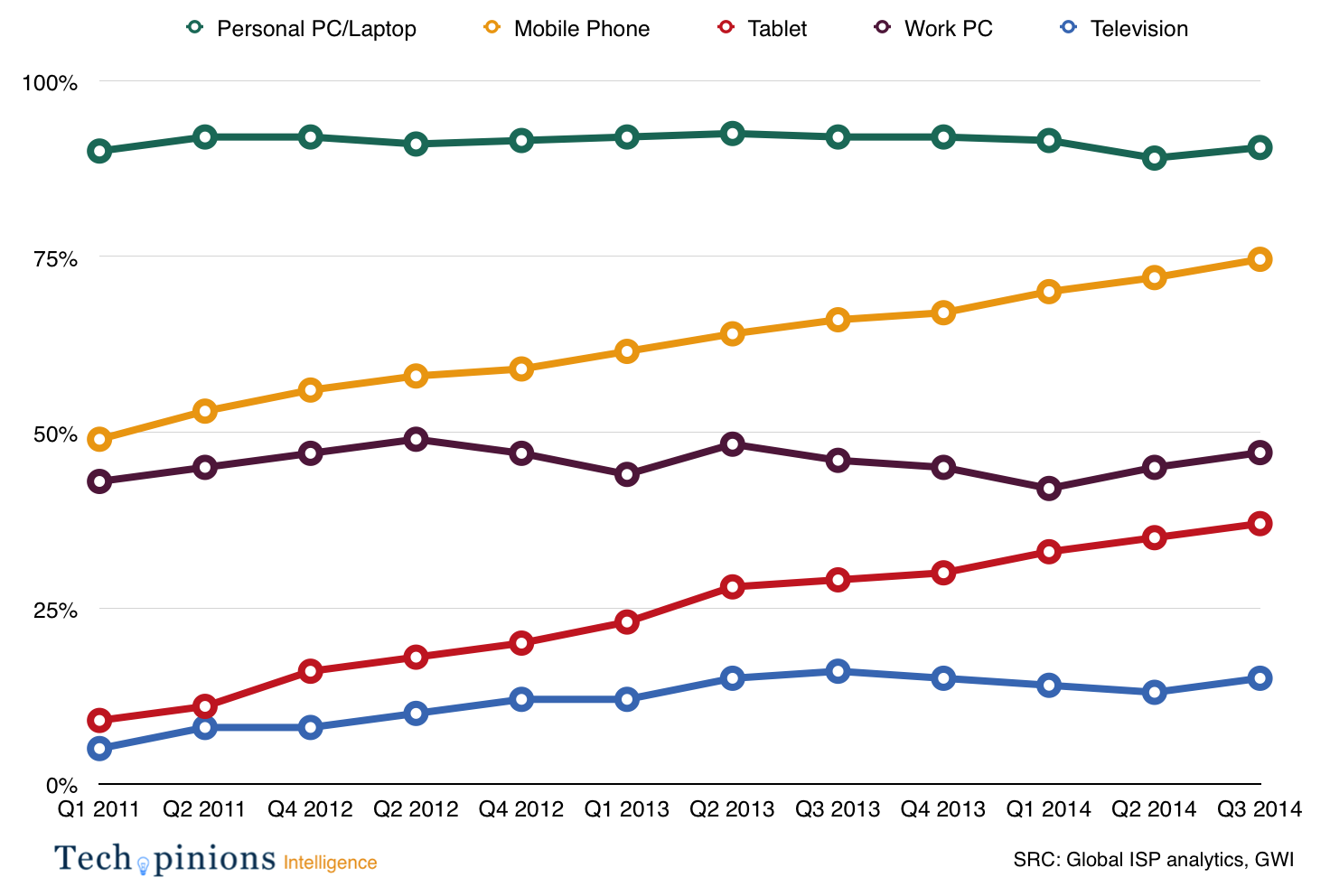

As our readers know, every now and then I like to post a chart and tease out the highlights. Today, I want to do that with some updated data. Across many global markets, consumers were asked which devices they have accessed the Internet on, either through an app or browser, over the past 30 days. This data is updated frequently so we can track the growth of internet access by device over time.

Mobile/Smartphones: This is be obvious and we can expect continued growth in internet access by smartphones for the foreseeable future.

Tablets: Tablets remain the other growth area. Given the slowdown of tablet growth overall, we can make a few observations. The first is the tablet is continuing to steal internet time from other devices, mainly the PC. The second is the tablet market is actually growing. However, it is doing so by the secondary market. Meaning that many of those initial rush of iPad buyers are continuing to hand down older iPads to other family members as they upgrade their iPad. Since this upgrade isn’t happening all at once but is trickling in over time, we see slower sales but larger use of tablets. Another is the continued explosive growth we see of Chinese white box tablets. In certain markets like Russia, India, Mexico, Brazil, and to some degree China, these low cost, no name brand tablets are quite popular. Most are dedicated game players or portable TVs, but internet access at some level should also be assumed. This is happening to a degree in the US as IDC highlighted RCA being in the top 5 of tablet vendors for Q3 2014.

As I see this data on tablets and see quarter after quarter of more people say they are getting on the internet with a tablet than the quarter before, it shows us the category is still viable and still growing.

PC/Work PC: I like that these two categories are separated in the survey. It helps us get an understanding of how much larger the consumer PC segment is vs. those who use a PC at work. When you look at both numbers, it is possible to interpret their lines and believe the PC market is simply not growing. This certainly looks to be the case. We are not adding brand new PC users at anywhere near the rate we once were. Also, as I alluded above, more PC users’ internet use is likely shifting to other devices.

I point this out in many of my focused PC industry analysis reports through my firm Creative Strategies. What we discover when we study PC behavior in both consumer and enterprise environments is the device is becoming a much more focused product than a general purpose one. People use it for specific tasks and have now defined what tasks it is better for vs. others. A great example of this is Facebook. In our studies, we found over 75% of daily US Facebook users access Facebook on their phone but while sitting at their work PC. Facebook has a browser based version so why not just use it? We find people simply prefer the mobile version, so we see this dual use of a PC and smartphone at the same time. Responses we’ve heard were that it was faster, more private, more convenient, and they could use the mobile app to get a particular task done, even though they could have done the same thing on the PC. If general purpose computing moves from the PC to devices like the tablet and even more so to the smartphone, it will bring dramatic implications to the PC ecosystem.

Television: Increasingly, more people are accessing the internet from their TV. It is important to note in this data that a game console or set top box is included. This is not referring to a dedicated connected internet TV, but to the use case of connecting to the internet in some way from your TV. Clearly Netflix, online console gaming, and other use cases drive this, but the fact it is slowly increasing tell us quite a bit about the role the TV will play going forward and the internet services are poised to be monetized from the big screen.

Given this survey comes from over 30,000 responses, what the lines also show approximates volumes. The higher the percentage of the line, the more people using the device to access the internet. Like most surveys, it does not include mobile only consumers, but we can be assured there are more people accessing the internet from a mobile device than a PC, even though these lines don’t show that. What this chart sheds light on is what the internet by device landscape looks like in the multi-screen user world. The “internet embedded into everything” is the theme. What devices dominate its usage is the interesting part to watch going forward.