If anything, John’s column on Android’s market share has stirred a good discussion around the market share vs. profit share debate. Some may argue that this discussion isn’t relevant to end consumers who really don’t care. To that I agree. As an industry analyst these things are of interest to how I study the industry. Data around market share and profit share help shape my perspectives relative to what companies, platforms, and technologies have the best chances of succeeding going forward. Although I agree that end consumers don’t care about market share or profit share, there is a group who does and should care–developers.

Developers Control the Future

Marc Andreesen boldly proclaimed in a 2011 essay in the Wall St. Journal that software is eating the world. He is, of course, correct and in the reality where software is eating the world, software developers control the future. Software developers are the heart of a platform. As long as a healthy software development ecosystem exists, a platforms future is not in jeopardy. Therefore, what interests me in the platform discussion, is what platforms are developers interested in and where is the most exciting software development taking place. I believe wholeheartedly the answer is iOS.

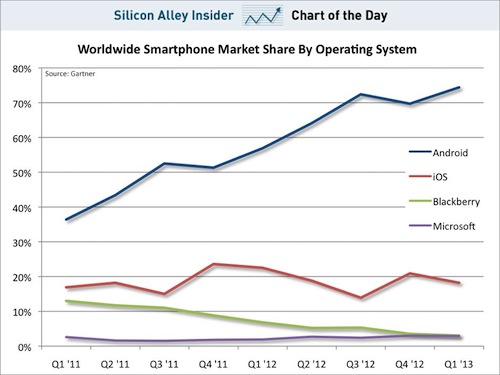

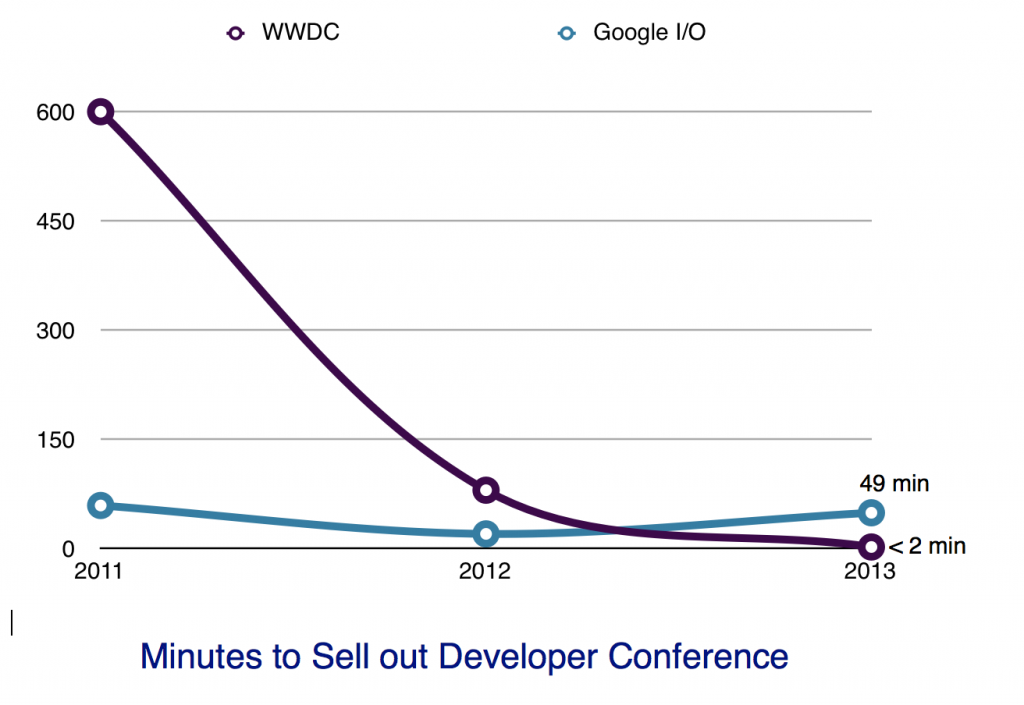

Here in Silicon Valley, where I live and work, I meet many new startups weekly. I talk with venture capitalists investing in the software revolution monthly. The major theme and trend I pick up on in these discussions is iOS first and Android eventually. Most VCs I speak with have invested in many iOS only app startups and they seem to have no problem with this from a business standpoint. Many have also invested in companies making software for iOS and Android but told me that the companies priority was iOS. From my viewpoint iOS is the hot ticket item. And it seems like developers agree. This years Apple World Wide Developer conference sold out in record time, faster than Google I/O for the first time. And it did this despite Android’s 75% smartphone market share.

Below is a chart showing how many minutes it took for each developer conference to sell out. ((I plotted since 2011 since starting that year each conference sold out in less than a day. Each year prior took days not minutes))

iOS also appears to be the best business bet for a majority of software developers. Distimo released a very interesting study this month highlighting some key metrics related to both the iOS and the Google Play Store. In a section of the report called The Apple App Store is Most Beneficial, Distimo point out:

“The daily revenue (In the US) in April 2013 generated by all applications in the top 200 grossing in Google Play was $1.1M, while the daily revenue of the top 200 in the Apple App Store (both iPhone and iPad) was 4.6 times higher at $5.1M. The vast majority of applications in those two top lists contained free applications with In-App purchases and this business model automatically generates the most revenue in both stores. The higher revenue share in the Apple App Store compared to Google Play was also characteristic for long tail applications and did not apply solely to popular applications.”

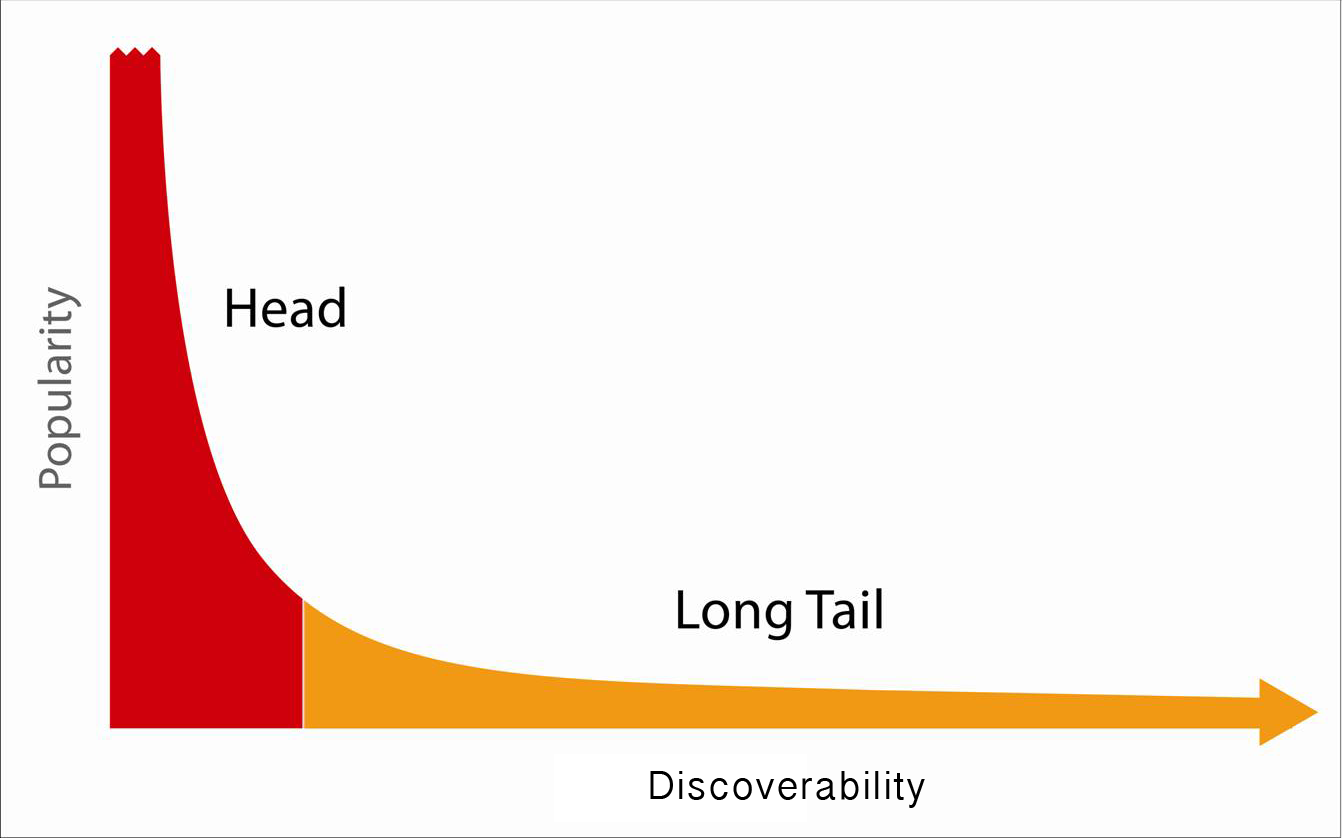

As impressive as that US centric data is, I think two clarifying points are necessary. First you will notice that Distimo specifically points out that the Apple app store revenue includes iPhone AND iPad. Why does this matter? First because there are disproportionately more iPad specific apps in the Apple App store than there are tablet specific apps in the Google Play store. In fact, I would be so bold as to say that there are so few tablet specific apps in the Google Play store that it barely showed up as a blip, if at all, in the Distimo app IQ tracking solution.

Second, this breakout which includes iPad, shows how attractive iOS is from both a smartphone standpoint and a tablet standpoint in terms of opportunities to make money for software developers. ((It is clear the iPad is a strong component to the strength of the Apple app store. Unless Google fixes this with tablet apps, the imbalance will remain))

Now, the above mentioned data was US centric, where we know the iPhone is dominant. So how about the rest of the world? Distimo makes the following observation:

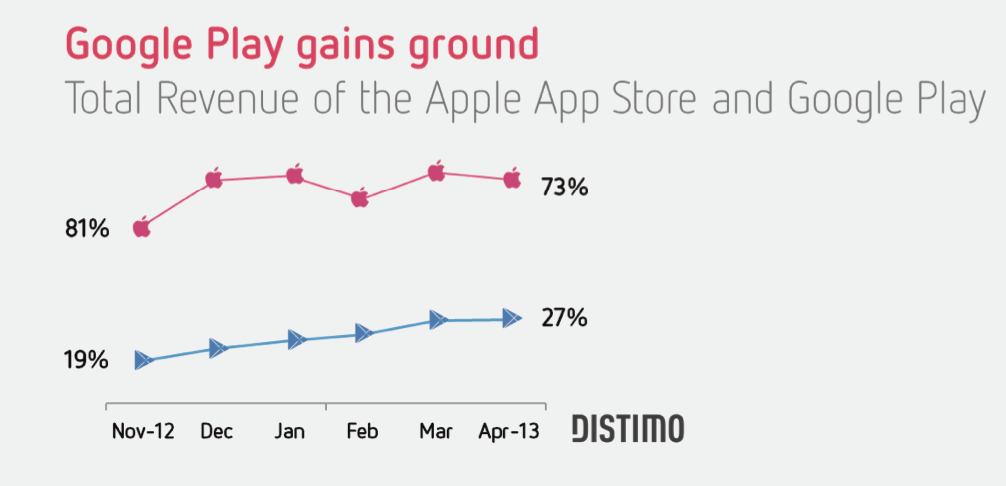

“The Apple App Store was still the larger market compared to Google Play in April 2013 in terms of total revenue. However, Google Play’s piece of the pie has increased significantly over the past six months. While only 19% of the combined revenue came from Google Play in November 2012, this share went up by eight percentage points to 27% in April 2013. The Japanese and South Korean markets were the main contributors for the growth in Google Play’s revenue share.”

Distimo makes a point that the Play Store has increased, and indeed it has. However, they also explain the answer.

“The Japanese and South Korean markets were the main contributors for the growth in Google Play’s revenue share.”

One word. Samsung. One question. Sustainable? ((I will be doing a deep dive on my thoughts on Samsung’s sustainability long term as a part of a new service we are launching soon. Sorry for the shameless plug))

Focusing on Android Software Development

Indeed, John’s column spurred quite the response from those in the church of market share. Of course Android is relevant and it’s not going anyway any time soon.

The question is can developers make money and sustain a profitable business developing for Android. Interestingly this is exactly what the Distimo report set to find out.

In the report Distimo highlights several developers and apps that have found more or at least equal success in the Google Play Store vs. the Apple App Store. The primary examples were game developer Mobage.

“In April 2013, Mobage generated more than $5.1M in Google Play in April 2013. The Apple App Store total revenue during April 2013 in the U.S. was $5.6M, which was slightly higher. This equates to a revenue share of 48% for all Mobage apps in Google Play in April 2013, while 52% of revenue came from the Apple App Store (iPhone and iPad).”

Not bad. Mobage has several popular games, Blood Brothers and Rage of Bahamut being two of the main ones. As you can see for this developer Android is a significant contributor. They are also a large publisher with games with strong brand cache.

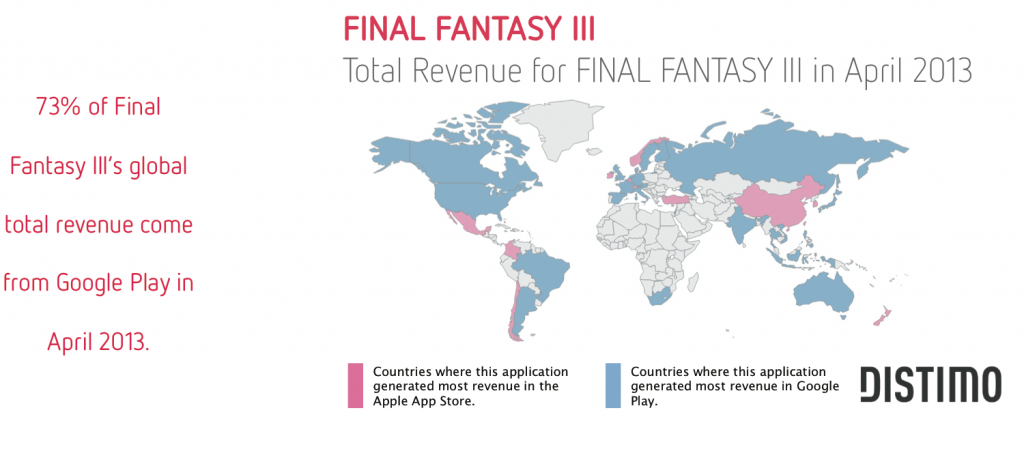

The other Android highlight was Final Fantasy III.

Again a game with serious brand affinity. As you can see Android is not a lost cause for developers. However, it does seem there is a template which is required to follow in order to make Android development worthwhile.

Conclusions

Android is a viable market place. However, as we see, it is also highly regional and more often than not success is being found by large developers with name brand apps. Therefore app developers need to be very targeted about the region and strategic about the business model that will work in that region.

The Android market is filled with successes but it also favors the larger more established app developers whose software has a strong and established brand to leverage. [pullquote]iOS presents the greatest opportunity for the entrepreneur app developer[/pullquote]

The data and the evidence constantly coming to light showcases how developers large or small are profiting from iOS development. But in my opinion, iOS presents the greatest opportunity for the entrepreneur app developer. The small to mid-size developer. The person who writes apps in their spare time and has a dream to quit their job and start their own business creating apps. This is where some of the most exciting software development is coming from. This is where the companies of tomorrow will be born.

So here is my advice to the smaller independent and garage software developers looking to build or continue to build their software development business. Follow the strategy being employed by the many silicon valley app startups. Start with iOS, build the business and the brand, then as the business grows expand. It would be foolish to ignore Android. It would also be foolish to start there. ((This is of course my opinion and you are welcome to disagree))

I have given this advice to dozens of app developers a month who seek my feedback and opinion. And I am told I am not alone in this opinion. Many remark that this advice is also given to them by their mentors, advisors, and investors (if they have them.)

It is of course true that developers can make money on Android. The Android market will continue to develop and grow. But can it attract and be a viable marketplace for the small software startups? Or for the long tail marketplace which is clearly in Apple’s App stores favor at the moment. I will agree and end with the conclusion Distimo makes in their report:

“We draw the conclusion that although the majority of applications still generate more revenue in the Apple App Store than in Google Play, there appears to be a great opportunity in Google Play in terms of revenue – and (as noted in previous publications) localization is the key.”