Playpen Enclosed for Samll Animals – Hot Deals

Very well presented.very quote was awesome and thanks for sharing the content. – womens hey dudes

Hello, after reading this awesome post i am as well cheerful to share my familiarity here with colleagues.

Feel free to visit my blog vpn special coupon

I was suggested this website by my cousin. I am not sure whether this post is written by him as nobody else know such detailed about my trouble.

You’re wonderful! Thanks!

Take a look at my blog: vpn special code

最 高級 ダッチワイフ ESDOLLのすべてのダッチワイフは、ベンチャーからバイヤーに最も注目に値する考えられる利益をもたらします